11272020 :: Friday finance week in review

A partial digest of what we learned:

CNN reported that the General Services Administration (GSA), through admin Emily Murphy, has notified the Biden-Harris campaign that the Trump administration is prepared to begin the formal transition process. As Trump has pointed out, that is separate from whether he continues to contest the election.

On Thanksgiving day, Trump indicated that he would leave if Biden were declared the winner by the Electoral College. However, multiple steps must still be performed to get to that actual announcement.

January 6 is when Congress meets in a joint session to tally the electoral votes that were received by Pence by December 23 after being cast on December 14. At that point, Pence, being the president of the Senate, announces the victor. However, objections can subsequently be lodged, to be considered separately by each congressional branch.

In the meantime, from now until December 8, state election results can be legally challenged as the various states seek to certify their results. If disputes are not resolved by December 8, Congress gets involved.

Michigan has certified its results, in spite of the Trump campaign’s preferences to the contrary. Politico performed a deep dive into the state’s election saga, including the aforementioned White House visit, the play at presenting alternate state electors, the rules that dictated how specific ballots were counted in the first place, old regional wounds and grudges, the nature of the state’s GOP majority, a Republican member of the state canvassing board who chose to break from his party on the path to certification, and more.

Amid reports in Wisconsin that Trump observers are attempting to obstruct the recount process in the two counties in question, the recanvassing effort there proceeds behind schedule. Full results may now not be known until December 1. What we do know is that Milwaukee county has completed its tally and found additional votes for Biden. Legal challenges by Trump lawyers to the validity of some ballots in the state remain.

In Georgia, Trump has indeed requested a recount by machine of all ballots. It is to be completed by the end of the night of Wednesday, December 2.

Nevada, Pennsylvania, and North Carolina all certified their results this past week. The first two officially went to Biden, while the third went to Trump.

In the Pennsylvania matter pending with SCOTUS, Democrats have sought an extension to file a brief in opposition to Republicans’ petition for a writ of certiorari, and it has been granted. Additionally, three organizations have jointly filed an amicus brief in support of the GOP position.

Meanwhile, a federal appeals court rejected the Trump campaign’s move to block a Biden PA win. This followed in the wake of a public hearing held by the PA Senate Majority Policy Committee in Gettysburg featuring Giuliani. Trump dialed in and then, in a Michigan repeat, invited state GOP leaders to the White House. Nobody has said a word about it since, but state lawmakers had already previously stated that they would not be interfering in the election.

The presidential transition appears destined to proceed incrementally. Because Trump is not conceding, the full election process is being put through its paces. Each stage must be acutely realized. This leaves us to run a hurdles course, and markets may behave accordingly.

Resting on the transition is the promise of large fiscal stimulus, the perception of future stability, improved management of the ongoing health crisis, and the normalization of global political relations, among other things. Hence, every hurdle that the transition clears may be accompanied by gains in equities, the loosening of bond yields, declining price action in gold, and upward momentum in oil, not to mention a declining dollar.

Conversely, every complication may serve as a market setback.

[tracking: SPY, VTI, QQQ, XLK, EDC, VWO, VXUS, LQD, VXX, XLE, TMV, GLD, VB]For brick and mortar retailers specifically, Black Friday is already being called a bust. People did not hit the stores. What appears to have happened is that they shopped from home as the pandemic further accelerated the transition from in-person to online shopping. This reinforces existing cases for tech and raises the possibility for shorting opportunities in commercial real estate and/or among certain physical retailers that have no online game and no plan.

[tracking: XRT, SPG, VNO, VNQ, XLK, QQQ]Mink keep making the news. Last issue mentioned the zoonotic nature of SARS-CoV-2, a mutated strain (referred to as “cluster 5”), human-mink joint infection by the mutated strain, the Danish cull, investigations in Ireland and Sweden, and outbreaks in the US states of Wisconsin and Utah.

At present:

No organization is publicly stating that “cluster 5” or any other mutated version of SARS-CoV-2 is a threat to vaccines being tested at this time.

Oregon is now reporting a COVID-19 outbreak among a mink farm’s livestock and employees, although Oregon state officials had previously taken the stance that there was nothing to worry about. This perpetuates the trend that those who take a minimizing approach during this pandemic are to eat their words later. The farm is under quarantine.

Denmark is having to rebury their culled mink as gases tied to corporal decay appear to have caused the dead mink to resurface from their shallow trench graves. At the same time, some mink may have escaped the nationwide culling altogether, raising concern that they would spread the infection among wildlife. The country’s prime minister has apologized for the handling of the situation as the hastily undertaken culling was a major, self-inflicted economic blow and has resulted in further adverse consequences for the nation.

It’s possible Ireland will cull its mink population, as well.

Lithuania has found mink livestock infected by SARS-CoV-2 and is employing a more limited cull than Denmark.

Polish scientists have identified cases of COVID-19 among their country’s mink population. The nation is the third largest producer of mink fur globally, behind China and Denmark. Apparently, the government is denying the finding.

France has discovered coronavirus infected mink among its own livestock, according to agriculture ministry officials.

Other European countries with active cases among mink not mentioned last go around include the Netherlands, Greece, Spain, and Italy.

Russia will reportedly seek to inoculate its mink population with a mink-specific vaccine that is currently under development so as to simply avoid infections among its livestock population. For multiple reasons, it’s difficult to take this seriously.

AstraZeneca officially joins Pfizer-BioNTech and Moderna as a vaccine heavyweight contender, but may launch a new trial amidst questions over preliminary data and a dosing error. That said, the efficacy of their vaccine with the dosing error could be as high as 90%, pending further results.

Markets have priced in stellar vaccine news. A major reversal would occur if something like a mutation called into question the efficacy of vaccines already on their way. All other questions posed in prior issues stand, including logistical ones expanded on elsewhere. And the research goes on.

There is no new fiscal stimulus, and still may not be until winter of 2021. There is also nothing new to report on any efforts by Mnuchin and McConnell to re-appropriate funds originally dedicated to Federal Reserve lending programs for a smaller stimulus package, nor on stimulus discussions between Biden, Pelosi, and Schumer.

What has surfaced is concern on the part of some Biden advisers that without immediate stimulus (no matter how small the package), we could be hit by a double-dip recession. How it would be a double-dip when we haven’t any clue when we’re going to exit from the recession we’re currently in is unclear.

At any rate, such opinion would bolster the Mnuchin-McConnell approach, if indeed Mnuchin will make good on extending funding for the majority of Fed lending programs leaving 90 days in the tank for 2021. Otherwise, taking money from one place to use it in another is just a rearranging of deck chairs.

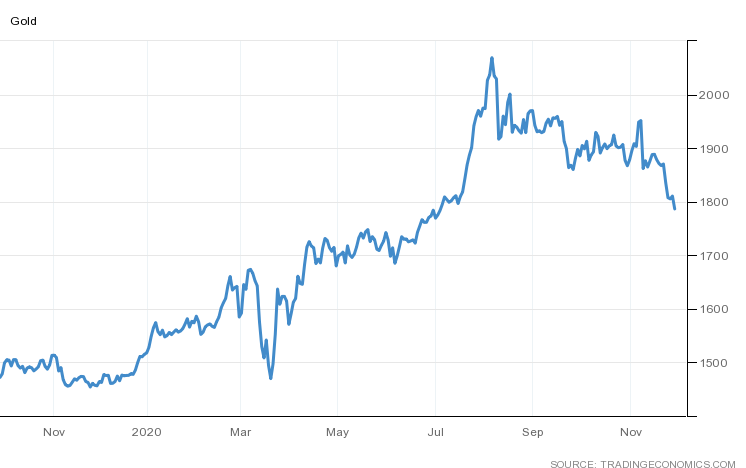

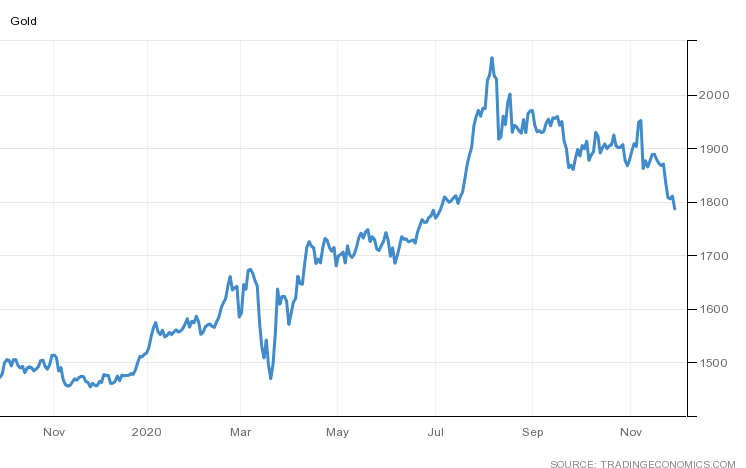

The precious metals complex suffered another blow. The thesis here remains that the next major wave for gold (and silver) is down. In fact, that major wave may well be upon us and picking up steam.

With progress on the vaccine front and increasing clarity around the presidential transition, there is less and less to justify gold ownership, not that there was that much to begin with. Of course, if new information calls either the presidential transition or vaccine efficacy into question, gold could see a bounce.

In considering short positions, a play on junior gold miners offers more volatility and greater return potential.

[tracking: GDX, GDXJ, GLD, DUST, JDST, SLV]The Biden-Harris administration is to select Janet Yellen as incoming Treasury Secretary. Yellen was head of the Fed when Trump took office and her term was allowed to expire. Instead, Powell was appointed.

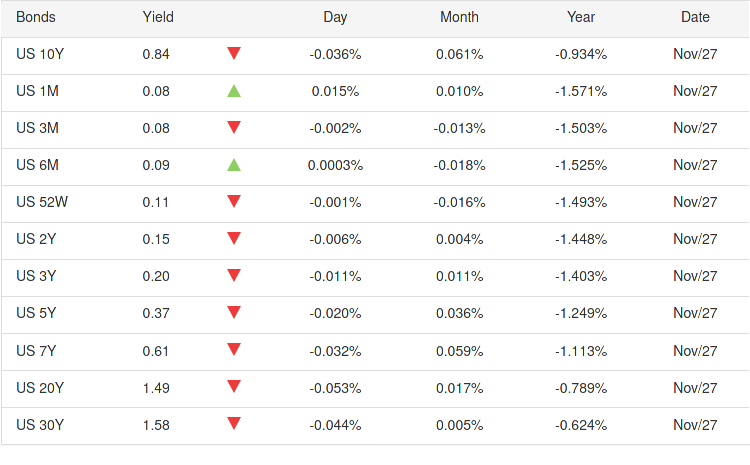

Yields tightened to close out the week. Together, the US health and political crises are a walking disaster. Illness and division are not conducive to personal and economic productivity and growth, not to mention the psycho-emotional toll on the populace. Small-ish and repeated flights to safety via bonds could be here to stay until we really round some corners.

[tracking: LQD, HYG, TMV]

Initial jobless claims in the US rose to 778k (seasonally adjusted) for the week ending November 21, up from an upwardly revised 748k the week prior and continuing the reversal of the earlier downtrend in numbers. We are approaching the 800k level again. One year ago, we saw 211k. The labor picture remains poor.

To add to this, nearly 312k people on an unadjusted basis applied for PUA, down from just under 320k the week prior.

As of November 7, close to 20.5 million people were claiming unemployment benefits of some kind, up 135k+ from the week ending October 31. In the comparable week one year ago, the US witnessed a bit less than 1.5 million people claiming unemployment insurance from all programs.

[tracking: SPY, VTI]New home sales declined to an annualized 999k units on a seasonally adjusted basis for the month of October. Meanwhile, months’ supply of housing ticked up to an estimate of 3.3 months at current rates based on 278k homes left for sale at the end of the period. Declining sales and increased supply would support the thesis that we will see oversupply in housing at some point.

However, more recently measured mortgage applications reversed course to jump 3.9% overall for the week ending November 20, with large gains in both homebuyer (3.5%) and refi (4.5%) applications.

As reported previously, JP Morgan eased lending requirements. It is probable that other financial intermediaries did, as well. In that case, one explanation for the surge would be that some applicants, blocked before, now fall within the adjusted acceptable range. Simultaneously, the 30Y mortgage rate decreased further to 2.92%, a record low. This may also continue to pull consumers out of the woodwork.

In this way, and at these rates, lenders and consumers could continue to chip away at current and incoming supply and keep the housing market simmering for a little while yet. However, that’s not entirely comforting, and there are some disquieting trends.

Removing lending curbs is a risk-on, and perhaps even a moral hazard, move in the midst of a global health and economic crisis with no firm recovery in place. What’s more, home prices continued to rise for the month of September and Q3-2020 more broadly, as did prices for homes under construction for the month of October (and really for the whole year thus far). Such a scenario sets us up for an unsustainable run.

One catch is that the number of homes that have been sold but not yet started is growing at such a rate that they outstrip those that are already under construction or those that have been completed. Is this due to construction workers falling ill, or because demand is that extreme, or is it some combination of the two? Will it ensure a backlog that will help the market avoid, or at least delay, an oversupply situation? Then again, how many sales of unbuilt homes can the market carry?

[tracking: XLRE, NLY, VNO, SPG]

EVs may be a bubble in the making. This is not a comment on the structural shift to electric vehicles; that trend is firmly in place. Indeed, bubble formation and popping is historically often part of the establishment of long-term trends (tech, housing, bitcoin), and it seems that it will prove no different with EVs.

Rather, the point is that get rich quick tendencies and FOMO are driving investor behavior, not fundamentals. This is fueling stock valuations on all players, no matter their prospects or whether they’re even producing a product, to impossibly high levels. While there’s definitely money to be made here, there’s also pain in store for some.

Used car trends: The latest Carvana car count rose to 34,644 vehicles from 34,037 the week prior, while the CarGurus price index fell ever so slightly to $22,456 from $22,466.

Oil has had a good month. This seems largely driven by the same two dominant factors driving most everything else in the US: vaccine success and progress on a presidential transition. It certainly isn’t actual inventories.

Yes, OPEC+ is debating whether to keep supply curbs in place, which are supporting oil prices. Increased holiday travel is also supportive in the very near term, as is the promise of a larger fiscal stimulus package under Biden-Harris. The pandemic as we know it will eventually pass.

However, oil’s time is limited. The world is evolving. Climate change is popularly less debatable. Industry majors are snapping up power traders to shore themselves up against a clean-energy future and make a profit. Europe is moving rather strongly in that direction, as is the world of finance. EVs increasingly represent an unstoppable wave. Renewables are cheaper every day. Obstacles to the oil industry’s return to prominence are only accumulating, not the other way around.

There may be a couple of good runs left for the commodity, but if modern society persists, it will be going the way of coal.

On the inflation front, the PCE came in flat for the month of October. The more recent November PMI indicates that prices for goods and services are on their way up, in part because of broken supply chains, as suggested before.

Personal spending growth, while positive, extended a downward trend for the month of October. This is not surprising given the ongoing lack of fiscal stimulus. Time will tell if this picked up for the month of November given that the holiday shopping season has begun.

[tracking: XRT]Airports and airlines are busier, which, on the one hand, is a positive for related stocks and oil, and on the other, all but ensures more COVID-19 cases for the holidays.

[tracking: BA, AAL, DAL, LUV, JBLU, ALK, SAVE, UAL, MESA, XLE]

Sovereign matters:

China is looking to double the size of its economy by 2035. In order to accomplish that, an official has revealed that GDP would have to grow by an average of 4.73% each year leading up to it. Perhaps opening its bond market to the rest of the world will help.

Fitch revised downward Tunisia’s outlook to negative, due to the potential for a liquidity crunch in the midst of the pandemic. Concerns include the size and nature of previously undisclosed government arrears to private vendors and SOEs because of “off-budget spending.”

Fitch downgraded Sri Lanka, citing worsening debt metrics like an extremely high interest to fiscal revenue ratio and potentially shrinking access to outside financing, among other things. In part, this would complicate the country’s capacity to make its payments. The nation is also challenged by decisions to cut taxes (2019), offer new tax incentives, and increase public spending.

S&P downgraded Panama due to worsening debt servicing metrics, including its interest to government revenue ratio. Weighing heavily on the country’s finances is the deteriorating health of its national pension fund, in addition to the pandemic.

Moody’s revised downward Kyrgyzstan’s outlook to negative, as the nation has slipped into political turmoil defined by contested elections, violence, and now sitting parliament’s rush to overhaul the constitution in support of what appears to be a power grab by the former acting president. All this could discourage FDI and cloud Kyrgyzstan’s ability to secure financing, magnifying the effects of the pandemic.

Moody’s downgraded Belize, citing the likelihood that the country would seek to defer interest payments as its tourism industry suffers considerably, adding to pandemic woes. In the wake of this year’s general election, officials may also pursue debt restructuring. Either way, investors should presumably anticipate losses.

[tracking: EDC, VXUS, VWO]

As of November 27, the US witnessed 133,317 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s 400 people per day on average. As pointed out by the CDC, many of these could be miscategorized COVID-19 fatalities that are going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the latest official coronavirus death toll of 264,709, puts the likely COVID-19 death count somewhere north of 330-340k. Across all cause-of-death categories, we’re witnessing 112% of the deaths that we would have expected in a non-pandemic year given historical trends.¹

In general, be cognizant of unstable COVID-19 data during the holiday period, especially around the number of cases, tests performed, and fatalities. With each passing holiday, figures are likely to fall only to spike before regaining some consistency in between.

Footnotes

¹ Valenta, Philip. “Death by COVID-19 Hides in Plain Sight.” HedgeHound archive (November 27, 2020).