12182020 :: Friday finance week in review

A partial digest of what we learned:

Will it be $908 billion, or only $748 billion if aid to states and municipalities gets axed to keep COVID-19 lawsuit protections out? The disputes don’t end there. A stimulus package accord may be derailed by sticklers for an irreversible end to Federal Reserve lending programs, much against Powell’s wishes. Then, there’s a lack of agreement over $1,200 checks to households.

It’s probable that traders have priced in at least $908 billion for the next aid bill, whenever it arrives. A smaller bill would mean that equity valuations have overshot the mark, on this front.

The bigger question is whether equities and other assets are overpriced, more generally, or if developments have indeed been accurately priced in and there are yet more positives coming down the pike. That would leave markets with room to run and traders to jockey further for position.

With this in mind, here’s an inexhaustive list of considerations:

Biden’s presidency seems fairly priced in, by now.

We have two vaccines that have received emergency authorization in the United States and likely will elsewhere, with a third on the way. Inoculations have begun. The vaccine miracle has likely been mostly priced in. In fact, this may be an area where we have put the cart before the horse and the reality may disappoint to the downside.

So many questions remain about how the vaccination process will play out. For example, if children can’t get vaccinated because they are too young, they can still carry and transmit the virus, and get sick. If inoculated adults around them are still at risk of also transmitting SARS-CoV-2 and/or getting infected/reinfected, or immunity simply doesn’t last that long, then the virus can linger. To compound this, some people are already letting their guard down (some always had it down) due to wide publicity of the vaccines. And let’s not forget the potential for viral mutations. No end to the pandemic is just around the corner in our collective future, yet.

A recovery, whatever that means, has been getting priced in before we even have it; the whole preconceived notions over fundamentals thing. This is another area where the reality may disappoint, i.e. we don't get the requisite resumption of economic activity and growth.

Stimulus has been getting priced in, but as noted above, may disappoint to the downside.

Improvement in the labor market was getting priced in, but the weekly numbers have been anything but an improvement (see below). Furthermore, thousands of employers have gone under. They aren’t open anymore for some segments of the workforce to return to, signifying permanent job losses and unemployment.

In the absence of additional fiscal stimulus, some households have just been burning through their cash. Many companies—among them zombies and those on the edge—have, too. Are loan delinquencies, bankruptcies, and failed businesses getting adequately priced in?

There’s a childcare crisis in the US, helping to preclude a true recovery in the dismal labor picture. Priced in?

The coronavirus health crisis is still in effect and won’t end soon, vaccine rollout or no. Priced in?

Household wealth is increasingly tied to asset valuations, such as homes and stocks, not incomes or real savings (especially when savings are tied to loan holidays). Priced in?

Waves of non-performing loans (NPLs) are heading to shore. Priced in?

What positives/negatives remain to be priced in at this time, and will they cumulatively propel markets further or drag them down? Optimism and realism don’t equate.

On Monday, December 14, the electoral college voted the popular vote, as well as the will of their people, and affirmed a Biden-Harris victory. The votes will be sent to Senate President Pence by December 23. Congress will tally those votes on January 6 and Pence will make the formal announcement, at which point the results can be challenged one last time should a member of each chamber sign on to an objection over the votes. Such a challenge is to be evaluated separately by each chamber of Congress to determine how, indeed, the votes should be counted, if not the way they arrived to Pence. If they revise the count and no candidate receives the 270 majority, the House calls the election. This is done on a one vote per state basis, however, not one vote per House member. With more Republican than Democrat states represented in Congress, Trump could be chosen. The likelihood of all this seems terribly slim, though.¹

Meanwhile, the original Pennsylvania case exploring the question over whether the state’s supreme court had authority to extend the ballot receipt deadline (as opposed to the state legislature) is still pending with SCOTUS and may be heard early next year. Importantly, the Republican party of PA has replied in support of the petition for a writ of certiorari, but apparently with full understanding that this case will not have a bearing on the current election.

From the brief:

…this case is an ideal vehicle, in part precisely because it will not affect the outcome of this election.

Indeed, this Court has repeatedly emphasized the imperative of settling the governing rules in advance of the next election, in order to promote the public “[c]onfidence in the integrity of our electoral processes [that] is essential to the functioning of our participatory democracy.” Purcell v. Gonzalez, 549 U.S. 1, 4 (2006). This case presents a vital and unique opportunity to do precisely that. By resolving the important and recurring questions now, the Court can provide desperately needed guidance to state legislatures and courts across the country outside the context of a hotly disputed election and before the next election. The alternative is for the Court to leave legislatures and courts with a lack of advance guidance and clarity regarding the controlling law—only to be drawn into answering these questions in future after-the-fact litigation over a contested election, with the accompanying time pressures and perceptions of partisan interest.²

What’s more, SCOTUS might agree that the case is not to influence election 2020. The high court has decided to “distribute [it] for conference” on January 8, two days after the January 6 electoral deadline of announcing the election’s victor in Congress. Additionally, distributing for conference doesn’t imply that they will actually discuss the case at all, never mind choose to hear the case at a later date.

Therefore, it would seem that whatever recourse Trump and his legal team explored across the entirety of the country’s court system really is, finally, coming to an end. The above case, should it be heard, could no doubt impact future elections, and perhaps even in a significant manner. However, this year, the ship looks to have left the harbor.

Separately, Trump may refuse to leave the White House. As stated here before, this may open him up to removal by Secret Service, perpetuating his self-portrayal as the victim of considerable [unsubstantiated] fraud and now a [fabricated] coup. The move could help foment violence perpetrated by Trumpists in response to what they see as their commander in chief being forcibly removed from legitimate office. Up to now, he has done and said plenty to lay the groundwork for such a thing.

Come what may, markets and the nation need him gone, though, and may rally in relief the very first day where he just doesn’t hold office anymore.

The first Pfizer-BioNTech vaccine doses have been administered in the US and Canada as of Monday, December 14. Upon being jabbed live on camera, NY ICU nurse Sandra Lindsay declared, "I feel like healing is coming."

Over one million people worldwide have already received their first dose. It hasn’t all been smooth. Allergic reactions, deaths, and vial delivery issues have been reported. Even some healthcare workers—the prioritized frontliners themselves—are balking at getting jabbed.

And, apparently not everyone should. There are parameters to consider, straight from the vaccine makers as well as VRBPAC and the FDA, the CDC, and others. STAT has published a guide on the Pfizer-BioNTech vaccine.

Meanwhile, the Moderna vaccine (mRNA-1273) VRBPAC briefing document is freely available online. Emergency authorization of mRNA-1273 was recommended by VRBPAC, and the FDA has authorized it for emergency use to close out the week.

The AstraZeneca vaccine (AZD1222) is still working its way through the paces, though its path to approval has been the most questionable.

Gold jumped this past week before settling north of $1,880/oz. Numerous China tensions, an ongoing health crisis, and US domestic political turbulence, among other things, keep the dream alive for some traders eager to see the yellow metal soar.

While prices could be driven up some in the interim, especially by issues related to the South China Sea, the call here for ultimately lower gold prices is not changing. It would be one thing if we were back at $2,069/oz and climbing. Instead, it’s more akin to the waves of a receding tide.

The DXY slipped for another week. We’re sub 90. This makes sense taking into account Bitcoin buying and the appetite for foreign securities like local currency sovereign debt, especially that of emerging markets. Traders seem perfectly content at the moment to give up dollars to chase returns.

To add to this, and linked with Treasury yields having risen again: Japan and China, the two largest out-of-country holders of US Treasuries, continued to cut their purchases in the month of October. That spells less foreign demand for the greenback, putting further downward pressure on the currency.

However, if yields on the long end become more attractive, and/or Bitcoin and EMs see a correction, and/or there’s a flight to safety for whatever reason, the dollar would benefit.

The US government averted a shutdown on Friday night with another stopgap funding bill, extending debates over the budget and a coronavirus relief package for a grand total of two days. And then? We’re waiting…

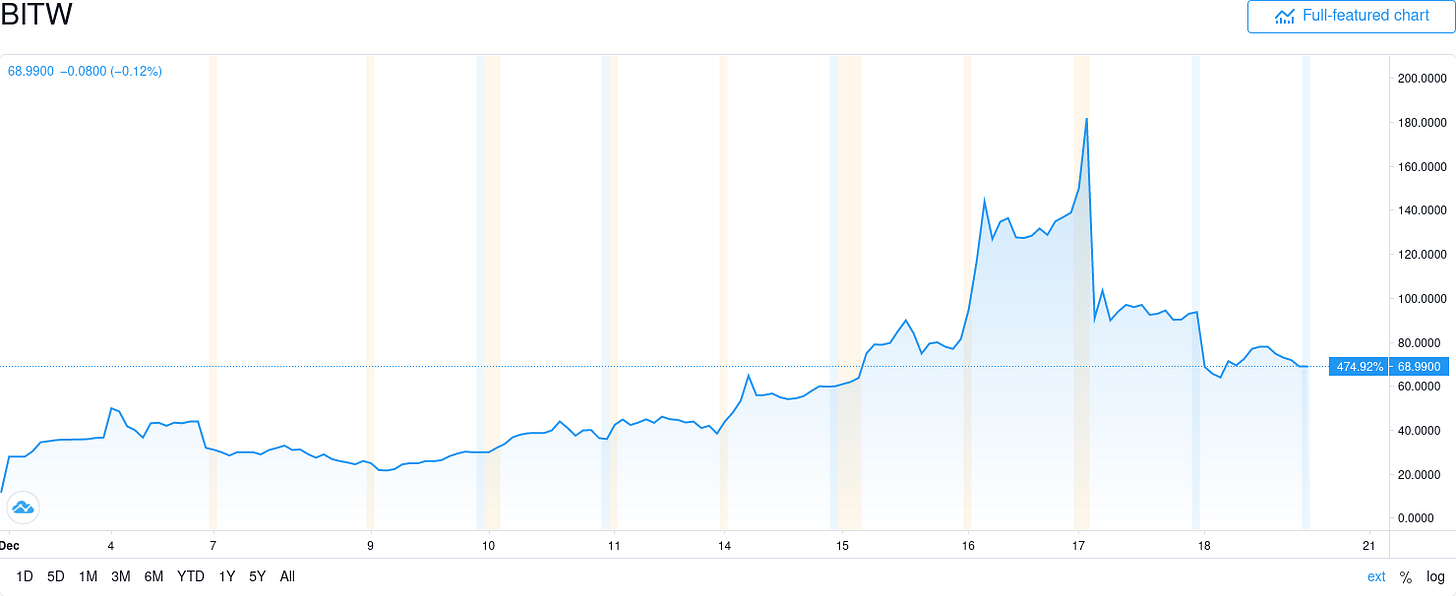

Mass Mutual’s $100 million purchase is a drop in the bucket compared to the $1 billion position being taken by One River Digital. There’s also the new Bitwise fund (BITW), and people were piling in. That is, until the fund deflated the last two days of the week.

As mentioned previously, to invest in crypto, one need not chase crypto. Traditional equities including PayPal and Visa provide some semblance of exposure.

[tracking: PYPL, V, BITW]Accounting relief for US banks to work with their customers on relaxing debt repayment behavior is set to expire without a Congressional extension, as are other coronavirus relief measures.

Initial jobless claims once again jumped, this time to 885k (SA) for the week ending December 12 from an upwardly revised 862k for the week prior. One year ago, we saw 229k.³

An ugly labor situation is worsening, and Congress still hasn’t cobbled a package together. Several relief measures are set to expire at the end of 2020 or January 2021, including UI benefits programs.

To add to this, 455k+ people on an unadjusted basis applied for PUA, up from a downwardly revised 415k the previous week.

As of November 28, over 20.6 million people were still claiming unemployment benefits of some kind, sharply up over 1.6 million from the week prior. Each individual program gained claimants. In the comparable week one year ago, the US witnessed slightly over 1.7 million people claiming unemployment insurance from all programs together.⁴

For many unemployed, there are no jobs to go back to (yet). Some of those employers don’t exist anymore.

Small businesses remain desperate, tapping the Fed Main Street Lending program in these final days at a much higher rate than originally. The program, like others managed by the Fed this year in response to the pandemic, will not be receiving Treasury reauthorization.

Mortgage applications in the US rose a blended 1.1 % for the week ending December 11. Both homebuyer applications and refis saw advances of 1.8% and 1.4%, respectively. The going 30Y fixed dropped further to 2.85%, a new record low.

Housing starts and permits rose further in the month of November, but completions fell, perhaps indicating that construction workers are falling ill.

Otherwise, companies the world over keep downsizing their occupancy needs, ensuring that the downturn in commercial real estate persists.

[tracking: XLRE, NLY, VNO, SPG]As tech giants Facebook and Alphabet are hit with antitrust lawsuits, the opinion here is that taking on big tech is good for tech, and for tech investors, as it may better serve the interests of innovation and a diversity of ideas.

[tracking: QQQ, XLK]FTSE Russell and MSCI are the latest indexers to pursue compliance with respect to Chinese firms blacklisted by the US.

Treasury and other US government agencies rank among the Russian hacking targets via the SolarWinds exploit. It is believed that, at the very least, department communications have been compromised.

Bank payouts are coming back in the US and the eurozone. Thus far, financial sector equities have not seen the same degree of appreciation this year as those of other industries.

[tracking: XLF, KRE, SPY]Tesla is joining the S&P 500. Of more interest is that new additions to the index tend to underperform in the year following, while former index constituents are likely to outperform the entire index after their removal by up to 20% over the same period. That said, Tesla is replacing AIMCO, a commercial and residential REIT. They’ll have no easy job of it in 2021.

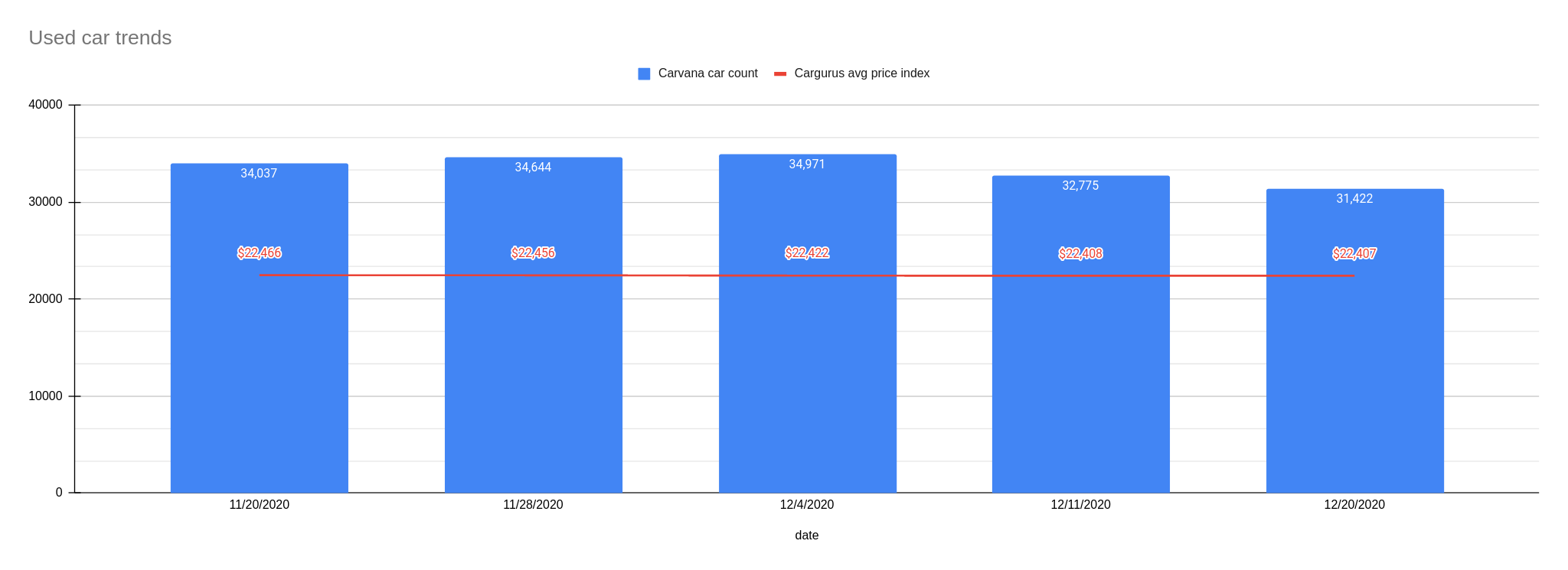

[tracking: TSLA, AIRC, SPY]Used car trends: The latest Carvana car count as of December 20 dropped to 31,422 vehicles from 32,775 the week prior (-4.13%), while the CarGurus price index flattened at $22,407 from $22,408 (0.00%). Falling inventories and rising prices beyond the holiday shopping season into next year could be an indicator of economic recovery setting in.

Sovereign matters:

China and the EU are working quickly in their own spheres to establish bad banks to deal with NPLs. The souring loans are coming, is the message, and it should be no different in the US.

The US Treasury has declared Switzerland and Vietnam currency manipulators. The Swiss don't feel like they have a choice, and Vietnam denies the implications.

Fitch downgraded Seychelles again, due to issues such as the coronavirus blow to tourism (25% of GDP), weakening domestic currency, stagnating forex reserves, and growth in the country’s external debt/GDP.

Fitch revised downward Peru’s outlook to negative, on account of the potential for policy volatility and political upheaval, destabilizing deficits, and difficulty implementing reforms.

In the wake of a sovereign default, Zambia is seeking to insert itself in the mining revenue stream to help bring about an economic recovery. It will take majority stakes in “strategic mines” active within its borders. Companies with operations in country include Barrick, Eurasian Resources Group, First Quantum Minerals, and Glencore. Stock prices of mining companies can be adversely impacted by such news. Zambia may not be the only country to pursue such a course of action, as sovereign finances are strained everywhere. Just don't call it nationalization, says President Lungu.

[tracking: GOLD, FM:TSE, GLEN:LON]

Real incomes are projected to fall in Russia, as is to be expected elsewhere. The US saw personal income fall for the month of October. Another reading for the month of November is due next week.

Nations are in different places in their willingness to maintain supportive monetary and fiscal stances. Germany, Japan, and Switzerland pledge expansion; Saudi Arabia, the UK, Russia, and Norway are telegraphing tightening.

In spite of their own troubles, certain countries are attempting to prop up others, for strategic reasons or not. Led by MUFG, Japan is lending $500+ million to Afreximbank to boost the bank’s capacity to ease the strain of the pandemic on African nations; China is helping Pakistan to extricate itself from indebtedness to Saudi Arabia; and Canada is offering hundreds of millions in aid to address COVID-19 in other nations through organizations such as UNICEF.

Greece has sold nearly half a billion dollars in spectrum in a bid to reduce government debt and prepare itself for future growth. Startups engaged in 5G products and services will be recipients of a portion of the funds.

[tracking: EDC, VXUS, VWO]The current state of equity: Childcare in the United States.

SARS-CoV-2 continues to wreak havoc on business operations and consumer goods and services, most recently paying a return visit to meat packing plants. Simultaneously, OSHA has assessed over $3.6 million in coronavurus violations committed by businesses in the US since the pandemic befell the country.

As of December 18, the US witnessed 142,289 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s 401 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 315,057, puts the likely COVID-19 death figure somewhere north of 405k. Across all causes of death, we’ve suffered 113% of the deaths we would have expected in a non-pandemic year given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a pre-existing one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably considerably higher.

Footnotes

¹ CNN, Zachary B. Wolf and Will Mullery. “Congress Has the next -- and Final -- Vote in the 2020 Election. Here’s How It Works.” CNN (December 7, 2020).

² Gallagher, Kathleen, Russell Giancola, John Gore, Michael Carvin, Noel Francisco, and Alex Potapov. “REPLY BRIEF IN SUPPORT OF PETITION FOR A WRIT OF CERTIORARI” (December 15, 2020).

³ The data quality of these numbers is still compromised, per a GAO report.

⁴ “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 20-2292-NAT. US Department of Labor (December 17, 2020).

Correction: The current issue originally stated, "As of November 21, over 20.6 million people were still claiming unemployment benefits of some kind, sharply up over 1.6 million from the week prior." This has been edited to properly reflect the actual date for this metric, November 28, from the DOL's report.