02052021 :: Friday finance

02052021 :: Friday finance

A partial digest:

Friday was day 17 of the Biden-Harris administration.

Pfizer’s CEO echoed Moderna’s in advancing the possibility that COVID-19 is here to stay and vaccinations will become a routine part of life, as with the flu.

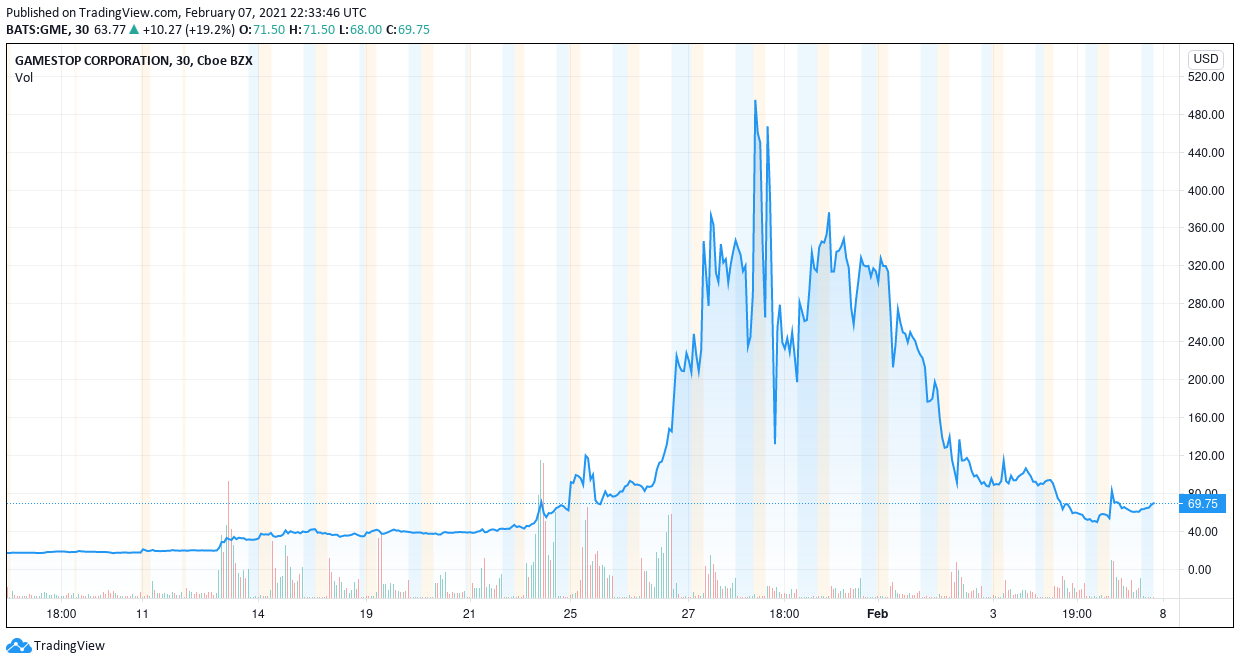

Those interested in how a >100% short interest position was achieved in GameStop [GME] would do well to read up on the SEC’s Regulation SHO.

To be more specific, the following parameters may or may not have been adhered to by the various parties involved:

There is language within the regulation around how broker-dealers mark the securities orders we place when we are trading (long, short, short-exempt) [Rule 200].

There is a “locate” requirement that a broker-dealer have reason to believe that prior to facilitating a short sale, they can actually borrow the security and ensure delivery on the date due [Rule 203(b)(1) and (2)].

Market makers may be exempt from the above “locate” requirement within the course of fulfilling their professional obligations, especially in providing market liquidity, but only to a point. They cannot leverage their exception status in order to engage in speculative selling; nor for their own investment purposes; nor in a manner that is disproportionate to their typical market making activity in that security. What’s more, no arrangement can be entered into with anyone else to leverage their own exemption from the “locate” requirement in order to help the other party deliberately skirt said requirement [footnote 7].

There is a requirement that broker-dealers of a registered securities clearing agency act in a timely manner to close out positions termed “failures to deliver,” which may include permissible naked short sales. For instance, in the process of providing market liquidity and meeting the demands of market participants, market makers may go out on a limb and create a position without having access to the underlying securities. When it comes time (the settlement date) to unwind that position and deliver the actual securities to those with whom they are transacting with, they may experience a temporary failure to do so for a variety of reasons. Upon persistent failures to deliver over so many consecutive days and where a certain amount of the shares outstanding is involved, the securities themselves may end up classified as “threshold securities.” In that case, said broker-dealers must acquire shares and close out their positions immediately [Rules 203(b)(3) and 204].

Really, the entirety of the document referenced here, “Key Points About Regulation SHO,” is worth a read.

Ethereum continues its march upward. Most recent price action is being attributed to the CME’s inclusion of ether futures come Monday, February 8.

Of the cryptos, ethereum seems the most promising: highly utilitarian, one of the greatest adoption rates, and it may avoid the pitfalls of the whimsical asset, unlike the expanding list of meme coins and even bitcoin.

Total crypto market cap is once again above $1 trillion, nearing $1.16 trillion as of publication.

[tracking: BTC, BITW, ETH, ETHE]US consumers acted responsibly with their stimulus payments, it would appear, even paying down credit card debt and saving more. (Gasp!) Indeed, bank issued credit card debt has fallen by 14% since March 2020, while savings has reached record highs. Some say all this is due to the fiscal aid packages passed by Congress, but that narrative neglects the importance of student loan and mortgage forbearance, especially. Given the chance, why wouldn’t people pay off revolving, higher rate debt, or simply save more, while on break from larger, lower rate, longer-term loans?

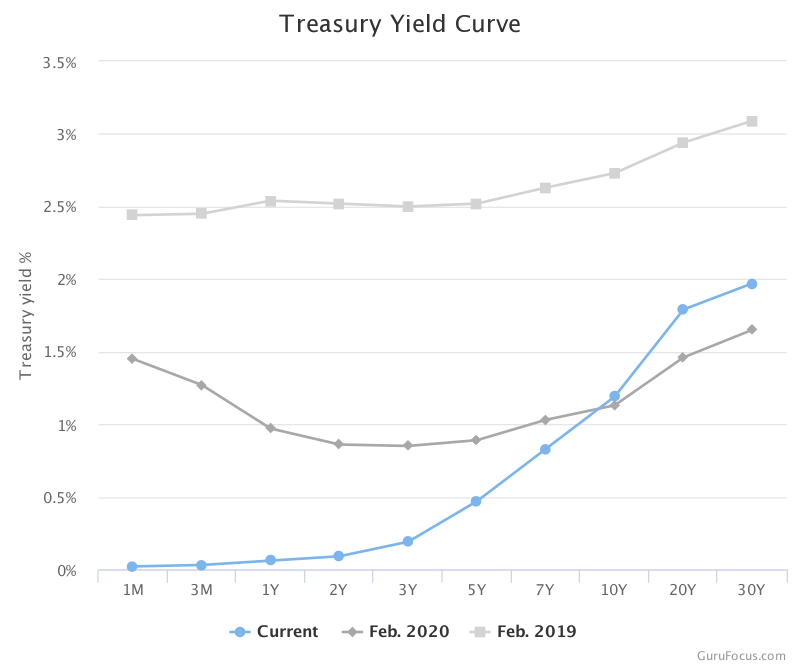

This past week saw a massive jump in yields, all the way up to 1.17% on the 10Y as of Friday. While inflation expectations may or may not project 2%+ inflation rates somewhere off into the future, the Fed is actively seeking 2%+ inflation on average and for a longer period. Even then, we still may not get there anytime soon.

Additionally, inflation expectations or no, we can't view current yields in a vacuum. For example, the dollar index (DXY) gained for the week against a basket of international currencies, meaning Americans have yet to lose any major purchasing power. It’s also still the world’s reserve currency, and it’s still in demand.

What’s more, the December reading of the real personal consumption expenditures index (PCE)—the Fed’s preferred inflation index—actually decreased, due to declines in spending on both goods and services.

Is there genuine cause for concern, then, regarding climbing yields? Perhaps if one is in Treasuries. The value of their bond portfolio is in decline. However, where were they when the Fed announced its inflation policy shift, or when the federal government passed fiscal stimulus?

For the wider populace, the answer is no, or at least not yet. We are seeing only confined cases of inflation in areas like housing prices and stock valuations, and perhaps in some foodstuffs due to supply shocks. The latter in particular is troubling, but none of this equates to systemic inflation that materially devalues our money and our ability to afford things across the board.

In other words, we don’t yet have more money chasing fewer goods, systemically-speaking. And on a related note, no rate hikes are planned, and perhaps for good reason.

So, what’s going on to drive yields up if it’s not fundamentals? Back to those expectations. If dominant market players interpret the tea leaves a certain way, leading themselves to believe that we’re heading towards recovery and price increases soon-ish, they won't buy further into Treasuries at this time, and demand will cool further. Yields will continue to rise, values will fall.

Thus, we enter the self-fulfilling prophecy, the confirmation bias feedback loop between expectations and yields. To them, the future looks rosy, “normalcy” is near at hand. Hence, they refuse to buy Treasuries and become potential bagholders, which fuels further rises in yields as their collective demand wanes.

To others, the future looks difficult at best, with anything akin to “normal” being several years away (say 7.4), and market corrections inbound. In that case, this may be a buying opportunity for them, before another flight to safety compresses yields once again.

[tracking: TYO/TYD, TMV/TMF, DXY]Initial jobless claims dropped to 779k (SA) for the week ending January 30 from a downwardly revised 812k the week prior. One year ago, we saw 201k.1

To add to this, close to 350k on an unadjusted basis applied for PUA, down from the previous week’s downwardly revised 403k+.

As of January 16, over 17.8 million people (UA) were still claiming unemployment benefits of some kind, down close to 500k from the week prior. In the comparable week one year ago, the US witnessed just over 2.1 million people claiming unemployment insurance from all programs together.2 The EB program saw the biggest gain as close to 200k additional individuals neared the end of the UI benefits road from January 9 to January 16.

Compare the above to the mere 49k jobs that were added to the economy in January, and keep in mind millions are not being counted in official unemployment figures.

Mortgage applications increased a blended 8.1% for the week ending January 29, mostly due to a snapback in refis of 11% overshadowing a meager rise of 0.1% in homebuyer applications. The 30Y fixed came in at 2.92%.

The expectation here is still for incoming housing market weakness. Some 2.7 million households remain in a state of forbearance. That number has been steady for a little while, implying that without material improvement in the economy, we could eventually begin to see some foreclosures.

Meanwhile, there’s evidence that some mortgage servicers didn’t hold up their end of the federal forbearance arrangement, to the detriment of consumers in many cases.

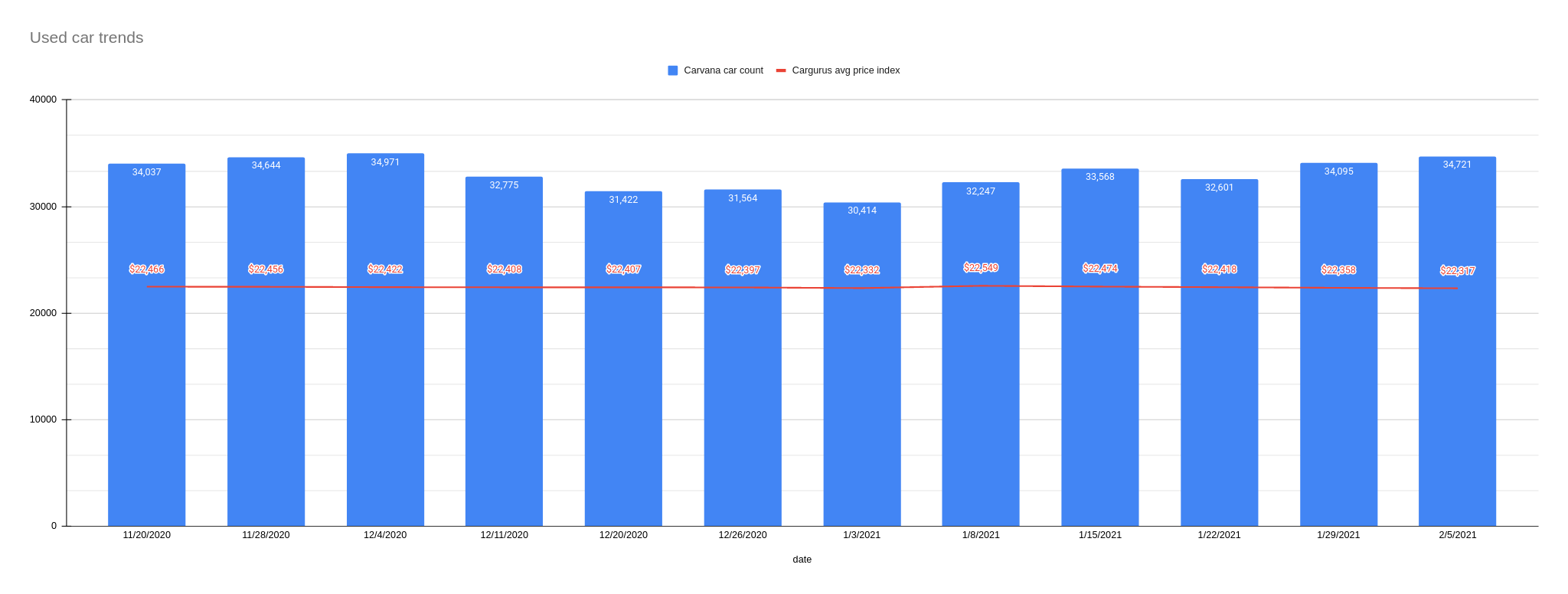

Used car trends: The latest Carvana car count as of February 5 increased 1.84% to 34,721 vehicles from 34,095 the week prior, while the CarGurus average price index fell 0.18% to $22,317 from $22,358.

Sovereign matters:

Burma’s military carried out a coup against democratically-elected leadership, placing Aung San Suu Kyi and others under arrest on various charges that appear fabricated. For instance, the military claims there was election fraud. (Maybe they took their cue from the US.) A one-year state of emergency was ordered and is being imposed by Burma’s military. The international community is condemning the power grab and debating sanctions.

Panama has been downgraded by Fitch with a negative outlook. An ever decreasing fiscal revenue to GDP ratio is one of the primary factors. The country is struggling under mounting public debt, and it’s unclear how the government’s efforts to right the ship will pan out as the pandemic grinds on.

Fitch revised downward Kuwait’s outlook on political and institutional gridlock that threatens the country’s ability to borrow in the near-term, as well as a lack of reforms to address a deteriorating fiscal landscape. However, the nation is still viewed as being in better shape than many.

[tracking: EDC/EDZ, VWO, MCHI]The current state of equity: A battle over racism as a social studies standard in the classrooms of North Carolina.

As of the CDC's February 5 update, the US witnessed 176,482 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per excess deaths data. That’s an average of 437 people per day. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 462,037, puts the probable COVID-19 death figure somewhere north of 560k. Across all causes of death, we’ve suffered 117% of the deaths in 2020 that we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

“Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-192-NAT. US Department of Labor (February 4, 2021).