01222021 :: Friday finance

A partial digest:

It’s day three of the Biden-Harris administration.

We may be approaching a serious inflection point in the markets. In the United States,

Initial jobless claims remain extremely elevated (see more below).

The health crisis marches on. Not all people can work or go about their lives if they’re falling ill. Variants and a sluggish vaccine rollout will make a difficult task of gaining the upper hand.

Chapter 11 company bankruptcies were higher in 2020 than in all previous years since 2012, in spite of record support, according to the American Bankruptcy Institute. Corporations, among them zombies, have only borrowed more over the last year. This increases the likelihood that “restructurings” will continue into 2021, since we will not resume the exact path we were on prior to the pandemic. Even if bankruptcy restructuring is not the outcome for most, corporate revenue streams will be under ever more pressure as companies seek to keep creditors happy and show profits.

Personal bankruptcies are being held in check by forbearance, a relationship which cannot last forever.

Every stimulus attempt is shaping up to be a partisan grind. Other parts of the world, including the eurozone, suffer no such compunction about free flowing aid or delusions about its necessity. It is irresponsible at best, and maliciously self-serving at worst, to prioritize serving the owners of capital with labor instead of checks to households while SARS-CoV-2 continues to run amok.

The forces of job destruction and creation are at work. Not all job seekers have the training or experience at hand to keep up with the changes that are rapidly occurring throughout the entirety of the economy.

Biden revoked a key permit on his first day that would have allowed the Keystone XL pipeline project to continue. The gauntlet is being thrown, and Biden did not mince words:

Biden, in an executive order signed hours after he took office, argued that the pipeline is contrary to U.S. national interests.

“The United States and the world face a climate crisis. That crisis must be met with action on a scale and at a speed commensurate with the need to avoid setting the world on a dangerous, potentially catastrophic, climate trajectory,” Biden said in the order.

“Leaving the Keystone XL pipeline permit in place would not be consistent with my Administration's economic and climate imperatives,” he added.¹

TC Energy, the company responsible for the pipeline, will lay people off and suspend operations effective immediately.

It remains the opinion here that the sun is setting on the oil industry, though further stimulus and supply shocks from reduced production may cause near-term spikes in price.

[tracking: XLE, GGN, TAN]Concern persists over yields, inflation, and how stimulus measures are going to be paid for. Some observers appear convinced that the Federal Reserve is in over its head. As if the Fed isn't monitoring the situation, or engaged in asset purchase programs. These observers would also seem to forget that the Fed has deliberately implemented a policy shift of targeting higher average inflation rates and is preparing for that. As always, there is a group of onlookers who may never be content to let the Fed do its job and see its policies through.

Worldwide, many countries are still pursuing stimulus and seeing little in the way of truly systemic inflation, if not deflation, actually.

The landscape is only becoming more friendly toward crypto, with the caveat of regulation: BlackRock is adding BTC futures to two of its funds to offer its clients exposure, while Yellen is seen embracing regulated crypto and Gensler is now head of the SEC.

[tracking: BTC, ETH, BITW, VYGVF, ETHE]McConnell made no bones about where he falls on the spectrum of Trump’s culpability for the Capitol insurrection. That helps to set the stage for a different kind of impeachment trial than last time. And yes, the Democrats in particular will look to block Trump from ever holding office again.

Initial jobless claims in the US remained at the 900k (SA) level (exactly) for the week ending January 16, following a downwardly revised 962k for the week prior. One year ago, we saw 220k.²

To add to this, almost 424k people on an unadjusted basis applied for PUA, up significantly from the previous week’s near 285k+.

As of January 2, nearly 16 million people were still claiming unemployment benefits of some kind, down over 2.4 million from the week prior as programs expired and before Congress and the White House finally passed the new stimulus package inside of the budgetary spending bill. In the comparable week one year ago, the US witnessed close to 2.3 million people claiming unemployment insurance from all programs together.³

Regular state programs saw the biggest increase of almost 386k people, pointing to a jump in new claimants in the unemployment insurance benefits ecosystem.

These are crap numbers, helping to bring about a decline in the WEI for the week ending January 16. It will be things like the labor and jobs picture—which is intertwined with the ongoing health crisis—as well Corporate America’s debt load and government’s hesitancy to pass stimulus, that will drag the markets lower. The economy is already down, and has been this entire time, whether or not part of the population is doing fine.

Nearly one year into the pandemic, and this is where we’re at, in large part because not everyone will wear a mask. That would have meant fewer people getting sick, which would have supported a healthier and more balanced economy, with more businesses still in business and less work absenteeism. It’s not complicated.

Also, let us not forget that one of the goals is to decrease transmission of the virus, and the prevalence of infections and deaths, in order to create slack in the healthcare system again. (It’s too late to “get rid” of SARS-CoV-2.) Easing the healthcare burden isn’t accomplished by simply getting everyone back to work at all costs and in any way possible, even if/when there are jobs to go back to. Coordination, rules, vaccinations, tiding people and businesses over with aid, and adherence to precautionary living are all required. We still have a bit of road ahead of us.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, HYG, TMV, VXX, XLE, TAN, GLD, JDST, BITW, VYGVF, VB, VTWO, TNA/TZA, XLF, KRE, SOXL]

Mortgage applications fell a blended 1.9% (SA) for the week ending January 15, mostly led by refi activity declining 5%, which overshadowed a rise of 3% in homebuyer applications. The 30Y fixed came in at 2.92%.

In other housing news, the FHFA and the CDC have extended foreclosure and eviction moratoriums to the end of February and March, respectively, to attempt to address housing insecurity. However, in many cases, the damage has already been done.

[tracking: DRV, XLRE, NLY, VNO, SPG, W]All Yellen all the time:

…advising that we go big.

…will work to incorporate crypto into a regulatory structure rather than shun it, and Gensler is to head the SEC. The Biden administration’s posturing is shaping up to be crypto-inclusive.

…will seek to preserve Fed independence.

…won’t commit to reinstating expired Fed lending programs from 2020 (unfortunately).

…wants a functional carbon pricing framework.

…will look to establish automatic stabilizers to kick in upon future recessions so that the economy is not dependent upon partisan politicking to obtain assistance.

and more.

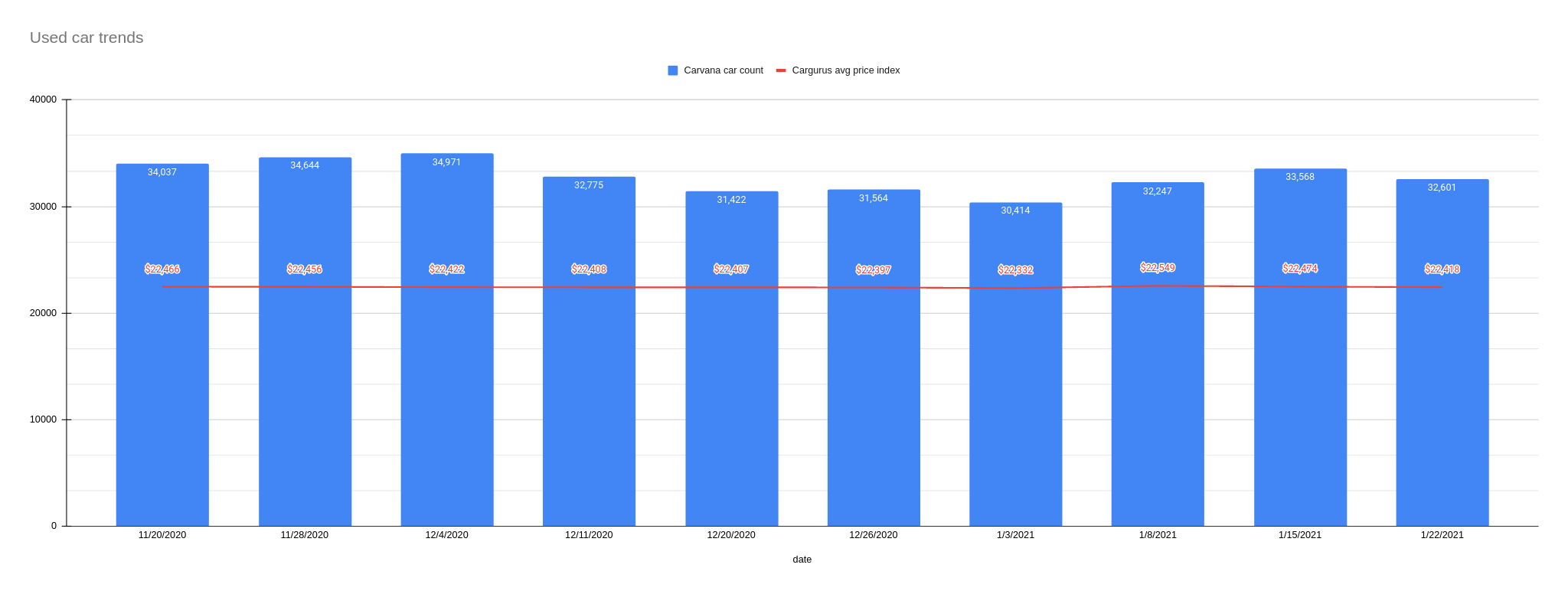

Used car trends: The latest Carvana car count as of January 22 decreased 2.88% to 32,601 vehicles from 33,568 the week prior, while the CarGurus average price index fell 0.25% to $22,418 from $22,474.

Sovereign matters:

As widely reported, Brexit isn’t going so well. Now, the Confederation of British Industry, which doesn’t see a recovery taking shape yet, is seeking an additional $10.3 billion in immediate government aid for the country’s corporations. The month of March, when Finance Minister Sunak’s next budget comes out, is not soon enough, they say.

A recent research report indicates that 10% of companies in the eurozone only have six months of cash on hand.

The Swiss are investigating Lebanon’s central bank governor, Salameh, regarding transfers that purportedly could be related to aggravated money laundering and embezzlement.

FDI into China continued to climb for the month of December, reaching a record amount in 2020 of over $144 billion. The Netherlands and UK, in particular, have upped their investments considerably.

[tracking: MCHI, FXI]Investors continued to pile into Canadian securities for the month of November, though the country suffered a Biden blow over the Keystone XL pipeline on the President’s first day in office.

[tracking: EWC]As discussed before, Zambia is increasing its stake in its own mining industry, this time through a convoluted debt-funded buyout of Glencore’s majority stake in Mopani Copper Mines PLC. While the nation’s leader, President Lungu, argued that it was a necessary move to address economic distress brought about by the pandemic, it seems at least partially politically motivated and self-serving; elections are being held in August, and more than 15k laborers would have lost their jobs were the mine to close, or so the mining minister claims.

The current state of equity long read: “Daughters of the Bomb: A Story of Hiroshima, Racism and Human Rights.”

As of January 22, the US witnessed 170,309 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s an average of 439 people per day. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 410,336, puts the probable COVID-19 death figure somewhere north of 520k. Across all causes of death, we’ve suffered 115% of the deaths we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

¹ Frazin, Rachel. “Canadian Firm Cuts 1,000 Jobs after Biden Revokes Keystone XL Permit.” The Hill (January 21, 2021).

² The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

³ “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-108-NAT. US Department of Labor (January 21, 2021).