12112020 :: Friday finance week in review

A partial digest of what we learned:

The FDA has authorized Pfizer-BioNTech’s vaccine for rollout in the United States effective December 11, 2020. A panel that advises the government agency strongly suggested it be implemented on December 10. BNT162b2 is already being used to inoculate residents of the UK, and Canada issued emergency authorization in the middle of the week.

States will decide who receives the vaccine within their geographies over the next couple of days, but healthcare professionals and residents of long-term care facilities will be prioritized.

One grand notion being circulated is that through the combination of the three vaccines expected to be authorized for emergency use in the US, enough shots could be distributed by the middle of next year to vaccinate all of the willing.

Though BNT162b2 prevents illness, it is not clear yet whether it prevents infection or transmission of SARS-CoV-2. Also unknown is how to address the illness among those who don’t meet the parameters of the subset of the population targeted for inoculation, including those younger than 16 and those who have already been sick.

December 8, the electoral process safe-harbor deadline, passed without incident. Congress didn’t have to get involved to resolve any lingering disputes, though SCOTUS rejected a Pennsylvania Trumpist request to void millions of mail-in ballots and block the state from certifying its election results.

The original PA case exploring the question over whether the state’s supreme court had authority to extend the ballot receipt deadline (as opposed to the state legislature) is still pending with SCOTUS and may be heard early next year.

Meanwhile, Texas threw its hat into the ring on Monday. Additional parties signed on both in support of Texas and in support of opposition to the Lone Star State’s move to either derail the electoral college vote set for December 14 or overturn the election results of four other states: Georgia, Michigan, Pennsylvania, and Wisconsin. The argument, filed in such a way as to seek original jurisdiction, roughly stated that election procedures in those states in particular were changed in a way that violates the country’s Constitution. Trump wanted in on the action.

By Friday evening, however, the Texas motion had been dismissed by SCOTUS on the grounds that Texas had no business in how other states handled the election. In response, Chairman West of the Republican Party of Texas suggested secession by “law abiding states.” Court observer Amy Howe wrote,

With the Electoral College vote slated to take place in just three days, Friday’s order as a practical matter puts a stop to efforts to contest the results of the election through litigation. It’s less clear, however, that the order can end the partisan divide in the country.¹

To its credit, SCOTUS has repeatedly resisted involvement in this year’s election.

On Monday, electors will visit their state capitals to cast their votes, presumably according to the popular vote, further entrenching Biden’s victory in the process. Accordingly, we may see positive market action to kick off the week.

Equities and oil still stand to gain / yields loosen / gold decline from the clearing of presidential transition hurdles, and retreat / tighten / bounce from any serious complications that arise. However, the realization of a Biden-Harris election victory may begin to have diminishing returns as it’s overshadowed by severe headwinds, including the nation’s fiscal stimulus game of chicken and poor labor situation.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, SJB, TMV, VXX, XLE, TAN, GLD, VB, VTWO, TNA, XLF, KRE]One thing that big government in the US has become quite adept at this year is delivering stimulus disappointment, as opposed to fiscal relief. A package has not materialized, and markets have given up some gains because of it.

The narrative hasn’t changed much. There are still snags, just as there were before, and just as there will be tomorrow. What’s more, they are the same as they ever were: issues like COVID-19 lawsuits and aid to states and municipalities.

Some analysts are saying we should expect only one stimulus bill of size beyond the CARES Act from here on out, given the McConnell effect and vaccines. Whenever (if ever) that stimulus package arrives, in what’s left of 2020 or next year, it’s very possible it could be the last coronavirus package we see. That would take some of the wind out of equities’ sails and reduce the likelihood that the US would see sustained inflation on account of fiscal stimulus, anyway.

[tracking: SPY, VOO, VTI, QQQ, XLK, EDC, VWO, VXUS, LQD, SJB, TMV, VXX, XLE, TAN, GLD, VB, VTWO, TNA, XLF, KRE]Initial jobless claims whiplashed back to 853k (SA) for the week ending December 5 from an upwardly revised 716k the week prior. One year ago, we saw 237k. The labor picture remains ugly.²

To add to this, nearly 428k people on an unadjusted basis applied for PUA, up sharply from a revised 288k the previous week.

As of November 21, over 19 million people were still claiming unemployment benefits of some kind, down over 1.1 million from the week prior. It’s probable that at least part of the drop is actually due to UI benefits simply running out for some. The amount of time an individual can receive such benefits is limited in each available program at the state and federal levels. In the comparable week one year ago, the US witnessed just slightly over 1.5 million people claiming unemployment insurance from all programs.³

Unless the government sees to an extension of public assistance, the PUA and PEUC UI programs will expire at the end of this year. At that point, millions will be left without UI benefits and still no work.

Most federal agencies lost their funding on Friday. A vote on a week-long stopgap budgetary spending bill to avert a government shutdown is slated for this coming Wednesday.

“Overcrowding” may become a new buzzword as more traders express their hesitation over the easy street recovery consensus taking root among investors. EMs are one such potential area of focus, and Morgan Stanley is already scaling back its bets. South Korean households are taking a different tack, borrowing at record rates to go all in on what are local exchanges to them.

Even the BIS is concerned over general asset valuation levels. Again, incoming sell-offs in global equities markets are not out of the question.

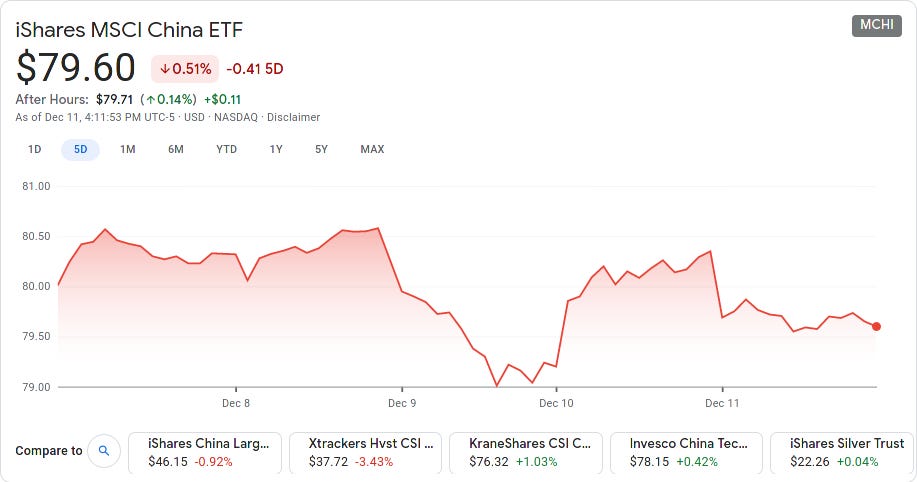

[tracking: SPY, VOO, VTI, QQQ, XLK, EDC, VWO, VXUS, VXX, XLE, TAN, VB, VTWO, TNA, XLF, KRE]We just got a tiny bit closer to the broader delisting of Chinese equities some day, in part because special treatment of said equities isn't an abstract exercise anymore. Dow Jones and S&P have begun the process of removing ten China-based companies from their bond and equity indices in what may just be a harbinger of things to come. The removals are to be completed by December 21. These securities are linked to companies that apparently have ties to the Chinese military. A recent executive order forbids trading in such securities in the US beginning January 11.

In the meantime, it would appear that either the list of companies is growing, or that there’s more than one such list of corporate entities with Chinese military ties. Whether the executive order banning investment applies to them all or not is unclear.

Meanwhile, the separate bill to delist Chinese companies that do not comply with financial oversight regulations has passed both chambers of Congress and only remains to be signed by Trump. There is a three-year phase-in period, so even by becoming law, the bill doesn’t change much overnight. All the same, many companies that have become household names for investors, like Alibaba and Nio, stand to be delisted over time if they refuse to submit their financial audits for scrutiny.

[tracking: MCHI, FXI]Another reason to believe corporations are less healthy than they seem is supply chain financing, according to reports. Such loans made to make a company’s suppliers whole don’t show up as debt on said company’s balance sheets but rather as payables, making them hidden, in a way. Failed hospital operator NMC Health was a notable case this year of such financing use.

“Financial Accounts of the United States” data released by the Federal Reserve indicates that US households gained wealth in Q3-2020. In particular, holdings of corporate equities and Treasuries jumped through the months of July-September [F.101]. Owners’ equity in real estate continued to increase, as well [B.101].

On the liabilities side of the ledger, outstanding mortgages and “other loans and advances” grew considerably from the previous quarter [F.101].

All developments that made life a little easier for households this year may have freed up funds to contribute toward wealth gains, including refinancing existing home loans at record low rates and mortgage and student debt forbearance.

Moving forward, a lot has to go right for wealth gains to stick, and there are no such guarantees on tap.

Mortgage applications were down again, this time by 1.2% for the week ending December 4. Homebuyer applications declined 5%, overshadowing a slight rise of 1.8% in refis. Rates wise, the going 30Y fixed dropped further to 2.9%, a new record low.

A reminder that FHFA is extending to the end of January 2021 the window to request agency forbearance, as well as receive foreclosure/eviction protection.

On the commercial front, CMBS delinquency rates remained elevated in Q3, though they declined slightly from the previous quarter.

The outlook here remains that real estate is eventually headed for a correction, at the very least, prompted by a chain reaction involving the spiraling health crisis and persistent labor weakness, in particular.

Net-zero is the new global climate objective being uttered from all corners, and the New York state pension fund may help lead the way in the US, as well as activist investors.

For its part, the EU has reached a climate accord that may result in net-zero in 30 years. Member nations will be helped along in order to achieve the targets. On a related note, the World Bank is adopting stricter climate-oriented targets for the next five years of lending to developing nations.

As the pledges pour out, serious questions remain about just how we’re going to get there.

Travel is not recovering anytime soon, says major airport operator GAP, of Guadalajara, MX. Indeed, this is likely to continue to exert downward pressure on airlines, cruiselines, hospitality operations, and the oil industry, among others.

Car sales in China rose yet again, including those of new energy vehicles like EVs. The market there is closely watched for its size as well as adoption of battery-powered automobiles.

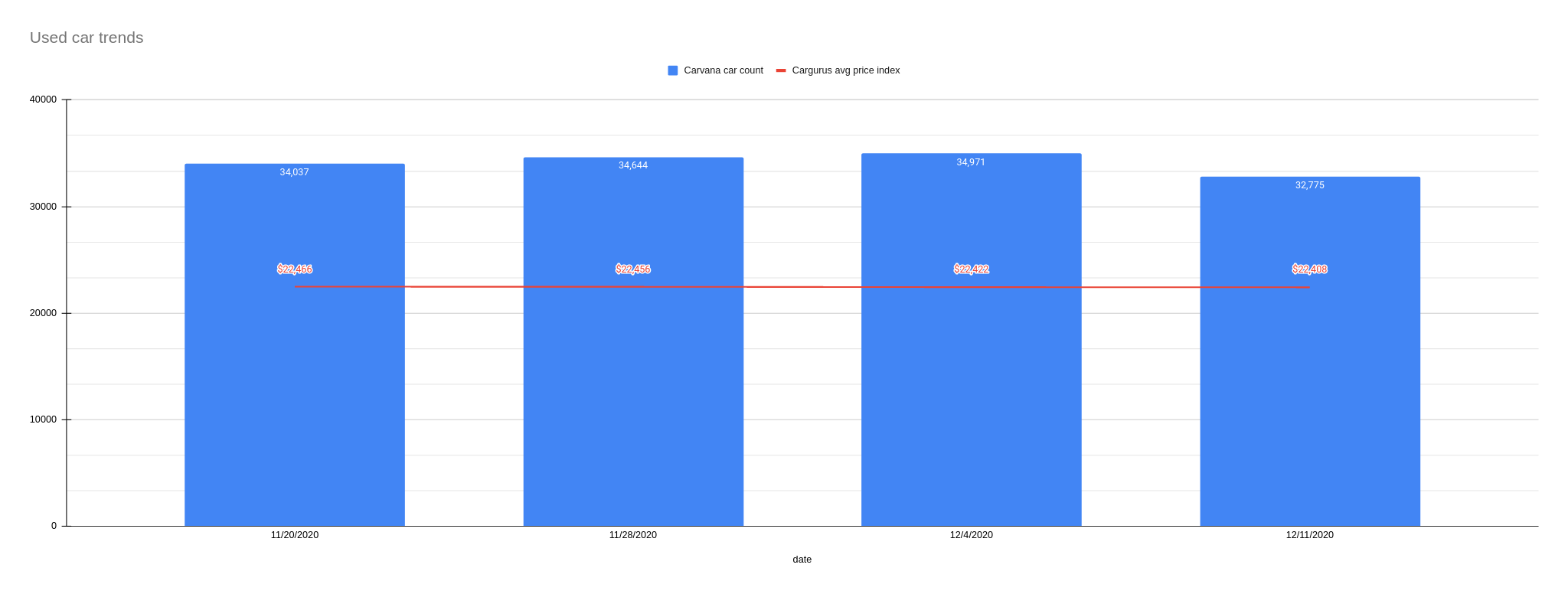

Used car trends: The latest Carvana car count for the week ending December 11 dropped to 32,775 vehicles from 34,971 the week prior (-6.28%), while the CarGurus price index again fell slightly to $22,408 from $22,422 (-0.06%). It’s the holiday shopping season, after all.

Sovereign matters:

Hungary and Poland [sort of] got out of the way of the latest eurozone stimulus package and will [probably] join in the 27 nations feeding at the trough. The ECB kept up its accommodative stance, as well. A rally in equities was over almost before it begun, though, due to the dire coronavirus situation and renewed restrictions, no new fiscal stimulus out of the US, and the Brexit deadbody drag, among other things. More major indices on the continent finished down than up on Friday, and were roughly split for the week.

Cuba will finally be unwinding its two currency policy come January of 2021. For decades, the country has been maintaining a local currency (CUP) for resident nationals and a convertible currency for outsiders (CUC). In practice within the country, this relied on a provider of goods or services sizing up every customer who appeared. Now, the CUC will be done away with, and the CUP pegged to the $USD at 24:1.

Bulgaria’s 18 banks have been green lighted by the nation's monetary authority to offer a loan forbearance extension to households and companies that request it. Some $5.27 billion in loans is on the table.

The Asian development bank has launched a $9b vaccine facility to assist it's developing members in accessing the medicines and inoculating their populations.

Germany will allow itself more indebtedness in 2021.

The BoE will permit UK banks to once again pay dividends, while their eurozone and American counterparts still cannot.

Zambia has asked for IMF assistance. The country is in default.

S&P downgraded Sri Lanka due to reduced capacity to service it's debt, especially given its low forex holdings.

Fitch is cautioning that Canada may be headed for more negative sovereign ratings action based on released fiscal plans, should revenue not pick up. Canada was already downgraded from AAA by Fitch earlier this year.

Indeed, the company sees ratings pressure persisting for potentially all of the world's economies in 2021, with upgrades unlikely.

[tracking: EDC, VXUS, VWO]The state of equity long read: Homeless watch over properties being flipped.

As of December 11, the US witnessed 139,101 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s 400 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 297,971, puts the likely COVID-19 death figure somewhere north of 370-380k. Across all causes of death, we’ve suffered 113% of the deaths we would have expected in a non-pandemic year given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a pre-existing one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably considerably higher.

Footnotes

¹ Howe, Amy. “Justices Throw out Texas Lawsuit That Sought to Block Election Outcome.” SCOTUSblog (December 11, 2020).

² The data quality of these numbers is still compromised, as outlined in last week’s issue and based on a GAO report.

³ “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 20-2249-NAT. US Department of Labor (December 10, 2020).

Correction, the budgetary shutdown stopgap measure cleared both chambers of Congress and was signed by Trump on Friday, December 11.