02262021 :: Friday finance

A partial digest:

Friday was day 38 of the Biden-Harris administration. Presidential actions included an executive order on America’s supply chains.

The stimulus vote took place in the House and the $1.9 trillion package cleared this initial hurdle. Next, the Senate, where some anticipate it will be stripped of the provision increasing the minimum wage to $15/hr. Whatever version the Senate ends up with and [possibly] passes will be sent back to the House for a new vote. If all goes well, it will then be sent to Biden’s desk. As the wrangling continues, the markets will behave accordingly.

Equities and the economy can’t go much higher from here without further government assistance. Otherwise, our recovery prospects at this time seem as overblown as ever, vaccine rollout or no.

A brief note on yields: Rising yields do not represent inflation. Right now, rising yields reflect a lack of demand for the bonds themselves, and snowballing selling activity. Much in the same way a stock rout can feed on itself, so can a bond rout. It still doesn’t mean inflation is around the corner. However, a bond rout may present challenges, especially as Treasury yields are used as reference rates or inputs for rates on a host of credit vehicles for everyone from the average consumer to the large corporation.

Some are pointing at convexity hedging to help explain the large moves in Treasury rates. It’s worth considering for what it might say about perceptions of where real estate is heading.

Gold: Look out below. As stated here before, gold miners can serve as highly effective proxies for the yellow metal itself in trading activities, including shorting. In that vein, Direxion offers two inverse funds that may be of interest: DUST and JDST. The juniors tend to be more sensitive than the majors.

[tracking: GDX, GDXJ, DUST, JDST, GLD, SLV]The SEC released a risk alert regarding digital assets. Far from outlining why such securities are problematic and should be done away with, the notice sought to outline how firms may best be in compliance with the regulatory body’s scrutiny of digital assets trading practices, including applicable rules and regulations.

Initial jobless claims fell to 730k (SA) for the week ending February 20 from a downwardly revised 841k for the week prior. One year ago, we saw 220k.1

To add to this, more than 450k on an unadjusted basis applied for PUA, down from the previous week’s downwardly revised near 513k.

As of February 6, over 19 million people (UA) were still claiming unemployment benefits of some kind, up over 700k from the week prior. In the comparable week one year ago, the US witnessed more than 2.1 million people claiming unemployment insurance from all programs together. The PEUC UI benefits program saw the biggest jump with over 1 million new claims. This is one of the extended benefits programs, meaning more people are remaining unemployed for longer periods of time.2

On the flip side, UI eligibility has just now been expanded under the Biden-Harris administration. This will involve the retroactive payment of benefits to claimants who were faced with a “devil’s bargain” of returning to work in spite of concerns over safety in the midst of a pandemic, or declining some level of employment—and therefore income—with no recourse.

In particular,

The new guidance expands eligibility to three categories of workers:

Workers receiving unemployment benefits who had their continued regular unemployment benefits’ claims denied after they refused to work or accept an offer of work at a worksite not in compliance with coronavirus health and safety standards.

Workers laid off, or who have had their work hours reduced as a direct result of the pandemic.

School employees working without a contract or reasonable assurance of continued employment who face reduced paychecks and no assurance of continued pay when schools are closed due to coronavirus.3

The expansion falls within the PUA UI benefits program structure, and its administration will be handled at the state level. Claims should be filed with a person’s local benefits office.

Mortgage applications decreased again, and at the yet steeper rate of a blended 11.4% (SA) for the week ending February 19, due to a decrease of 11% in refis and 12% in homebuyer applications.

The average loan size across purchase applications was a record $418k. MBA’s choice for a 30Y fixed benchmark came in at 3.08%. The simple national average as reported by Freddie Mac (via FRED) for February 25 was 2.97% on the 30Y fixed.

The expectation here remains that we are due for housing market—and more generally, real estate—weakness. Some 2.6 million households remain in a state of mortgage forbearance, we have worked our way through much of the qualified pools of homebuyers and refi seekers, lending standards are being relaxed, and the labor market is in pain.

That said, January pending new home sales were robust.

Commercial real estate distress is only growing, though demand for the properties at a discount has been relatively healthy thus far. There also seems to be no shortage of investors in associated CMBS, still.

In relation to what the future holds for commercial real estate, here’s the quote of the week; an understatement that has much broader application:

It’s a little presumptuous to assume that when everyone is vaccinated, the green light is immediately switched and we immediately return to 2019 fundamentals.4 ~Will Sledge, senior managing director, JLL’s capital markets group

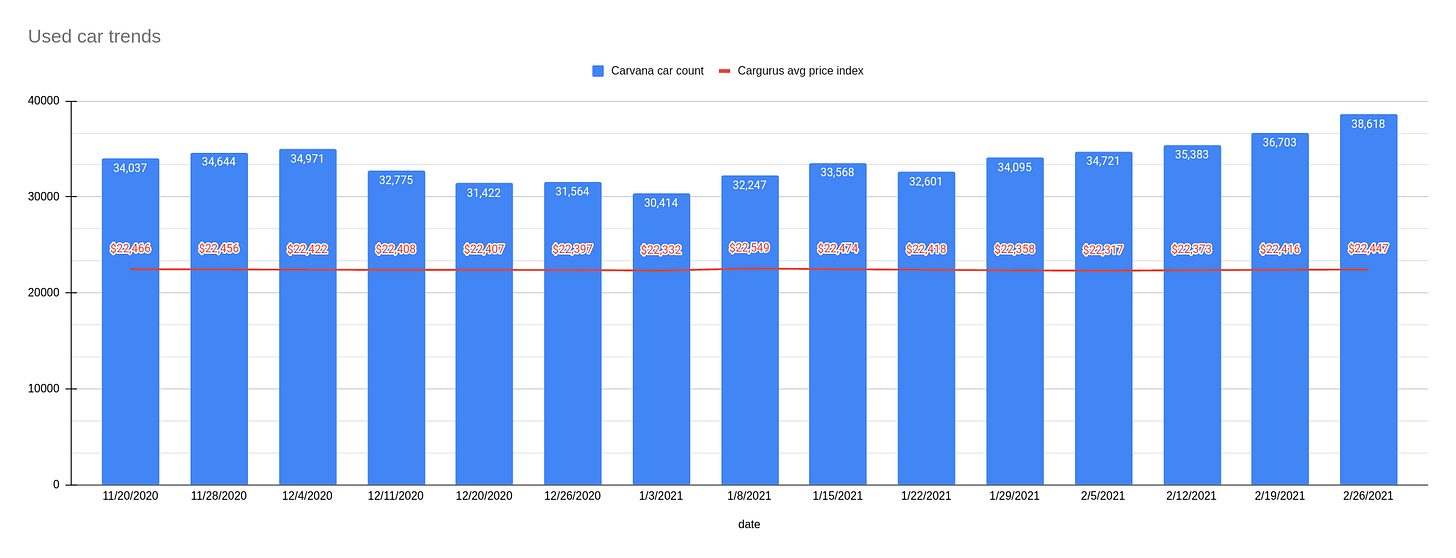

[tracking: NLY, XLRE, DRV, SPG, VNO, WPG]Used car trends: The latest Carvana car count as of February 26 increased 5.22% to 38,618 vehicles from 36,703 the week prior, while the CarGurus average price index rose 0.14% to $22,447 from $22,416. This is the highest car count reported since the start of data gathering for this newsletter in November of last year.

Sovereign matters:

Central European currencies took a hit as the corresponding countries face down what some are terming a third wave of the pandemic. Czechia in particular, followed by Hungary and Poland, are debating further lockdown measures and/or resisting any additional opening at this time as they grapple with rising infection rates. Slovakia and Serbia deserve mention, as well.

Moody’s revised upward Taiwan’s outlook to positive from stable since the nation’s governance appears stronger, and its economy more durable, than the ratings agency previously gave it credit for. Furthermore, it has a track record of solid decision making that supports its fiscal standing, as well as national trends in place that continue to highlight its competitiveness.

Moody’s downgraded Tunisia with a negative outlook given deteriorating governance and a contentious relationship with civil society institutions that will complicate decision making and policy implementation in the service of more adequate debt management, among other objectives.

S&P Global upgraded New Zealand with a stable outlook on account of how well the nation has contained SARS-CoV-2 transmission relative to most. It is believed that even should things worsen again temporarily in the form of another outbreak, or sectors such as real estate take a hit, the country has the capacity to weather the challenges. If there were ever any doubt over whether it made economic sense to contain the virus and financially support the general public as opposed to carrying on as if it didn’t exist and letting it run rampant, the example of New Zealand, and Australia for that matter, should put that to rest.

S&P Global downgraded Cape Verde with a stable outlook as it, along with international tourism, continue to be negatively impacted by the pandemic. The ratings agency does not see an economic recovery to pre-pandemic levels until 2024 here.

Moody’s has revised upward its projections of US and EM growth while cutting that of Europe.

[tracking: EDC/EDZ, VWO, EWU, IEV]The current state of equity: JPM pledges funds to help fuel the businesses of America’s marginalized.

As of the CDC's February 26 update, the US has witnessed 185,880 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per excess deaths data. That’s an average of 439 people per day. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 510,373 puts the probable COVID-19 death figure somewhere north of 610k. Across all causes of death, we suffered 118% of the deaths in 2020 that we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

“Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-365-NAT. US Department of Labor (February 25, 2021).

Employment and Training Administration. “US Department of Labor Guidance to State UI Programs Expands Eligibility for Workers Who Declined Work due to Pandemic Safety Concerns.” US Department of Labor (February 25, 2021).

McNeely, Allison. “‘Purgatory’ Grips $146 Billion of Distressed Commercial Property.” Bloomberg (February 25, 2021).