03192021 :: Friday finance

A partial digest:

Friday was day 59 of the Biden-Harris administration. Stimulus checks are quickly making their way to recipients. CNBC reports that roughly 90 million checks landed in bank accounts as of March 17.

Make no mistake, SARS-CoV-2 is still spreading, vaccinations or no.

Quick wrap:

Oil volatility has returned.

Gold has bounced back somewhat, though it’s still splashing about in the shallow end of the $1,700s.

Crypto keeps bouncing and retracing, bouncing and retracing. Total market cap is $1.74+ trillion as of publication.

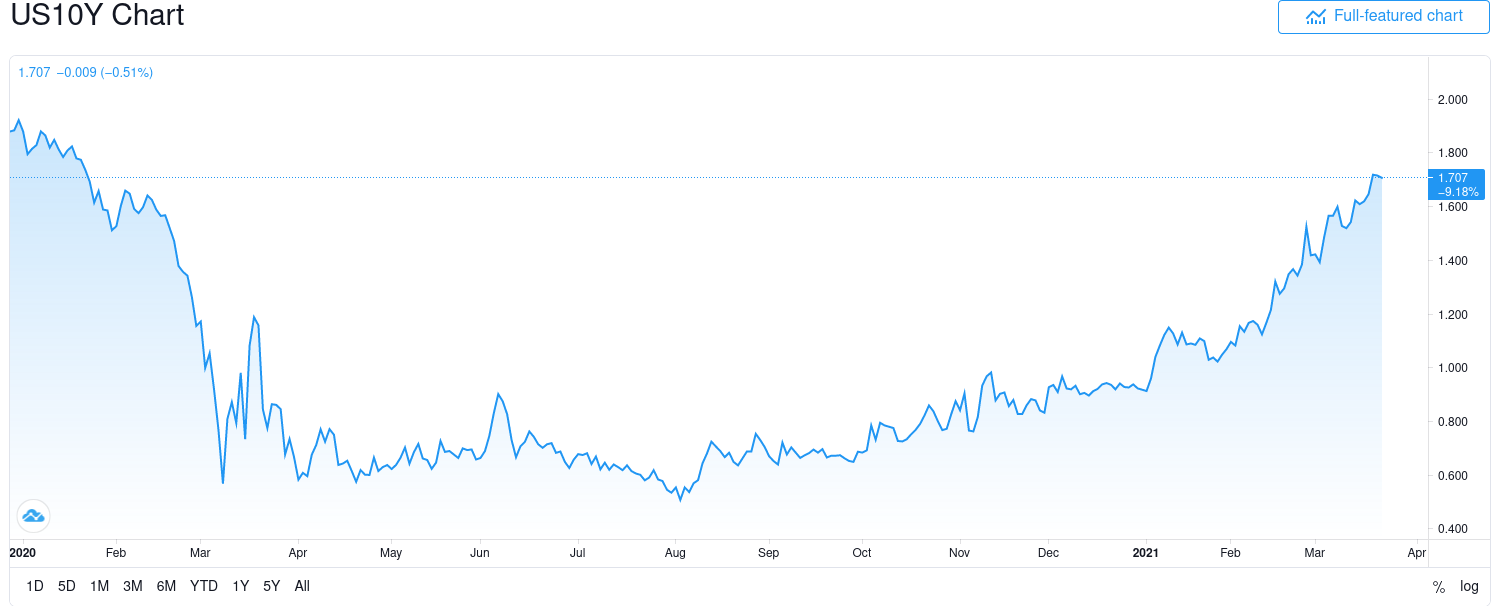

Yields climbed quite a bit, finishing at 1.72. There does appear to be concern over borrowing costs, evidenced by Corporate America switching over to fixed rate debt to fund itself.

The DXY is the real trooper here, approximating 92.

Companies like Annaly Capital Management [NLY] dealing in mortgage-backed securities have exhibited appealing stability in these tumultuous moments, all while still offering outstanding dividend payouts. MBS are some of the only instruments the Fed is still gobbling up every month, especially since their special acquisition programs in partnership with Treasury ended last year. This looks like a different flavor of the Fed put.

The Fed has failed to soothe anyone on yields, but that may not be the point. If traders don’t believe the Fed can steer the ship and they’re betting against the monetary authority, the selloff in US Treasuries may continue and yields will continue to climb, accordingly.

Source: TradingView That is, unless the Fed implements yield curve control. At this time, there is no indication that they will do that.

Initial jobless claims jumped to 770k (SA) for the week ending March 13 from an upwardly revised 725k for the week prior. One year ago, we saw 282k. Note that quite often, the previous week's figures are being upwardly revised. Also, we are entering the one year ago timeframe when the US began to feel the brunt of the pandemic.

To add to this, more than 282k on an unadjusted basis applied for PUA, down from the previous week’s upwardly revised 479k.

As of February 20, more than 18.2 million people (UA) were still claiming unemployment benefits of some kind, down some 1.9 million from the week prior. In the comparable week one year ago, the US witnessed closer to 2.1 million people claiming unemployment insurance from all programs together.

Across the board, UI benefits programs saw decreases in continued claims for the week in question from the week prior.

(A reminder that UI eligibility has now been expanded under the Biden-Harris administration. This will involve the retroactive payment of benefits to claimants who were faced with a “devil’s bargain” of returning to work in spite of concerns over safety in the midst of a pandemic, or declining some level of employment—and therefore income—with no recourse. The expansion falls within the PUA UI benefits program structure, and its administration will be handled at the state level. Claims should be filed with a person’s local benefits office.)

Mortgage applications decreased a blended 2.2% (SA) for the week ending March 12, due to a decrease of 4% in refis and in spite of a 2% increase in homebuyer applications.

The report once again neglected to mention the average loan size across purchase applications. MBA’s choice for a 30Y fixed benchmark came in higher at 3.28%. The simple national average as reported by Freddie Mac (via FRED) for March 18 was 3.09% on the 30Y fixed.

At the same time, the forbearance rate fell slightly to 5.14% as some households made their exit in one way or another. Exits, the good, the bad, and the ugly, are expected to pick up now and into next month as we mark a year of being beset by the pandemic in the US.

Of concern is that the relative number of households extending their original forbearance periods grew, while those continuing to make payments in these days of forbearance shrunk. Moreover, the percentage of households that missed payments, and are now exiting forbearance without a plan in place, rose.

An anecdotal note on commercial real estate: Ford Motor Company is moving to indefinitely permit 30,000 employees to work from home, if they so choose. That's just one company based in one country in the world. A slew of companies across the globe are making such decisions. They are also reaching conclusions, such as that they can save money on real estate and get more out of their employees. And what about all the ancillary businesses and services; what of their fates? These developments fundamentally change the landscape. While some equilibrium will once again be established some day, we are still out on the highway. None of this spells light switch recovery.

[tracking: NLY, XLRE, DRV, SPG, VNO, WPG]

Used car trends: The latest Carvana car count as of March 21 dropped 0.90% to 36,616 vehicles from 36,949 the week prior. Meanwhile, the CarGurus average price index continued rising by 0.50% to $22,729 from $22,615.

Sovereign matters:

Moody’s has revised upward Vietnam’s credit outlook to positive on account of the nation’s concerted effort to monitor and set aside for its debt obligations in advance. Furthermore, Vietnam is coming into its own as a major global trading partner, while the government is focusing more on tax compliance and other fiscal consolidation measures, among other things.

Moody’s has revised upward Mongolia’s outlook to stable due to reduced debt obligations stemming from multilateral lender assistance and refinancing. Additionally, things like more secure sources of funding and growing forex reserves bolster the country’s outlook.

FDI keeps pouring into China.

[tracking: EDC/EDZ, VWO, EWU, IEV]

The current state of equity: How “‘tax policy adds insult to injury’ by magnifying the financial toll of Blackness.”

As of the CDC's March 19 update, the US had witnessed 195,507 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per excess deaths data. That’s an average of 438 people per day since such data reporting began early last year. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 541,760, puts the probable COVID-19 death figure somewhere north of 640k.

Across all causes of death, we’ve suffered 118% of the deaths in 2020 that we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.1

When the average pneumonia deaths per day count begins to decline significantly and consistently, perhaps we can start to say that we might finally be gaining the upper hand on SARS-CoV-2.

NPR reports that some 12.6% of the population in the US has been fully vaccinated, up from 10.3% last week. The vaccination rate is on the rise.

An increasing vaccination rate notwithstanding, we stand to lose ground we’ve gained on SARS-CoV-2 as location after location drops any precaution-related mandates. Also, spring break is now in full effect.

Footnotes

Valenta, Philip. “Death by COVID-19 Hides in Plain Sight.” HedgeHound (June 29, 2020). This research includes the full methodology behind the figures, as well as other details regarding death categorization in the US during the global pandemic. It was last updated on December 4, 2020.