01292021 :: Friday finance

A partial digest:

It’s day ten of the Biden-Harris administration.

Volatility was the name of the game this past week, with the VIX on the CBOE gaining over 50% by EOD Friday.

Hedge funds have long had the potential to pose systemic risk to the financial system in the United States. Most, if not all, graduate-level students of finance would have come across the LTCM case study at some point during their programs.

Yes, hedge funds, brokerages, GameStop (GME), and r/WallStreetBets were a thing, but so was GDP growth that was low enough that the United States capped off 2020 in the hole. For the final quarter of 2020, GDP grew by an annualized 4% only, leaving the nation with a YoY contraction of 3.5%. In addition, personal saving and income both declined.¹

Yields fell in response to the volatility, and the DXY gained. It remains above 90, while the 10Y finished at 1.07%.

The pandemic continues to be a slog, with tight vaccine supplies, vaccine nationalism an ongoing issue, SARS-CoV-2 variants wreaking havoc, and even greater fatality risk presenting itself.

Stimulus resistance in the US persists.

Calls continue for a downturn in the markets.

[tracking: UVXY, VTI]Beware the misleading and misinformed broadcasts around GME, the WSB subreddit, brokerages, hedge funds, and the government. Additionally, while more and more details are being exposed, such as Robinhood’s relationship with Citadel and political power brokers, note that what’s being somewhat lost in the mainstream is the 140% short interest of float in GameStop stock that was allowed to accumulate.

There are different means of getting to that 140% value, so how exactly was such a collective bearish position achieved in GME? Was there collusion between brokerage and hedge fund, and to what degree? This all implicates not only hedge funds and larger privileged players, but multiple brokerages and their regulatory body FINRA, among others.

Currently, GME short interest is still above 113% of float as of January 28, according to one analyst. AMC and Virgin Galactic Holdings [SPCE] are likely still the next most heavily shorted stocks in US markets thereafter.

Has BlackRock been raking it in as GME moons?

The full on Biden assault on the oil and gas industry has it on the defensive. It remains the opinion here that the sun is setting on the oil industry, though further stimulus and supply shocks from reduced production may cause near-term spikes in price.

[tracking: XLE, GGN, TAN]

Crypto hasn’t received much love from central bankers of late. From the BoE to the ECB, its lack of state backing and perceived speculative nature are encouraging calls that it won’t last; investors should be prepared to lose everything.

As stated here before, user adoption will help dictate its fate.

[tracking: BTC, ETH, BITW, VYGVF, ETHE]Initial jobless claims in the US remained at the 847k (SA) level (exactly) for the week ending January 23, following an upwardly revised 914k for the week prior. One year ago, we saw 212k.²

To add to this, almost 427k people on an unadjusted basis applied for PUA, down some from the previous week’s upwardly revised 447k+.

As of January 9, almost 18.3 million people were still claiming unemployment benefits of some kind, up nearly 2.3 million from the week prior as programs expired and before Congress and the White House finally passed the new stimulus package inside of the budgetary spending bill. In the comparable week one year ago, the US witnessed close to 2.2 million people claiming unemployment insurance from all programs together.³

The PUA program saw the biggest increase of over 1.6 million people, pointing to a jump in non-traditional applicants.

These numbers remain abysmal, helping to further an even deeper decline (-2.28) in the WEI for the week ending January 23.

Mortgage applications fell a blended 4.1% (SA) for the week ending January 22, mostly led by refi activity declining 5%, which went along with a drop of 4% in homebuyer applications. The 30Y fixed came in at 2.95%.

Existing home sales for the month of December increased 0.7% from the previous month. The price range that saw the greatest YoY jump in sales was the $1m+ category (93.6%).

Inventory is at record lows with a mere 1.9 month supply on hand, and housing prices increased across the country yet again. Hence, not only are we working our way through all qualified buyer pools, but we are continuing to price out some buyers completely.

A reminder also that the forbearance clock is ticking. Builders will continue to build, but at what point will supply actually overshoot the mark because some households will be foreclosed upon and others still won’t have employment to support home purchases? Indeed, new home sales slowed slightly in December.

What’s more, annual sales for 2020 hit a level not seen since 2006, as the country was on its way into the 2008 financial crisis. That’s not comforting.

In the commercial real estate sector, execs are looking to data centers, single-family rentals, and industrial spaces like warehouses to keep the market afloat.

[tracking: DRV, XLRE, NLY, VNO, SPG, W]Yellen was confirmed. She is the first female treasury secretary in the history of the office. One of her many objectives is to re-engage with the OECD on international taxation.

The GME spectacle shined light on the fact that she’s taken money from Citadel, which oversees Melvin Capital, one of the primary shorters of GameStop. She is not alone. There is a revolving door in effect. For example, Bernanke is now a senior advisor to the firm.

The Comptroller of the Currency won’t publish the contentious “fair access” rule that was implemented by an outgoing Trump official and would have forced banks to lend to businesses in sectors that they would have otherwise organically pulled away from, such as the oil and gun industries.

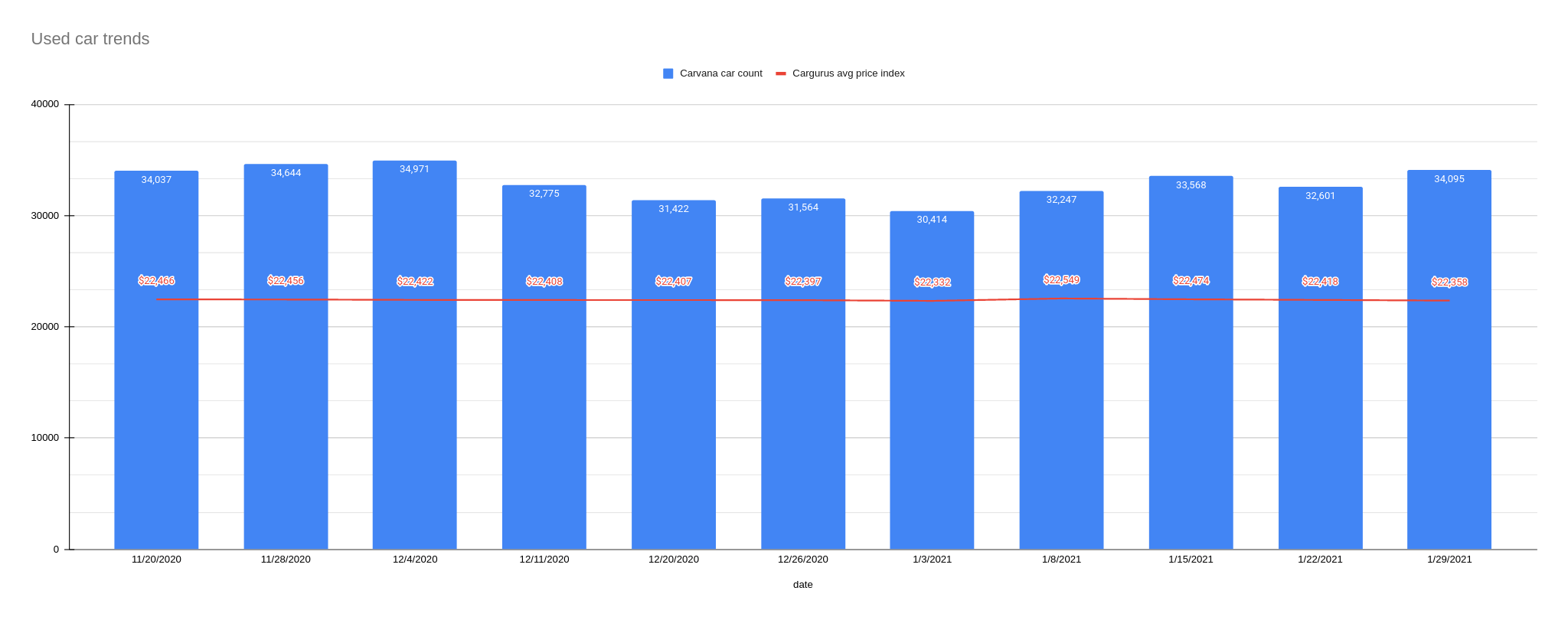

Used car trends: The latest Carvana car count as of January 29 increased 4.58% to 34,095 vehicles from 32,601 the week prior, while the CarGurus average price index fell 0.27% to $22,358 from $22,418.

Sovereign matters:

S&P Global revised the credit ratings outlooks of Azerbaijan and Slovakia to stable from negative. In Azerbaijan’s case, the ratings agency cited the benefits of a ceasefire arrangement between the country, Armenia, and Russia. As to Slovakia, the expectation is that eurozone funds and private investment in the country’s auto industry will boost prospects for solid GDP growth this year and into the next few, at least.

The above revised outlooks notwithstanding, EMs are set to see the bulk of negative ratings action moving forward, says S&P Global. That will make international debt assistance and forgiveness programs all the more crucial for poorer nations.

GDP growth in the eurozone at the end of 2020 surprised to the upside, though nobody is breathing a sigh of relief yet.

The Phillipines is racing to the head of the recovery pack with two straight quarters of GDP rebound. There were gains in manufacturing, trade, and household consumption, among other areas. YoY, the nation still saw an economic contraction of 8.3%.

Reeling from the state of the oil market, Iraq is seeking a credit lifeline from the IMF.

China is the world’s leading recipient of FDI, eclipsing the US for the first time.

[tracking: EDC/EDZ, VWO, MCHI]

The current state of equity: “Low U.S. Rates Exacerbate Racial Wealth Gap, Paper Shows.” The full report can be accessed here.

As of January 22, the US witnessed 173,534 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s an average of 440 people per day. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 433,180, puts the probable COVID-19 death figure somewhere north of 520k. Across all causes of death, we’ve suffered 116% of the deaths we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

¹ “Gross Domestic Product, 4th Quarter and Year 2020 (Advance Estimate).” US Bureau of Economic Analysis (BEA, January 28, 2021).

² The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

³ “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-141-NAT. US Department of Labor (January 28, 2021).