10092020 :: Friday finance week in review

A partial digest of what we learned:

There is still no agreement within the political establishment of the United States over further stimulus measures or safety nets for the general public, industry, or the country’s municipalities and states. First, Trump returned from Walter Reed and called off negotiations. He then seemed to engage in attempted vote buying with the general public, only to thereafter seek to provoke Pelosi into piecemeal stimulus (another round of $1,200 checks). Pelosi and Mnuchin resumed talks, with the White House signaling it would again be open to a more sizeable package, although Trump on his own said he would prefer a “skinny” pandemic aid package (checks to households, aid to airlines, something to that effect). The latest? The White House proposed a larger package than before (from $1.4 up to $1.8 trillion), though not quite up to House Democrats’ $2.2 trillion.

Here’s the deal: everything hinges on fiscal stimulus, the form of stimulus produced by the federal government. What’s more, the majority of the United States will be better off with a “blue wave” victory, i.e. a sweeping Democratic win.

Why? First off, the packages the Democrats wish to release are invariably larger than those offered by Republicans, as well as more inclusive. On all fronts, a large package that reaches more corners of the economy than not will boost all facets of the economy to a greater degree. This goes for stock and commodities markets, for the wellbeing of households and marginalized groups, for existing corporations and smaller businesses, for the employed as well as the furloughed, underemployed, and unememployed.

You cannot withhold or minimize financial support in the midst of a once-in-a-century global health crisis and expect things to turn out well.

Secondly, there is more certainty to be regained in all areas and dealings—political, fiscal, or otherwise—with a Democratic sweep in terribly uncertain times. Certainty is something that many in trade and industry and beyond still prefer. Trump is not a purveyor of certainty, but rather the erratic.

Certain Federal Reserve officials, meanwhile, are themselves calling upon the government to provide more aid and indicating that they look forward to tapering off the massive asset purchases the central bank has undertaken, once the pandemic begins to ease. Their form of stimulus has served its purpose and is increasingly limited in its efficacy. To do more is to welcome diminishing returns and weaken the structure of the American economy. As Kaplan of the Dallas Fed has stated,

I don’t think it’s healthy for the markets to be addicted, or too reliant, on Fed presence ... it engenders fragilities.¹

The Fed is limited in its capacity to help, and has acknowledged that. The federal government, on the other hand, is not thusly limited. It can issue checks to households. It can offer loans to businesses. It can grant direct aid to struggling sectors. It can provide the Fed with capital that can then be leveraged to increase its size and scope and further support the economy in ways the Fed has within its charter to do.

One could have a bountiful meal composed of all the red herrings around providing further stimulus that have flooded communication channels:

The solvency of the US government is at risk should more stimulus be provided

Stimulus discourages people from working altogether

We would just be bailing out “corrupt” and “mismanaged” blue states

COVID-19 fatality rates are low, ergo reopening sans restrictions is in order/best for the economy

On this latter point, in between hospitalization and not, in between death and life, there is an entire range of experiences of COVID-19 that are being glossed over. Business and school employees are home sick in droves, portions of entire departments too ill to be at their respective workplaces, leaving just a few to carry on in their absence in any given situation. Government employees the same, as evidenced by the spate of White House, congressional, and military infections publicized most recently, should one have any doubts.

Some classrooms are emptying as students become infected in groups. Meanwhile, those who are not themselves the most vulnerable in our society may have someone in their lives who is, and they may act accordingly. Finally, some may simply not wish to test their luck, and who can blame them.

Nobody needs to be hospitalized or die in order for there to be economic impact as a consequence of all this. Yet some are also requiring hospitalization, and some are losing their lives, on top of it all. Infection by SARS-CoV-2 remains a game of Russian roulette, if nothing else.

This is a health crisis with a novel virus at the center of the vortex and no vaccine, no cure. We cannot force optimal workplace or national productivity in times of sickness and under duress. If an assembly plant relies on dozens of skilled fabricators and many are home sick because they need to rest and recover, if only so that they can do their best work and not screw anything up, then the assembly plant will be assembling less, for the time being. If that keeps occuring because we are not containing SARS-CoV-2, then there is a chance the assembly plant will eventually need to furlough employees. At that moment, the solution is not to withhold or minimize aid, neither to the assembly plant nor to the households of those furloughed workers.

The struggle at hand with stimulus, then, is this: Serve the most interests in a humanizing manner, or serve a select few? It is the opinion here (and elsewhere) that we serve the most, in which case, prepare for rising price action. Otherwise, with little to no further aid and a Republican victory in the national election, prepare for a major leg down and greater hardship.

[tracking: SPY, QQQ]Initial jobless claims continued to exceed 800k for the sixth consecutive week (this latest ending Oct 3, 2020). They keep pouring in.

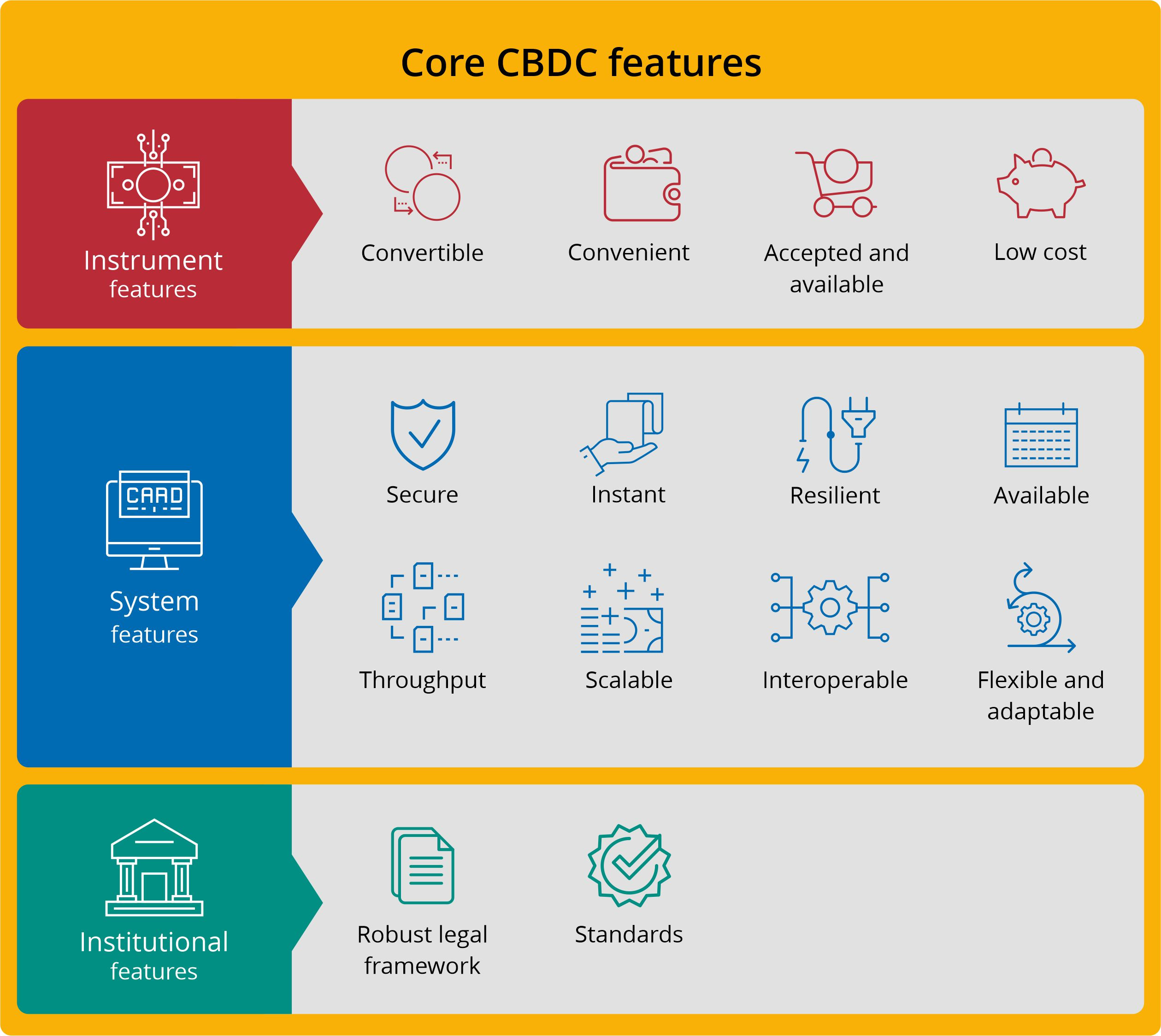

A report from the Bank of International Settlements (BIS) has forwarded key criteria for central bank adoption of digital currency issuance. Cryptos must not be destabilizing, must not seek to replace legal tender, and must not be expensive to utilize, among other things.

Gold has breached $1,900/oz again, while silver has broken through $24/oz. Despite this most recent runup, their performance remains underwhelming with prices well below August highs. One of the only remaining drivers for higher valuations may be total election chaos in November, which is not guaranteed.

The opinion here remains that the next major wave for the precious metals complex is down.

[tracking: GLD, SLV, DUST, JDST, GDX, GDXJ]The future of housing hinges on the employment picture improving to pick up the slack left by the exhaustion of resources of people who are moving because of climate crises, or white flight (COVID-19, civil unrest), or to better accommodate their remote work lives. In the intermediate term, we may be headed into a supply glut as construction is still on a tear and will most likely overshoot demand. Over the very long term, there may be an end to housing as climate disasters drive people away from ownership of a stationary asset that will possibly have become continually at risk of destruction by this or that climate event.

Watch for things like falling mortgage applications for home purchases (not refis) and a growing monthly supply of houses in the US.

[tracking: XLRE, NLY, VNO]ESG (environmental, social, and governance) is the new hot ticket in debt, the market having just eclipsed $1 trillion in notional value. Sustainable finance is alive and well, and growing. The University of Toronto is the latest large-scale investor in ESG credit.

Sovereign matters:

India signals that it will be easing further in the face of increasing economic headwinds and inflation that precludes it from cutting rates.

UK financial regulators are telling their own finance industry to brace for a messy no-deal Brexit. In particular, the concern deals with whether UK firms and EU clients will still be able to engage in the smooth trade of financial instruments, including stocks and derivatives.

Japan may begin early stage tests of a digital currency issuance, in order to keep pace with global central bank interest.

Bloomberg sees emerging markets recovering sooner and more robustly than developed ones, including the United States. It is the opinion here that emerging markets offer more upside than the domestic market moving forward for the foreseeable future, and valuations are currently more reasonable, yet.

[tracking: EDC, VXUS, VWO]

Globally, we have exceeded 1 million COVID-19 fatalities (and counting). The United States continues to outpace the rest of the world in COVID-19 infections and deaths, never mind the Americas. Russia tops Europe in infections, Iran the Middle East, India Asia, and South Africa Africa.

Footnotes

¹ Saphir, Ann. “Fed’s Kaplan Rejects Adding to QE, Eyes Eventual Taper.” Reuters (October 9, 2020).