12252020 :: Friday finance week in review

A partial digest of what we learned:

Lame what? Trump sends the $892 billion in coronavirus stimulus packing back to Congress for amendments including $2k payouts to households, the likelihood of which isn’t great. Never mind that the package is not as large as hoped, and is disappointing in its breadth, as well, leaving out elements such as much needed help for states and municipalities.

Pelosi will reportedly call a full floor vote regarding the checks on Monday. All along, the Democrats themselves wanted bigger checks for households. However, if they think Trump’s involvement on this front gives them leverage over the GOP to get it done, they can forget about it. For McConnell, Toomey, and others, the notion is probably DOA. Indeed, the House GOP has already blocked a move by Democrats to advance a measure to approve such payments.

Trump is doubling down. Note that the budgetary spending bill and coronavirus relief are a one-package deal. Hence, a government shutdown now seemingly hinges on what (if anything) the White House, Democrats, and Republicans hash out over stimulus checks in the 11th hour.

The rundown of what expires or is forgone without a spending bill in place and no coronavirus aid includes:

UI benefits for millions of people via such programs as PUA, PEUC, and EB.

Key bank workings and allowances for lenders, which up to now greased the wheels for financial institutions to accommodate struggling customers by modifying various loans. Dealing with PPP loans, both written and newly provided, would have become easier, as well.

Childcare, rent/eviction, and food assistance.

Tent cities may only be the beginning of this country’s troubles should no more government aid be immediately forthcoming.

Additionally, Trump vetoed the defense spending bill (NDAA) that made its way to his desk, on account of social media protections and military base name changes he didn’t fancy. (Or, was it because the Corporate Transparency Act, a serious anti-corruption measure aimed at confronting criminal use of anonymous shell companies, was rolled up into it?) The NDAA was first passed in 1961 and has been reauthorized every year since. Congress is preparing to vote on Monday to override the veto.

Watch for market volatility and declines in the most sensitive corners, including small caps and oil. Broadly speaking, reasons are piling up for a correction in equities.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, HYG, TMV, VXX, XLE, TAN, GLD, BITW, VB, VTWO, TNA/TZA, XLF, KRE]The UK has raised the alarm over another mutant strain of SARS-CoV-2. Accordingly, restrictions on UK travelers have swiftly been imposed by multiple nations. That said, many countries have already documented COVID-19 cases caused by this very strain within their borders.

The new strain is apparently more infectious. Nobody is yet saying it would render existing vaccines useless, or that it’s more dangerous. Time will tell how mutations play out. Which brings us back to the mink.

Switzerland and Germany are to begin vaccinating their populations with the Pfizer-BioNTech inoculation shortly, expanding the international rollout (though all this vaccine nationalism may hurt global progress against the pandemic overall).

A trade deal has been reached between the UK and EU. Should the British Parliament approve of it when they meet to debate it on December 30, one day before the Brexit transition period ends, Brexit will have occurred with a deal in place. After 4.5 years, may the term “no-deal Brexit” finally be retired.

Not everything has been resolved. Questions remain about fishing rights and financial services, among other areas.

[tracking: GBP, EWU]

Initial jobless claims fell to 803k (SA) for the week ending December 19 from an upwardly revised 892k for the week prior. One year ago, we saw 218k.¹ The labor situation is ugly and there is still no fiscal stimulus package. Several relief measures are set to expire now, including UI benefits programs, and others at the end of January 2021, including the student loan and mortgage forbearance window.

To add to this, 397.5k+ people on an unadjusted basis applied for PUA, down from a downwardly revised 454k+ the previous week.

As of December 5, over 20.3 million people were still claiming unemployment benefits of some kind, just slightly down from the week prior. In the comparable week one year ago, the US witnessed a little over 1.75 million people claiming unemployment insurance from all programs together.²

For many unemployed, there are currently no jobs to go back to. Some of those employers don’t exist anymore, and more are on their way out.

Mortgage applications in the US increased a blended 0.8% for the week ending December 18. A fall in homebuyer applications (-4.6%) was made up for by a gain in refis (3.8%). The 30Y fixed came in at 2.86%.

MBA’s mortgage forbearance figures increased ever so slightly to 5.49% as of December 13, describing the situation for an estimated 2.7 million homeowners. Of the loans in forbearance, 78.54% are already in a forbearance extension.

New home sales dropped a considerable 11% (SA) for the month of November. Existing home sales also fell by a relatively moderate 2.5%.

In short, the thesis here still is that the housing market will take a hit eventually, especially given the poor labor picture/sputtering job market, and expiring coronavirus relief measures.

Adding to other commercial front headwinds mentioned in prior issues, many white collar workers do not ever want to return to the office. Perhaps commercial real estate should be repurposed somehow. At any rate, things will get worse before they get better. Shoppers of distressed real estate are already beginning to gather.

Republican attempts to corral Federal Reserve emergency lending powers will persist, even if the confrontation doesn’t prevent the next stimulus package from getting passed, whenever (if ever) that is. We only know what members of the party argue, which is that the Fed’s action this year was outside of its traditional role, and that at least some of the entities shouldn’t be bailed out.

However, what is most likely underpinning the GOP’s behavior is the age-old desire for control, especially over who benefits. That’s simply more difficult to maintain when the Fed is an independent actor and the incoming Treasury secretary is a Democrat. A more benign take would be that the likes of Toomey are disconnected from what’s happening on the ground.

Trump has signed S. 945: Holding Foreign Companies Accountable Act, which governs how and when Chinese companies would be delisted from US exchanges should they not comply with American oversight requirements. Again, a company would have to refuse PCAOB audit inspections for three years straight before the SEC moves to delist. That includes EV high flyers like NIO and XPEV.

As mentioned here previously, some Chinese companies that are considered part of their country’s military industrial complex are already being removed from securities indices and trading in them will soon (January 11) be prohibited per executive order. One can’t help but wonder how loosely the military designation could be applied.

Reuters ran an interesting review of market valuations from what is being termed the “plague year.” Some highlights:

Globally, Denmark’s stock market outperformed YTD. Greece came in at the bottom of the stack.

Against the $USD, the Swedish krona was the best performing currency YTD, the Argentinian peso the worst.

Copper beat gold on a YTD and QTD basis.

The S&P 500 had a better YTD return than the MSCI EM index.

Italy’s 10Y put in one of the world’s best YTD performances for sovereign bonds.

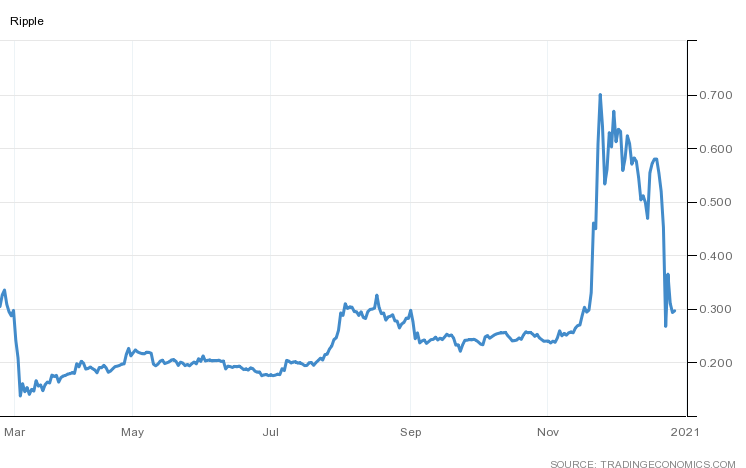

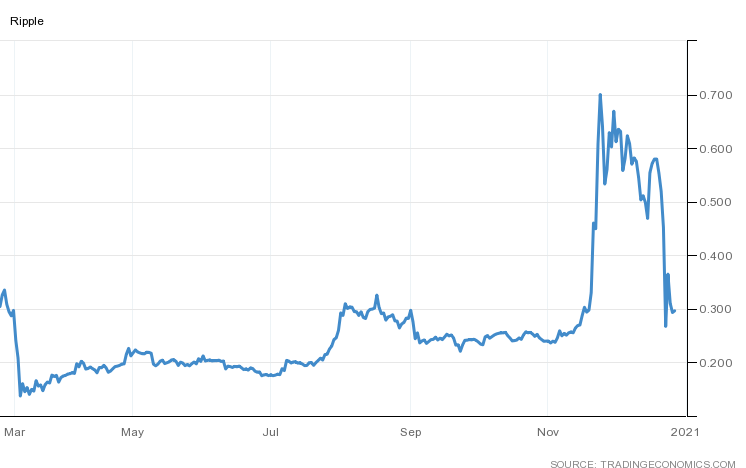

Not all crypto is the same, says the SEC in so many words as it sends XRP scurrying with legal action against its creator, Ripple. The agency charges that Ripple misled investors and should have registered XRP as a security before making money off it. BITW and some exchanges have already dropped what was the third most popular cryptoasset after Bitcoin and Ethereum. Its valuation has effectively imploded.

BTC, on the other hand, continues its march upward.

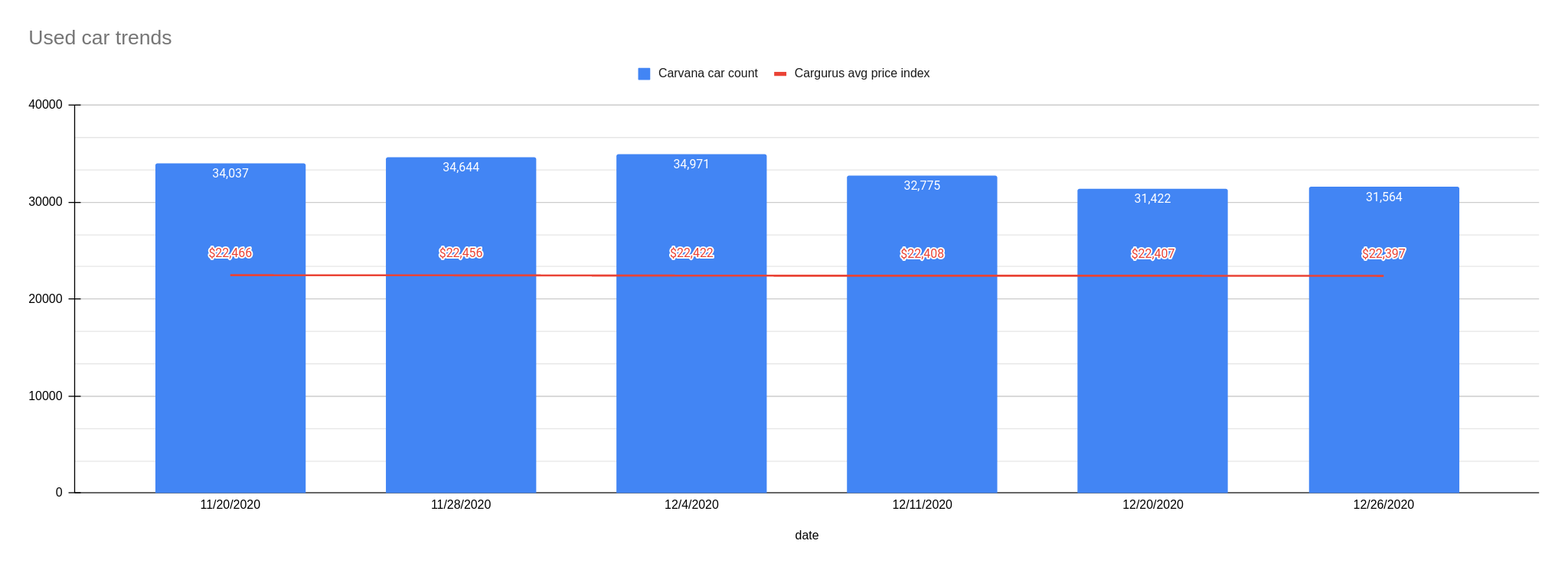

[tracking: XRP, BTC, ETH, BITW]Used car trends: The latest Carvana car count as of December 26 rose to 31,564 vehicles from 31,422 the week prior (0.45%), while the CarGurus price index continued its decline to $22,397 from $22,407 (-0.04%).

Sovereign matters:

Ethiopia is getting a debt lifeline from the Paris Club via a payment extension to the end of June 2021. In general, there continue to be calls to consider debt forgiveness and restructuring when dealing with emerging and frontier debtor nations.

Frontier market debt issuance is set to keep rolling right along next year. Any flight to safety could counteract this.

East Africa is trying to get ahead of the carbon free curve as nations such as Rwanda, Uganda, and Kenya set out to reach renewable energy and electric vehicle targets, helping fuel exploding demand for electric motorbike taxis, for instance.

[tracking: EDC, VXUS, VWO]The state of equity: Mutual aid throughout history.

As of December 23, the US witnessed 144,343 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s approximately 400 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 332,011, puts the likely COVID-19 death figure somewhere north of 420k. Across all causes of death, we’ve suffered 113% of the deaths we would have expected in a non-pandemic year given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a pre-existing one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably considerably higher.

Footnotes

¹ The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

² “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 20-2328-NAT. US Department of Labor (December 23, 2020).

Correction: The current issue originally stated, "As of November 21, over 20.3 million people were still claiming unemployment benefits of some kind, just slightly down from the week prior." This has been edited to properly reflect the actual date for this metric, December 5, from the DOL's report.