04092021 :: Friday finance

A partial digest:

Friday was day 80 of the Biden-Harris administration. Among the executive orders is one to establish a presidential commission examining SCOTUS. The commission will, along with other things, provide the following:

(i) An account of the contemporary commentary and debate about the role and operation of the Supreme Court in our constitutional system and about the functioning of the constitutional process by which the President nominates and, by and with the advice and consent of the Senate, appoints Justices to the Supreme Court;

(ii) The historical background of other periods in the Nation’s history when the Supreme Court’s role and the nominations and advice-and-consent process were subject to critical assessment and prompted proposals for reform; and

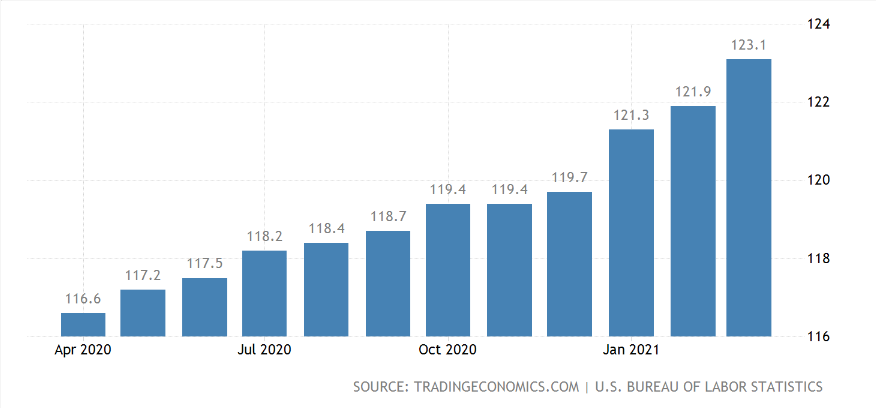

(iii) An analysis of the principal arguments in the contemporary public debate for and against Supreme Court reform, including an appraisal of the merits and legality of particular reform proposals.Producers are reporting higher priced inputs in various countries, including China and the United States.

Inflation, inflation, inflation is all anyone can seem to discuss. Again, we already have siloed inflation, in that there are many isolated cases of it due to supply shocks as the global population cannot stay healthy enough to produce at rates prior to the pandemic.

However, even if siloed inflation gives way to systemic inflation at some point for the US, the Fed may still not get what it wants, unless it is sustained. Again, the Fed is actively seeking sustained inflation, not trying to avoid it.

In that case, equities and energy, as stated multiple times here in the past, are historically the most proven hedges of systemic inflation. Gold has never reliably hedged anything, and there isn’t any hard data on crypto, though some believe it may shine in inflationary environments. Only time will tell.

With the above in mind, crude finished down while US equity indices recorded new all-time highs. In fact, the vast majority of equity indices the world over are up YTD. That may end up speaking for itself.

The oil and gas industry, on the other hand, is complicated by structural economic shifts toward clean energy, OPEC+ plans to increase output starting in May, pandemic lockdowns, surges in infections, and vaccine issues.

[tracking: SPXL, VTI, QQQ, XLK, XLE, MCHI]Quick wrap:

All of the vaccines being employed in the fight against SARS-CoV-2 are under investigation for various reasons, including blood clots in the brain and precipitous drops in platelets resulting in a rare blood disorder.

In spite of insistent talk of inflation, yields finished down for the week.

Simultaneously, the DXY declined to slightly above 92.

Not one to be left out, crude finished down for the week, as well.

CALL: No change; near to semi-intermediate term, prices could rise further given supply shocks, OPEC+ micromanagement, inflation expectations, "recovery," and more fiscal spending, among other things. Longer term, it's a dying industry.[tracking: XLE, GUSH, DRIP]US indices, however, notched new all time highs.

Total crypto market cap is nearing $2 trillion as of publication.

Gold finished up by Friday close, but not by much. It remains sub $1,750.

CALL: No change; expecting ever-lower valuations moving forward. Looking for an eventual floor around $1,200/oz.

Initial jobless claims rose yet again to 744k (SA) for the week ending April 3 from a upwardly revised 728k for the week prior. One year ago, we saw over 6.1 million. To repeat, we are now in the one year ago timeframe when the US began to feel the brunt of the pandemic.

The four week moving average remains over 720k.

To add to this, almost 152k on an unadjusted basis applied for PUA, down from the previous week’s downwardly revised 237k+.

As of March 20, over 18.1 million people (UA) were still claiming unemployment benefits of some kind, down only about 52k from the week prior. In the comparable week one year ago, the US witnessed more than 3.4 million people claiming unemployment insurance from all programs together.

UI benefits programs saw a mix in continued claims for the week in question from the week prior. The PUA and PEUC programs saw the biggest jumps in continued claims.

These remain unsettling numbers, to say the least.

Mortgage applications decreased a blended 5.1% (SA) for the week ending April 2, due to a decrease of 5% in refis and 5% in homebuyer applications. ARM activity rose to 3.7% of all applications.

The release once again neglected to mention the average loan size across purchase applications. MBA’s choice for a 30Y fixed benchmark increased to 3.36%. The simple national average as reported by Freddie Mac (via FRED) for April 8 was 3.13% on the 30Y fixed, down from that reported last week.

At the same time, the forbearance rate as of March 28 fell slightly to 4.90% as more households made their exit in one way or another. Exits, the good, the bad, and the ugly, are picking up as we mark one year plus of being beset by the pandemic in the US.

Forbearance extensions and re-entries increased this last go around, as did loan/trial loan modifications and deferrals/partial claims. Finally, the group that continues to make their monthly payments during their forbearance period shrunk again.

2.5 million households remain in a state of mortgage forbearance, and the flow of mortgage credit keeps rising as loan providers try to keep the good times rolling, even at the risk of low credit scores and high LTV ratios.

CALL: No change; housing weakness inbound. For the call to reverse, labor conditions would have to consistently improve, among other things. Again, a giantinfrastructurebill might help.[tracking: DRV, XLRE, SPG, VNO, WPG, NLY]

Used car trends: The latest Carvana car count as of April 9 rose 1.10% to 33,888 vehicles from 33,520 the week prior. Meanwhile, the CarGurus average price index continued rising, this time by 1.22% to $23,305 from $23,023. This is the highest average price registered since said data collection began for this newsletter in November of last year.

Sovereign matters:

Rising Treasury yields may threaten the sustainability of dollar denominated debt worldwide, as may the strength of the $USD. On the one hand, yields would increase borrowing costs through higher interest payments, while a strong $USD would make it more difficult for certain nations to maintain sufficient forex reserves and keep their own currencies from inflating. Furthermore, ascending Treasury yields may once again make US sovereigns more appealing over emerging market debt. Yields in some other countries appear to be following those in the US upward since roughly August of last year.

Kenya secured an IMF assistance package to the tune of $2.3 billion over three years.

S&P Global downgraded Morocco on account of the nation’s economic contraction and growing debt. The ratings agency does not expect the country to effectively consolidate its budget until at least 2024.

[tracking: MCHI, EDC/EDZ, VWO, EWU, IEV]The current state of equity: Shots in Florida intended for marginalized groups are going to wealthy whites.

During the pandemic alone, the US has witnessed 204,261 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. This equates to an average of 440 people per day since the start of 2020. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 560,486, puts the probable COVID-19 death figure somewhere north of 660k.

Across all causes of death, we suffered 118% of the deaths in 2020 that we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.1

When the average of pneumonia deaths per day begins to decline significantly and consistently, perhaps we'll be able to start saying that we might be gaining the upper hand on SARS-CoV-2. We’re not there yet.

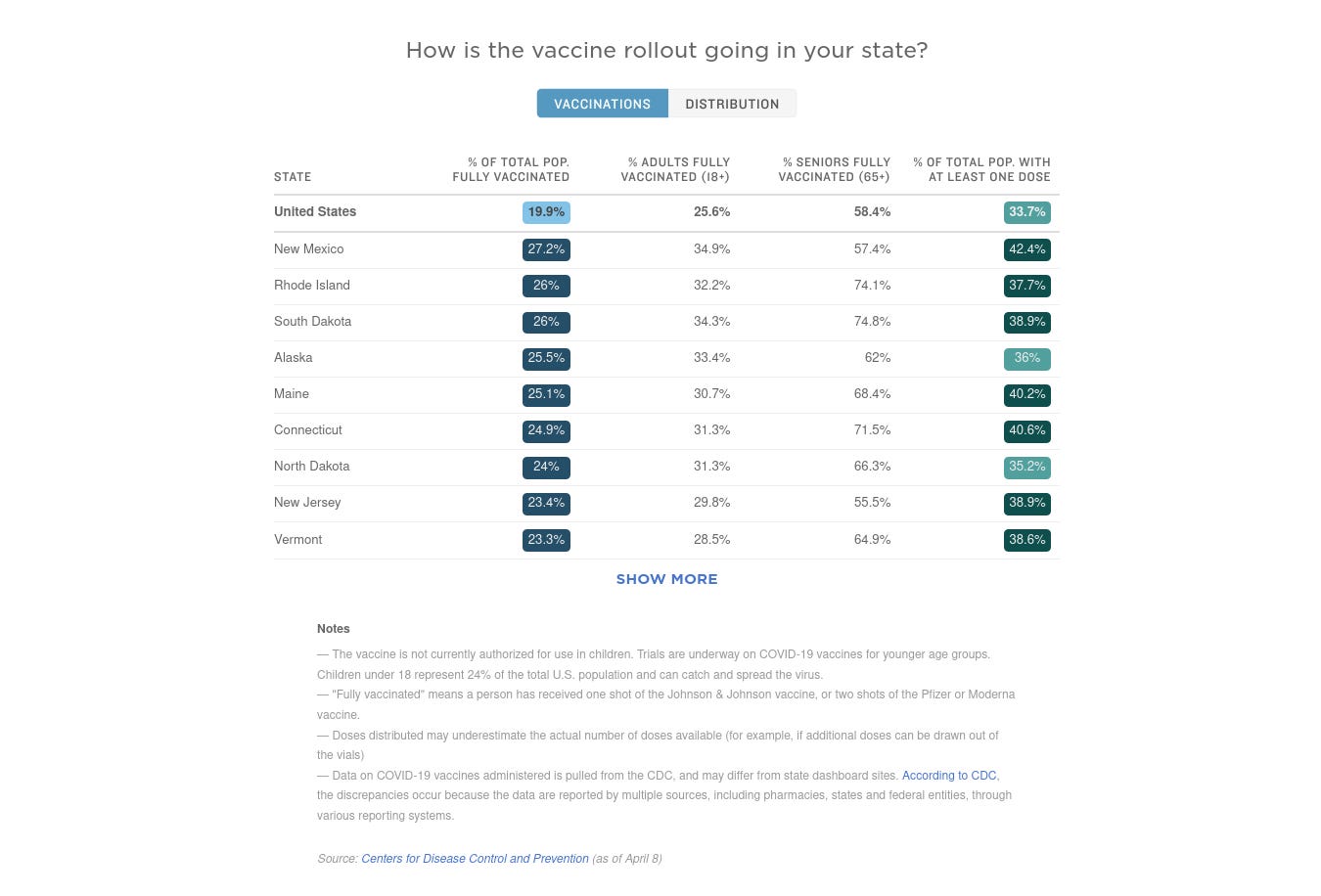

NPR reports that some 19.9% of the population in the US has been fully vaccinated, up from 16.9% last week. The vaccination rate was roughly 2%/week for a couple of weeks, and now appears to be accelerating further to 3%/week.

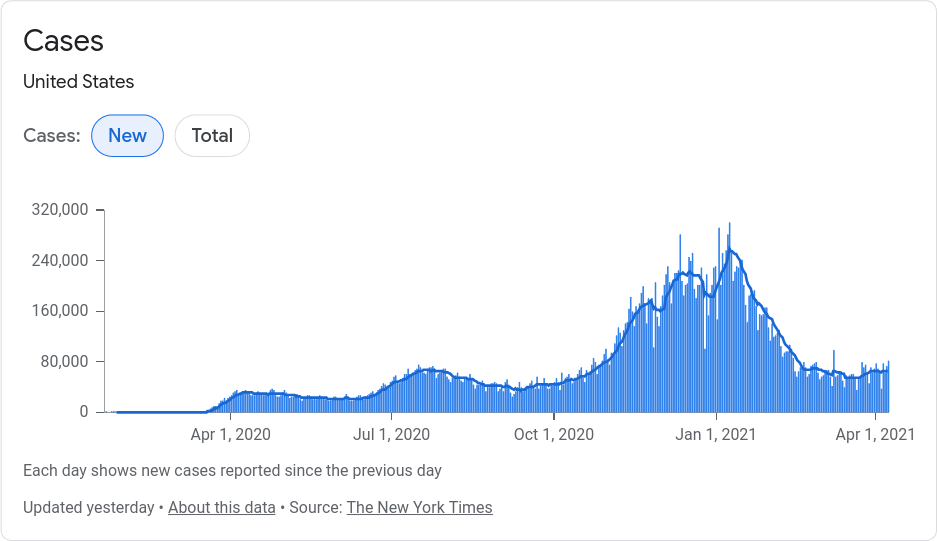

However, daily infection case loads jumped considerably from last week, exceeding 80k in one day for Thursday, April 8, whereas in the prior week, one day loads were more like 60k+. Deaths follow infections.

Footnotes

Valenta, Philip. “Death by COVID-19 Hides in Plain Sight.” HedgeHound (June 29, 2020). The research includes the full methodology behind the figures presented here every week, as well as information on historical pneumonia trends and death categorization in the US during the global pandemic. It was last updated on December 4, 2020.