01152021 :: Friday finance week in review

A partial digest of what we learned:

Biden revealed plans for a $1.9 trillion aid package that includes $1,400 checks, raising the federal minimum wage, and coronavirus-specific spending. This is in keeping with expectations that Democrats would introduce more stimulus measures in the next term cycle, but it can now be paired with a higher likelihood of passing given the blue wave of election 2020.

Stimulus is friendly to oil and other commodities (not gold), as well as to equities. That said, the health and labor situations are abysmal, and businesses continue to struggle or fail. Therefore, we may experience push and pull in the markets, i.e. volatility that persists for the foreseeable future. A more significant correction or downtrend may visit us this year.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, HYG, TMV, VXX, XLE, TAN, GLD, JDST, BITW, VB, VTWO, TNA/TZA, XLF, KRE]Additional details regarding the Capitol insurrection became known. For instance, Trump and Guiliani attempted to contact Republican lawmakers to continue to apply pressure to overturn election results even as the breach of the building was occurring and evacuations were underway.

Among many other concerning aspects, video (@ 1:32) shows a column of organized combatants passing through the melee under the cover of the Trumpist crowds and rioters, up the Capitol steps and, we presume, into the building itself. Numerous arms and explosives have been recovered, as well as evidence around the illegal entry, destruction, theft, and assaults that occurred. The whole of the day’s events is being investigated by the DOJ and FBI from a counterterrorism and counterintelligence angle.

Blame is being traded for the lack of protective forces in place on January 6. More officials have resigned, including Transportation Secretary Chao, McConnell’s wife. What is on display is that Trumpists had inside help, as well as that denial is a part of the fabric of the United States.

And now, the related death toll comes in at six persons, as another Capitol police officer was found dead by apparent suicide in the days since.

Because of the events of January 6, Corporate America is pulling GOP contributions. Specific companies to do so include the following:

Blue Cross

Marriott

Dow Chemical

Goldman Sachs

Airbnb

AMEX

GE

Mastercard

Verizon

AT&T

Best Buy

Comcast

The fallout from the insurrection is far from over, and our understanding of its scope extremely limited thus far. From a presidential transition process standpoint, the focus has turned to maintaining the safety of Biden-Harris. On Inauguration Day, it’s the Secret Service’s turn.

Moderna’s CEO indicated that SARS-CoV-2 is going to stick around, himself using the word “forever.” If so, it will be the fifth coronavirus to become endemic. The immunity to SARS-CoV-2 that Moderna’s vaccine provides should last a year, but the idea that the virus isn’t going anywhere opens the door to a perpetual stream of vaccines and, presumably, revenue for the likes of Moderna, Pfizer, Bio-N-Tech, and AstraZeneca. It also means further tough times ahead.

Significant mutations will remain a concern. Right now, things are the worst they've ever been, deaths-wise, and more infectious mutations will only make matters worse. The darkening of the health crisis, which exacerbates the troubling economic landscape, is one reason for markets to tank again. There is some safety in stimulus-driven indices such as the S&P 500, as stated here before, but hedging may be worth considering. Strategies can be as simple as insurance contracts in the form of long-dated put options on the most sensitive of sectors, including small caps.

Meanwhile, vaccine distribution hasn’t smoothened out any. On top of multi-layered hiccups with the rollout, there is apparently no existing federal vaccine reserve for states after all. Imagine that.

Yields are catching everyone's attention, as they climbed in the prior week to levels not seen since March, then traded within a narrow band this past week. There was talk of tapering, the taper tantrum of 2013, supply-side inflation, recovery, hesitant buyers for Treasuries, and no change to the Fed’s aggressive asset purchases.

It is not the opinion here that rising yields are a sign of recovery taking hold in the US, nor systemic inflation actively taking root, but rather that they are likely tied (at least in part) to a lack of buyers, as stated here in previous issues. Those potential investors probably prefer other bonds, securities, and/or assets, including foreign ones, at this time. That would change if there is a flight to safety, brought about by the current crises proving to be more protracted than hoped for.

So far, systemic inflation measures remain subdued, while the economy is deteriorating further as we speak, not recovering.

The DXY kept rebounding for the week ending January 15, even as Biden announced stimulus plans and there was chatter about inflation. One of the most relevant co-occurrences was the drop in crypto market cap back down to sub-$1 trillion levels.

Some are making the call that the $USD will be part of a US recovery play as traders cycle out of foreign assets and back into American ones, with eyes on a recovery taking hold. This is certainly possible, but that recovery simply isn’t here yet, only hope of one.

When that day comes, the greenback could appreciate further. However, cryptoassets may continue to present competition. What isn’t advisable is naked shorting of the $USD. Aside from the potential for incoming flights to safety boosting the DXY, Biden-Harris bring credibility back to this country on the international stage. Perhaps that will lead to even greater FDI between these shores, which would bolster the DXY.

[tracking: DXY, BTC, ETH, BITW, PYPL, VYGVF]The cutting out of Chinese equities from US exchanges proceeds, with BlackRock the latest to remove said stocks from five of its ETFs, to sync with removals from underlying indices on which they are based. In addition, the financial services firm has nearly sold out of its stake in China Telecom, per the US ban.

[tracking: MCHI, FXI]Dimon is worried for JPM Chase. A new breed of fintech entities is a serious threat to his financial institution, he believes, especially on the payments front. These include PayPal, Square, and Stripe.

Absolutely, we should be scared s---less about that. We have plenty of resources, a lot of very smart people. We’ve just got to get quicker, better, faster… As you look at what we’ve done, you’d say we’ve done a good job, but the other people have done a good job, too… I expect to see very, very tough, brutal competition in the next 10 years. I expect to win, so help me God.¹

[tracking: JPM, PYPL, SQ]A Trump official’s parting gifts to the banking industry: rules forcing them to lend to gun and oil companies, as well as federal banking charters for tech firms. This, as more banks and activist investors worldwide are turning away from the sectors in question, and financial institutions are already under pandemic strain, never mind facing additional competition for customers. As with so many things, the pandemic is hastening certain trajectories, incuding the disruptive force that is fintech. There will be new winners and losers.

[tracking: XLF, KRE, PYPL, SQ]The US Treasury’s aid disbursements to airlines began. There are plenty of strings attached, including no dividend payouts, share buybacks, or unfettered executive comp allowed. Things still look pretty rough for them, for the time being, and chances are that we may yet see a major bankruptcy in this space. American is the airline that the markets perceive to be the most vulnerable.

[related: BA, AAL, DAL, LUV, JBLU, ALK, SAVE, UAL, MESA, XLE]Retail sales fell again for the month of December, which is troubling from a GDP/consumption perspective given it was the holidays. Online retailers were among the hardest hit. Personal consumption made up some 68% of GDP at last reading, so holiday weakness doesn’t bode well for the next little while.

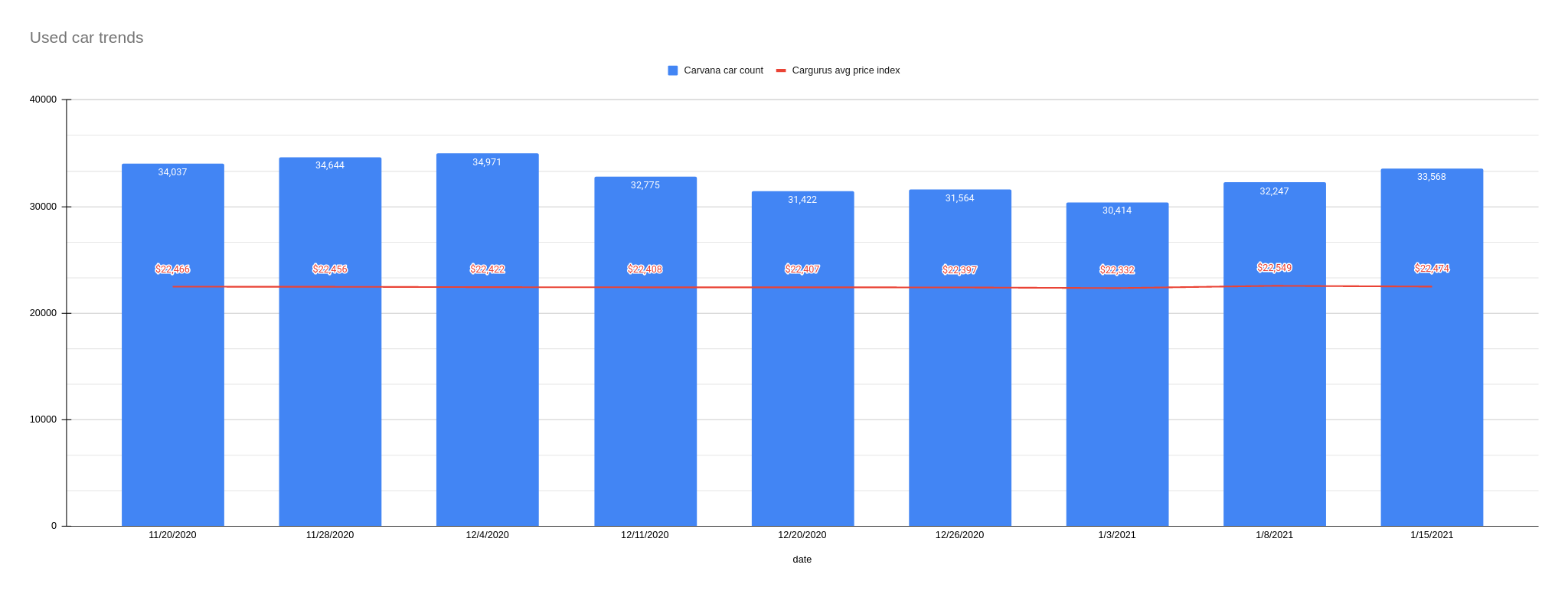

On the other hand, auto dealers had a good month with a nearly 2% rise in sales, which is in keeping with the shrinking inventory for the month of December per the used car trends featured weekly in this newsletter. That decreasing inventory trend has since reversed, however, as highlighted below.

Time will tell how much more fiscal stimulus there will be, and how it will impact retail and other sectors.

[tracking: XRT]Initial jobless claims in the US leaped to 965k (SA) for the week ending January 9, much higher than a downwardly revised 784k for the week prior. One year ago, we saw 207k.²

To add to this, 284k+ people on an unadjusted basis applied for PUA, up significantly from the previous week’s 161k+.

As of December 26, over 18.4 million people were still claiming unemployment benefits of some kind, down over 740k from the week prior. The EB program once again saw the biggest increase, adding over 375k people, which is of concern as this is the benefits program folks end up in after they’ve exhausted regular UI benefits; it’s the program after the programs, on the way to running out of benefits altogether. In the comparable week one year ago, the US witnessed more than 2.1 million people claiming unemployment insurance from all programs together.³

That said, for those who still have employment, real average hourly earnings for all wage earners increased 0.4% from November to December. This is an increase of 3.8% over the same period one year ago. There may be pressure on employers to pay higher wages to maintain operations in the midst of the pandemic. However, because it is an average, it may also be skewed by outlier wages that don’t actually provide an accurate picture of the situation for the bulk of wage earners.

Mortgage applications jumped a considerable 16.7% (SA) blended for the week ending January 8, mostly led by refi activity jumping 20% but including homebuyer applications rising 8%. The 30Y fixed came in at 2.88%.

Who are the borrowers, though? Per AVP Kan and the weekly MBA survey,

The lower average loan balance observed was partly due to a 9.2 percent increase in FHA applications, which is a positive sign of more lower-income and first-time buyers returning to the market.⁴

How is it possible exactly that with housing prices at all-time highs and an employment situation in the dumps, lower-income and first-time buyers are “returning to the market”?

It can happen if lenders relax their criteria further, adding risk to the system in the process. If instead it’s purely highly-qualified first time homebuyers, then it’s just another example of how we’re exhausting the pools of available housing consumers at these low mortgage rates. After that, then what?

[tracking: DRV, XLRE, NLY, VNO, SPG, W]Used car trends: The latest Carvana car count as of January 15 increased 4.1% to 33,568 vehicles from 32,247 the week prior, while the CarGurus average price index fell 0.33% to $22,474 from $22,549. We once again have both growing used car inventories and declining prices.

Sovereign matters:

China tightened by withdrawing liquidity from its financial system for the first time in months, in order to moderate lending. The country’s central bank is signaling that they seek to curb their economy’s leverage levels.

A total resident drain is taking shape in Hong Kong in response to the Hong Kong national security law passed by China last year. Some two-thirds of the city’s population are eligible for British citizenship, and the UK will be opening that path as January comes to a close. Many are expected to take advantage of it. This has drawn criticism of interference from China.

Any negative impact on the Hong Kong dollar may be countered by an ever greater number of Chinese firms listing on the Hong Kong exchange.

The Swiss are trying to avoid a full coronavirus lockdown, opting instead for tighter restrictions. In particular, the country is concerned about the newer variants of SARS-CoV-2.

Angola is set to receive another installment of its $3.7 billion in funding from the IMF, amounting to nearly $500 million. Basically, the country has stuck to the plan, according to a routine review of its borrowing program. This has involved passing austerity measures and weaning itself off oil revenues.

[tracking: EDC, VXUS, VWO]The current state of equity: “Moral Tragedy Looms In Early Chaos Of U.S. COVID-19 Vaccine Distribution.”

As of January 15, the US witnessed 169,126 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s approximately 444 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 395,882, puts the probable COVID-19 death figure somewhere north of 510k. Across all causes of death, we’ve suffered 114% of the deaths we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

¹ Son, Hugh. “Jamie Dimon Says JPMorgan Chase Should Absolutely Be ‘scared s---Less’ about Fintech Threat.” CNBC (January 15, 2021).

² The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

³ “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-60-NAT. US Department of Labor (January 14, 2021).

⁴ “Mortgage Applications Increase in Latest MBA Weekly Survey.” Mortgage Bankers Association (January 13, 2021).