11132020 :: Friday finance week in review

A partial digest of what we learned:

The drama over the presidency remained in full effect over the preceding weekend and into last week. Biden and Harris took their victory lap with a public appearance Saturday night, November 7, and quickly began working, unveiling their transition website and specific language around racial equity, countering the COVID-19 pandemic, climate change, and facilitating an economic recovery.

Biden “cemented” his victory as Arizona was more clearly called for him, but of course, Trump has not conceded. Keep in mind that in Trump, we have someone nobody believed could even be the Republican nominee, let alone the President, an individual who has argued for his own way at every turn, a politician who, with the help of his party’s senators, steamrolled the federal impeachment process. Now, an entire world would think it appropriate for him to voluntarily announce he’s done. Mental illness or no, we should not be surprised when he does not.

What we are left with is the attempt to gum up the election works with lawsuits that seek to invalidate the results in various places. Many of these suits have been thrown out, some have been pulled, some are pending, and at least one is on appeal.

In the legal case over the GOP’s objections to the Pennsylvania Supreme Court's ruling to extend the ballot receipt period for the election, the Supreme Court of the United States accepted further filings from both Democrats and Republicans. For their part, the GOP claimed that nobody could verify that the election boards in PA were following secretary of state guidance that ballots arriving after the evening of election day were being set aside and tallied separately from all other votes. Therefore, they sought a reiteration of the SCOTUS order reinforcing the original guidance, as well as an injunction to stop the counting or leave the ballots in question uncounted.

In turn, Dems urged SCOTUS to deny the injunction. They argued that there is no reason to believe that the counties are not following previously issued guidance around setting aside and separately counting the ballots arriving later, and that SCOTUS already did not block the extension ruling by the lower court. What’s more, where the SCOTUS order required compliance with the earlier guidance from the secretary of state, all county election boards in PA were re-informed of that guidance and the demand for compliance, according to the state’s attorney general.

SCOTUS has not responded. In the meantime, Ohio, Missouri, and Oklahoma, all states that went to Trump this last go around, have filed amicus briefs voicing interest in how SCOTUS will proceed in its review of the PA court ruling. These other states side with the GOP.

Wisconsin’s vote canvassing deadline is coming up Tuesday. Once that is completed, a recount can be requested. It remains to be seen if Trump will petition for, and finance, one, as it may cost millions.

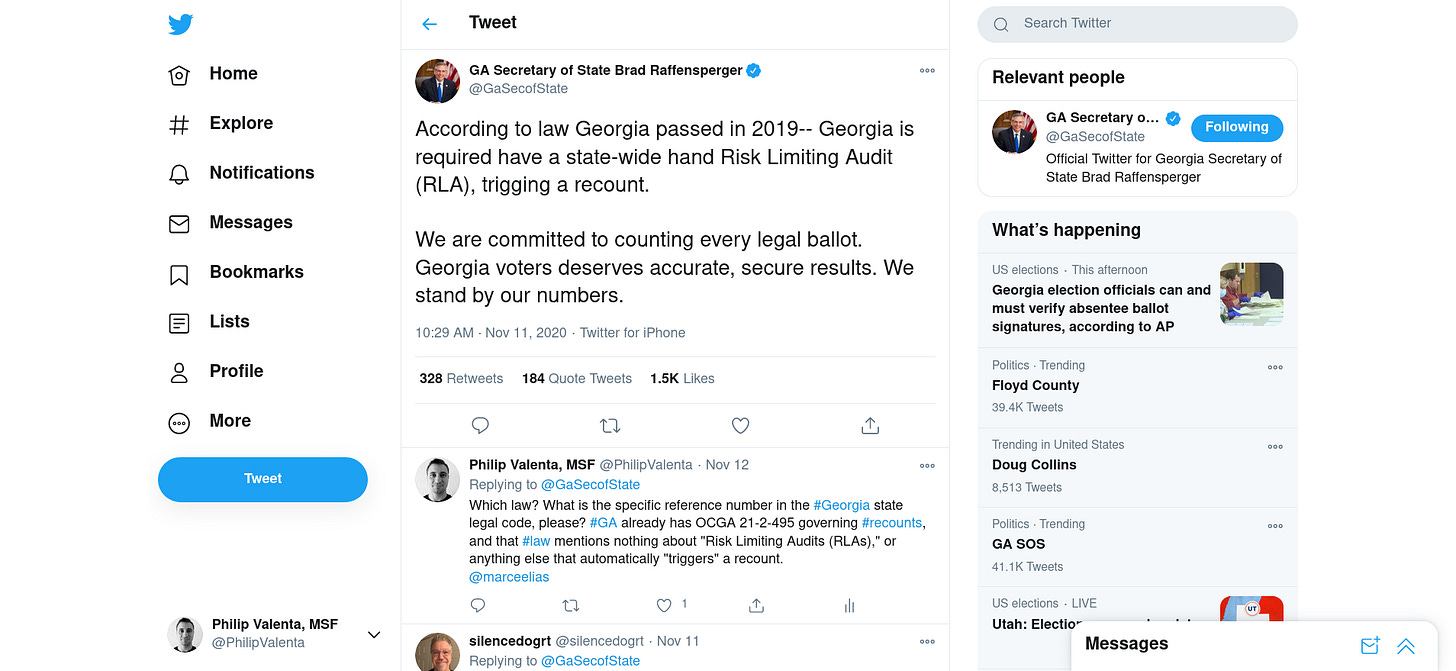

Georgia has begun a recount of all ballots by hand. As outlined in last week’s issue, the move began unfolding when Secretary of State Brad Raffensperger gave a press conference and stated unequivocally that there would be a recount. News agencies repeated the statement, in some cases presenting misinformation that under certain circumstances, this is an automatic process. Days later on Twitter, the secretary of state vaguely mentioned a “law passed in 2019” that details the circumstances for when an automatic “Risk Limiting Audit” is required, and how it “triggers” a full recount.

Strangely, the state already has a section in its legal code governing recounts. O.C.G.A. § 21-2-495 clearly sets forth that a recount may be requested by the losing party in an election if the margin of difference in votes is 1/2 % or less. The request is to take the form of a petition that presents the case for the recount. the law makes no allowances for any automatic recounts whatsoever.

The state’s “superintendent” may also make the case for a recount, but must describe the possible error or discrepancy that is being addressed. While Raffensperger mentioned more than once that there would be a recount and that they believe there was some issue here or there, no Georgia state authority has detailed what that issue is.

Even stranger, Raffensperger has not responded to any direct questions on Twitter over the existing law, the 2019 law he referred to, or the issue, and now, the original source of O.C.G.A. § 21-2-495, once hosted on LexisNexis, is unavailable. All that remains at the moment is an archive of the legal code’s page taken November 7, 2020, as well as Raffensperger’s tweets.

All this means that the path to the Biden White House is not unfettered. Thus, we cannot yet expect to see market action related to fiscal stimulus and new leadership that is unfettered, either. One may increasingly place their bets that the presidential transition will, in fact, take place, but in some form, it’s still a bet. Tread carefully.

Holy vaccine. There was no way with those kinds of preliminary results from the Pfizer-BioNTech partnership that price action wasn’t going to surprise to the upside. Except for limited corners of the markets, assets reacted very strongly in a manner highly positively correlated with the news.

In short, the study by the partnership that took no money from the US government for any part of the operation (not even manufacturing), is finding that their vaccine reduces a larger percentage of infections in a particular subset of the population than was originally anticipated, or 90%. Popular consensus prior to the news anticipated 60-70%.

It seems too early to celebrate, though; we may still have a bit to wait. Here then, we also do not have reason to expect an ongoing rally. The gradual decline of the pandemic will come about, but the endgame may not be linear in nature. For the time being, we are still very much in the midst of it. Cases and deaths are only increasing, with various states and other countries resuming business closures and re-instituting stay-at-home orders.

These are just some of the considerations to keep in mind regarding the vaccine:

The Pfizer-BioNTech vaccine trial has not ended. The bulk of the study’s participants are awaiting their second double dose. Recipients of the vaccine are given a double dose to begin their vaccination, then a second double dose three weeks later to conclude it, which in the study’s case, is the third week of November. The study is bigger than was originally planned, and obviously there is a great deal of data to collect yet in order to fully understand the results. Nothing has been peer reviewed nor confirmed. Hence, we must wait to see what the final results actually are. Will it still be a 90% reduction in cases among a particular subset of the population?

Thereafter, Pfizer will seek emergency FDA authorization. Will it be granted?

We have the logistics of vaccine manufacturing and distribution to contend with. On Pfizer’s own website, the company states 50 million units will be made globally available this year. That is presuming the study terminates well and emergency authorization is granted by the FDA. We imagine that the United States will receive some of those doses, but that they will go to certain members of the population before others, such as first responders. Even tens of millions of doses is but a small percentage of the country’s population. Those doses will probably not reach the general public this year.

The partnership is scheduled to produce 1.3 billion doses globally next year. This, again, is a fraction of the world’s population, spread out over the entire year. It’s true that there are other companies like Moderna that may produce highly effective vaccines as well, so we may get to a large reduction in cases and deaths next year through some combination of products. Then again, it could be 2022 before we build that momentum, making next year a continued challenge economically as well as health-wise.

That particular subset of the population in which the study has seen a 90% reduction in the incidence of COVID-19 cases is “participants without evidence of prior SARS-CoV-2 infection.”¹ What about everyone else, including the so-called long-haulers, those who are getting infected now, and those who may become reinfected?

How long will immunity last for?

Nonetheless, the markets have been eating up the news. Notably, it was the Dow that popped the most last Monday. Globally, it is estimated that some $2 trillion in trades were made across various markets. The S&P climbed, yields jumped, oil rallied. There seems to be a case for how every asset will be helped by a vaccine moving us closer to the light at the end of the tunnel. Junk bonds, emerging markets, you name it. To put it concisely, it allows investors to imagine “normalcy” again and move to more of a risk-on position.

Tech, however, slumped. One argument is that there will be less need for tech as people supposedly resume lives that are more “in-person” and less on screen. This is shaky logic, at best.

The pandemic will get worse before it gets better. We have been accumulating confirmed COVID-19 cases at a startling pace, and that is highly likely to mean many more fatalities in the coming weeks and even months. We still have no focused leadership around the issue, no national mask mandate, no plan. (Well, we have whatever has been proposed by Biden-Harris, but they don’t represent the current administration and the transition is being blocked.)

Additionally, there are reasons to believe that our reliance on, and love affair with, tech is only growing. The pandemic has already accelerated adoption of AI and automation to replace more vulnerable human employees or fuel productivity. Companies like PayPal have added millions of net new accounts and performed a record number of transactions. Plus, tech keeps innovating. Think VR sets.

To add to this, there’s no guarantee that people’s habits will revert to a pre-pandemic state. A new tech-heavier norm may be in place. An example of this might be digital streaming. Who’s to say that digital streaming subscribers will give up their subscriptions, or that producers won’t keep releasing direct to subscriber films (or come up with some other way to maintain and grow their customer base)? Connecting viewers to that creative output requires tech. It makes more sense at this point to worry about movie houses, not tech companies.

Regarding the workplace, one example is online meetings. More people are familiar with them than ever before, making the decision to continue employing them—as opposed to an in-person business meeting that may involve expensive travel—an easier one. On a different note, for some employees such as mothers, online meeting culture has helped level the playing field somewhat. Employers, meanwhile, have diminishing reason to continue to value these employees and their contributions less, or see them as risky, or not accommodate them.

Gold, for its part, collapsed last Monday. With some of the election turmoil moving into the rearview every day that passes and the clearer visualization of an actual vaccine that could come through for at least a portion of the population, the rationale for investing in it is fading. (Yes, while the GOP is launching lawsuits around the election, it will remain elevated, though.)

Oil, on the other hand, got a big boost from the vaccine news. However, it’s an industry that’s going to have to work very hard to survive, even with an effective vaccine in place. There is no indication that it will ever recapture its former glory. The United States uses the most petroleum in the world, and again, 68% of that is use is for transportation. If the American consumer continues to move toward electric vehicles (which is the biggest trend counting against the industry) even if nothing else changes, demand may stay slashed by millions of barrels per day moving forward.

Finally, with a vaccine, some have already begun speculating that there would be less need for fiscal stimulus. This is simply dangerous. If anything, the economy needs to be cushioned, not fed a starvation diet, including aid for states. Other nations in much better shape pandemic-wise continue to support and accommodate, rather than not, like China.

All the same, the White House has stepped back from the stimulus debate, and with an incomplete election cycle, circumstances have left stimulus negotiations in a lurch.

[tracking: SPY, VTI, QQQ, XLK, EDC, VWO, VXUS, LQD, VXX, XLE, TMV, GLD, VB]

Certain Federal Reserve officials believe that Fed policy is right where it should be. However, it is still questionable whether it is doing enough to get the word out on its Main Street Lending program, for instance.

On other fronts, the Fed is looking to join its peers in fighting climate change through the Network of Central Banks and Supervisors for Greening the Financial System (NGFS). It has now officially listed climate change as a threat to financial stability.

Otherwise, the central bank continues to express concern over the path the pandemic is taking in this country.

Initial jobless claims in the US fell to 709k. This is a decent drop from the weeks when we were consistently above 800k, but then again, we remain above 700k. What’s more, there appears to be a dire tradeoff: fewer jobless but more sick after they return to work, possibly out of desperation over their financial situation.

To add to this, 298k+ more people applied for PUA, down from 362k the week prior.

[tracking: SPY, VTI]

Mortgage applications fell for the week ending November 6, with those for home purchases outstripping any slight gain in refis.

JP Morgan is relaxing mortgage lending standards. If housing really has become a bubble, such action on the part of the banking industry would help fuel said bubble.

Building on previous weeks’ newsletters, the real estate thesis here is that the housing market will enter a period of decline as labor weakness continues and the pool of qualified buyers at current prices, especially, is exhausted. This diminishing pool could be part of the reason behind JP Morgan's easing of lending curbs, by the way.

The downturn in commercial real estate will persist as malls continue to fail and businesses yield office space, among other things.

At the same time, the Fed will try to absorb souring packaged mortgage debt securities.

[tracking: XLRE, NLY, VNO, SPG]There have been calls for the S&P 500 to breach 4k following news of the vaccine. This is in keeping with the S&P inflation scenario discussed earlier this year.

Sovereign matters:

Fitch began covering the UAE, rating it AA- with a stable outlook.

Fitch revised downward Saudi Arabia’s outlook to negative, due to fiscal and balance sheet weakness induced by the pandemic, which has of course hurt oil-rich economies.

Moody’s revised down Guatemala’s outlook, citing the country’s increasing debt load, low revenue stream, and government’s limited capacity to address challenges.

S&P downgraded the Bahamas, citing the impact of the pandemic. No doubt this is due to the blow to tourism.

While countries left and right experience ratings downgrades, Mexico has so far bucked the trend. Fitch maintained its rating of the country’s sovereign debt at one notch above junk.

Zambia effectively entered into default by not seeing to a eurobond coupon payment. The country already missed a dollar-denominated interest payment on another bond in October. Creditors have refused to accept deferral as an option.

Argentina is seeking an extended fund facility from the IMF to replace failed debt. Such a move usually means that a country is willing to accept even stricter parameters in areas like reforms. Argentina’s creditors certainly wish to see stringent requirements put in place by the IMF in a bid for extra protection, given how many times the country has defaulted/restructured its debt. Simultaneously, a bill is being floated in government that would give Argentina’s Congress final say on foreign debt deals. It’s unclear whether this would better align the needs of the various parties involved or complicate matters more.

New Zealand, the envy of the progressive white world… It has stiff-armed SARS-CoV-2, charmed foreigners with a sheen of sheer humanity, and its economy is in better shape than it could have hoped. The government continues to embrace accommodative measures to cushion the blow from the pandemic, including delaying requirements for increased capital reserves at banks and launching a new program to encourage lenders to make more loans.

Peru is devolving further into political turmoil. Most recently, President Vizcarra was forcibly removed from office by the nation’s Congress.

Foreseeing an ongoing need, the G20 has agreed on a plan to facilitate the orderly restructuring of government debt in a pandemical world. For the first time, it standardized a framework to be leveraged, no matter the creditor and debtor nations involved.

The ECB will maintain QE programs. Lagarde and others do not seem to be of the opinion that we are soon to be out of the woods.

China still appeals greatly to investors, but surprise defaults by state firms have some fearing contagion.

The Swiss see the drag of the pandemic persisting for a while.

The European Investment Bank will be spending $1 trillion on climate-focused projects aligned with the Paris agreement.

The UK will offer its first green bond next year. This comes after the announcement midway through October that the Bank of England will require companies to disclose their climate related risks such that they can be priced in.

[tracking: EDC, VXUS, VWO]

The Bank of England is not enthusiastic about stablecoins, but it is taking the stance that it doesn’t exist to ensure that commercial banks are protected from cryptos. Apparently, some fear that traditional bank deposits will dry up as part of the customer base shifts to storing its wealth in digital wallets that banks have nothing to do with.

Footnotes

¹ “Pfizer and BioNTech Announce Vaccine Candidate Against COVID-19 Achieved Success in First Interim Analysis from Phase 3 Study | Pfizer.” 2020. Pfizer.com (November 9, 2020).