01082021 :: Friday finance week in review

01082021 :: Friday finance week in review

A partial digest of what we learned:

Emboldened as always, Trumpists overran the Capitol. People died. Trump may be impeached again. Both insiders and outsiders suspect he was attempting to engineer a coup. His Twitter account was suspended twice last week, the second time for good. With his license to communicate with the general public effectively revoked and the app of choice of his followers, Parler, also getting taken down, Trump's filth can't fly far. He has no immediate outlet. Even some of his own zombies are coming to and turning on him.

Multiple days remain until January 20, but there are few people who will, or even can, do his bidding anymore. His own officials are resigning. Furthermore, it’s unlikely that anyone in a significant position within the country’s power structure will take a call from him any longer, let alone an order.

There was a story with this guy. It was full of plot twists, suspense, drama, international intrigue, sexual assault, abuses of power and corruption, prison camps, foul language, and violence. There was a climax or three. Perhaps the Secret Service has yet to make an appearance, and there will still be a denouement, or an epilogue. But, this particular story encompassing the last four years is coming to a close.

On Wednesday, Congress resumed its review of all electoral votes, state by state, late Wednesday night. Results from specific states, such as Georgia, were objected to. They were all rejected:

Objections to Arizona, signed onto by Cruz and others, were debated and rejected.

In Georgia’s case, the signatories required had bailed following the events of the day, i.e. the violent breaching of the Capitol. Thereby, the objection to the state’s results was not allowed to proceed.

Michigan’s results were objected to but the Georgia lawmaker from the House to raise it indicated that while many from the House had signed on to the objection, there was no senator signatory. Hence, it wasn’t permitted to proceed.

Nevada’s results were objected to, the objection raised by a representative of Alabama and signed on to by many other House members, but no Senator signed on to it. Thus, it wasn’t allowed to proceed.

Pennsylvania’s results were the next to be objected to. The objection did have Republican Senator Hawley as a signatory, so the joint session of Congress was adjourned in order for the two houses to separately debate the matter. Things got heated in the House. The joint session then reconvened after the Senate and House voted it down.

Keep in mind that this one in particular is a legal issue pending with SCOTUS, perhaps to be heard early this year. Not sure it was ever for Congress to decide whether a state supreme court overstepped its bounds. Otherwise, for what do we have the judicial branch of the federal government. Unfortunately for the state of the union, 138 Republican House members and seven senators voted in favor of overturning PA’s certification of the state’s election results, further defiling the electoral process.

Wisconsin’s results were objected to. No senator would sign on anymore, though there apparently had been one earlier in the day.

With formalities completed, and Biden-Harris thoroughly declared President and Vice President, the joint session was dissolved by Pence. No legal avenues to contest the results remain.

Existing vaccines have demonstrated potential against worrying SARS-CoV-2 mutations thus far. This is positive news, but vaccine nationalism and rollout challenges, the propensity for the virus to mutate, and the inconsistency in the world’s response to it, make for an uneven playing field. There are more lockdowns than not, London is buckling, the US keeps setting records. The virus still has the advantage.

$2k checks may be coming, or they may not be given opposition to them within the Democrats’ own party.

Generally speaking, Biden wants more stimulus and debt forgiveness, which really is it's own form of indirect stimulus. This puts the inflation investment thesis in play again as traders price in stimulus projections; stocks, oil, and yields to rise, gold to fall. There's not enough data on crypto yet, but it's possible that further fiscal stimulus would drive it higher than not. Generally-speaking, some investors remain nervous about how inflated assets are already.

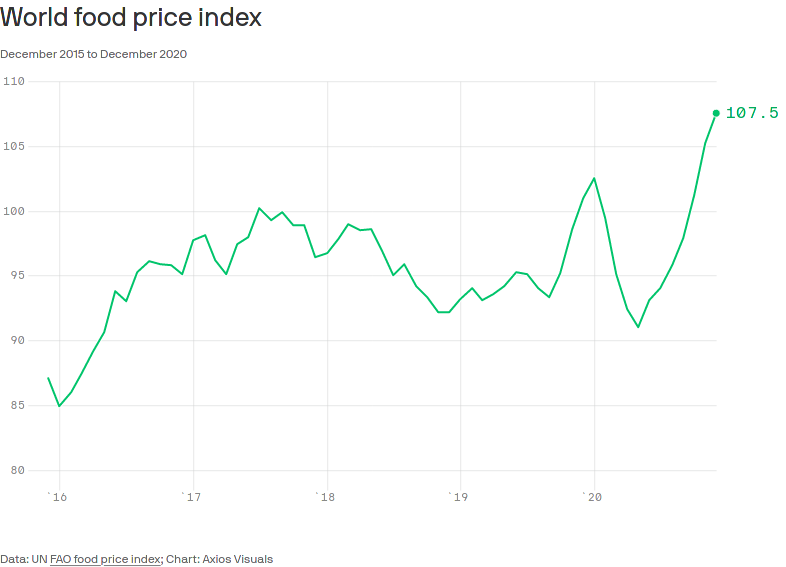

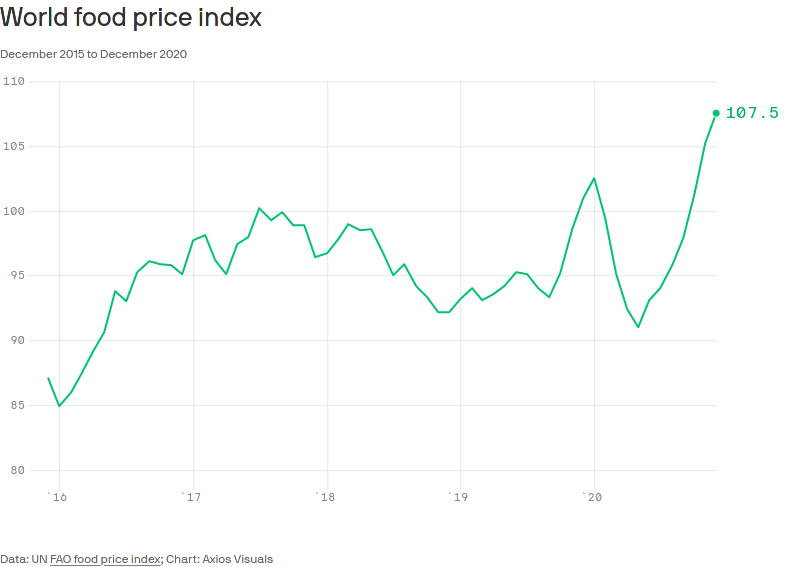

Speaking of inflation, we're seeing that siloed inflation in food, still. The FFPI is currently well below its 2011 peak of 131.9, but the trajectory is clearly up.

Gold fell, of course, but even as the Congressional confirmation of Biden’s victory was being disrupted by an insurrection. That’s how lame and unreliable the stuff is as a hedge of any kind. The opinion here remains that gold’s next truly large price moves will be down rather than up as we continue to pick our way through to more solid ground. Again, the most historically reliable inflation hedges have been equities and energy.

The split government theory—in this case that investors desire political gridlock as opposed to a Democrat sweep—has not been echoed by the markets thus far. Congressional affirmation of Biden-Harris and Georgia’s runoff election puts the entire legislative branch in Democrat’s hands, and Wednesday, the DOW, S&P, and crude moved up, yields climbed, and gold and tech moved down. These are risk-on/safe-haven-off moves signifying stamps of approval of the full election outcome.

By way of explanation, resting on Biden-Harris taking office is the promise of further fiscal stimulus, the perception of future stability, improved and more responsible management of the ongoing health crisis, sensitivity to marginalized groups, possibly less abuse of power, and the normalization of global political relations, among other things. A Democrat sweep amplifies the above items from which we all may benefit.

Simply put, these positives may outweigh any anachronistic fears of the wealthy invested over tax hikes, heavy-handed regulatory activity, and extensive social welfare deemed fiscally precarious.

Wednesday, the DOW alone climbed nearly 500 points, just to punctuate things. Said market behavior continued into Thursday as Biden-Harris were finally affirmed by Congress, this time with the NASDAQ coming along for the ride in a big way. The rally continued through Friday.

Crypto climbed no matter what was going on, whether it was the sacking of the Capitol, or a Democrat sweep and the promise of more stimulus, or in sympathy with jumps in other assets. It appears to be in a zone of its own. Total crypto market cap exceeded $1 trillion as of Friday, January 8.

Initial jobless claims in the US declined slightly to 787k (SA) for the week ending January 2, down from an upwardly revised 790k for the week prior. One year ago, we saw 212k.¹

To add to this, 161k+ people on an unadjusted basis applied for PUA, down from a upwardly revised 310k+ the previous week. There is either a data issue here, or some people fell off the map.

As of December 19, over 19 million people were still claiming unemployment benefits of some kind, down over 400k from the week prior. The EB program saw the biggest increase, which is of concern as this is the benefits program people end up in after they’ve exhausted regular UI benefits; it’s the program after the programs, on the way to running out of benefits altogether. In the comparable week one year ago, the US witnessed a little over 1.8 million people claiming unemployment insurance from all programs together.²

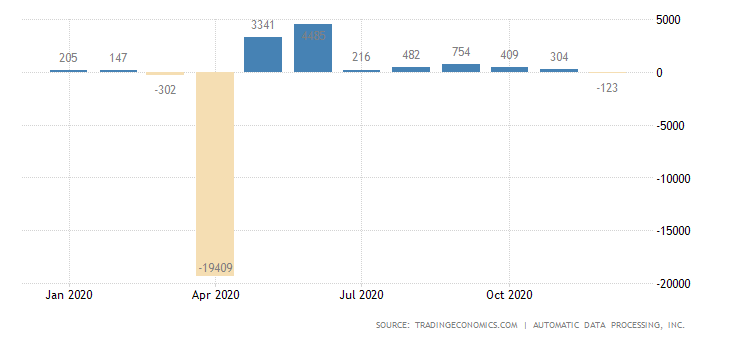

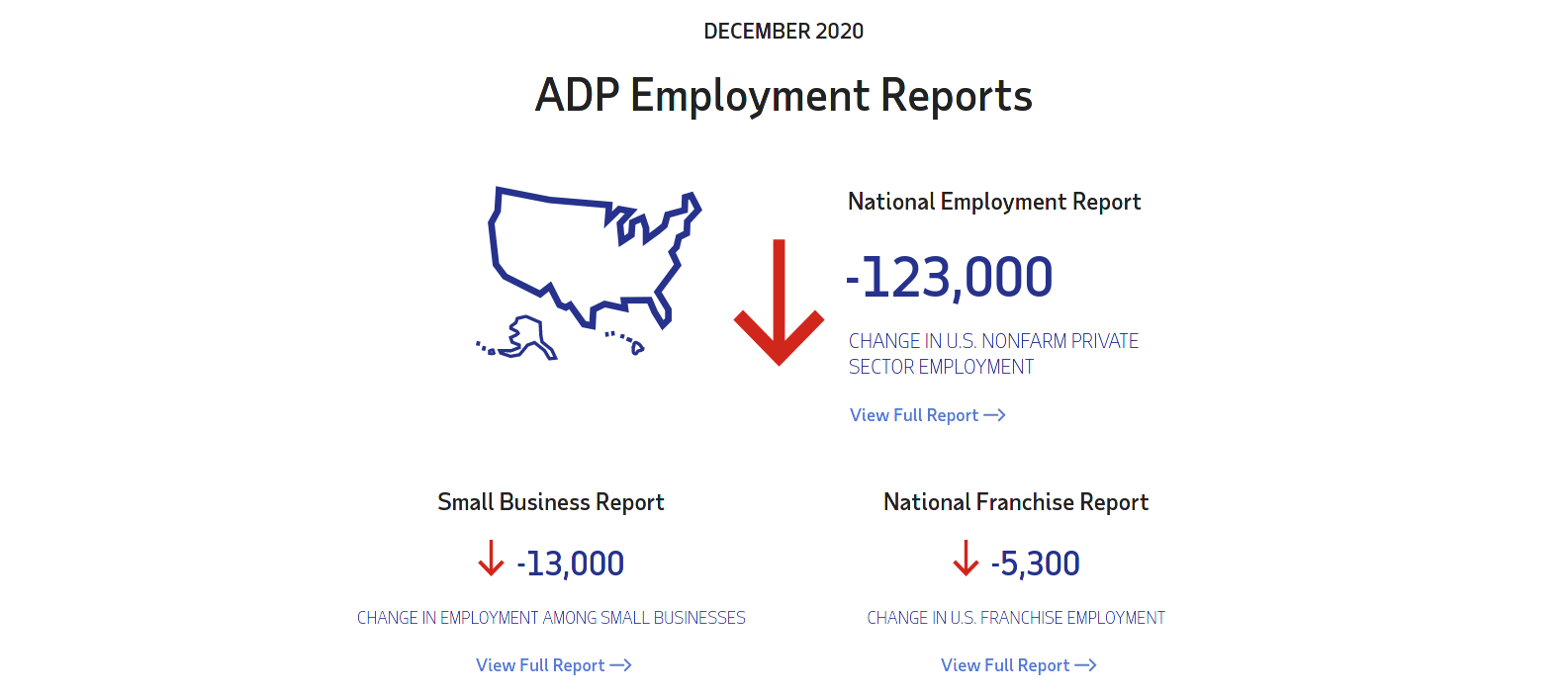

Private US companies cut a large number of jobs for the month of December, 123k, most of them from large sized companies. This is the first loss in private nonfarm payrolls since April 2020, when the pandemic’s economic impact began striking with full force. We’re heading the opposite way we want to be.

The December employment situation report put out by BLS revealed that 140k total nonfarm jobs were lost for the month of December, with the unemployment rate flat at 6.7%.

Digging further through the data, we find the following, among other details:

Over 37% of the country’s unemployed have been without work for more than six months.

We have 2.3 million more people than back in February not being counted as part of the labor force but who want work. The official unemployment figures do not reflect this group.

The teleworking rate increased to 23.7% from 21.8% in the month prior.

15.8 million people revealed that they had lost work in December because their employer closed or was losing business. This is viewed as an implication of the pandemic, and the total is 1 million individuals greater than for the month of November.

The latest job losses disproportionately impacted women.³

More stimulus and assistance programs are needed. If the political will exists for that, equity and other asset prices will inflate.

Mortgage applications decreased a blended 4.2% (SA) for the two weeks ending January 1, 2021, with refis dropping 6% while homebuyer applications fell 0.8%, according to MBA. Two weeks of data were released at a time this go around on account of the holidays, and adjustments were made to the data to account for them. The 30Y fixed came in at 2.86%.

There is no change to the previously stated opinion that the overall housing market in the US is setting up to decline. The industry is working its way through the finite qualified pools of owners for refis and borrowers for homebuyer applications. What’s more, the construction industry keeps chugging along with spending rising 0.9% for the month of November 2020, potentially leading to an oversupply issue if demand begins drying up and existing buyers cancel contracts.

As of December 27, MBA estimates that 5.53% of surveyed loans are in forbearance, for a total of 2.7 million households. Stimulus, forbearance, and other coronavirus relief measures will keep people afloat, but it will not enable the purchase of real estate where prospective buyers are not already individuals of means and resources, and again, we are exhausting those pools.

In order to sustain the housing market, the employment picture must sustainably improve all the way around. To accomplish that, the health crisis must be addressed. It is uncertain that it will be this year, and unclear when it will be. SARS-CoV-2 is still a moving target.

Commercial real estate’s picture is bleak at best.

One interesting means of shorting US real estate is DRV.

[tracking: DRV, XLRE, NLY, VNO, SPG]Oil inventories finally took a meaningful plunge at last reading, perhaps due to increased travel for the holidays, among other things. Crude stocks dropped over 8 million barrels for the week ending January 1. Prices have been rising for reasons stated earlier, including oil’s role as an inflation hedge, but also as fresh cuts occur. Still, the oil industry is turning dinosaur.

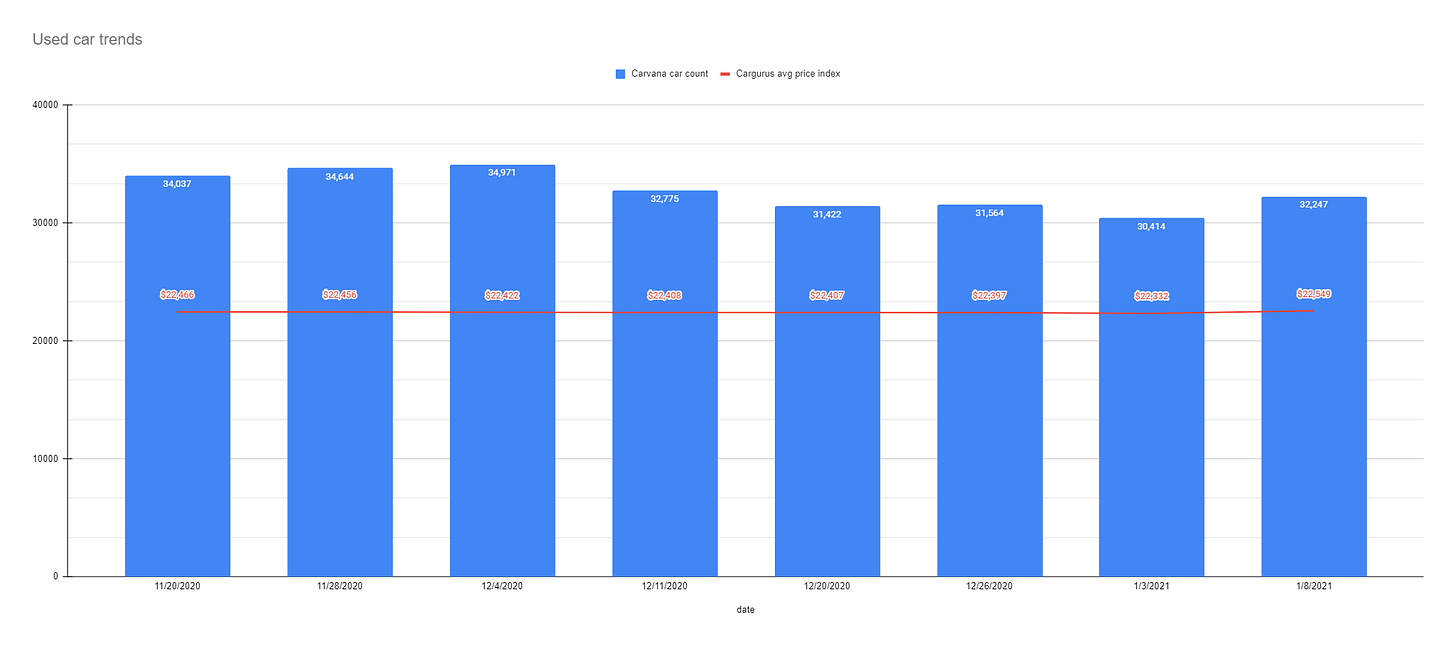

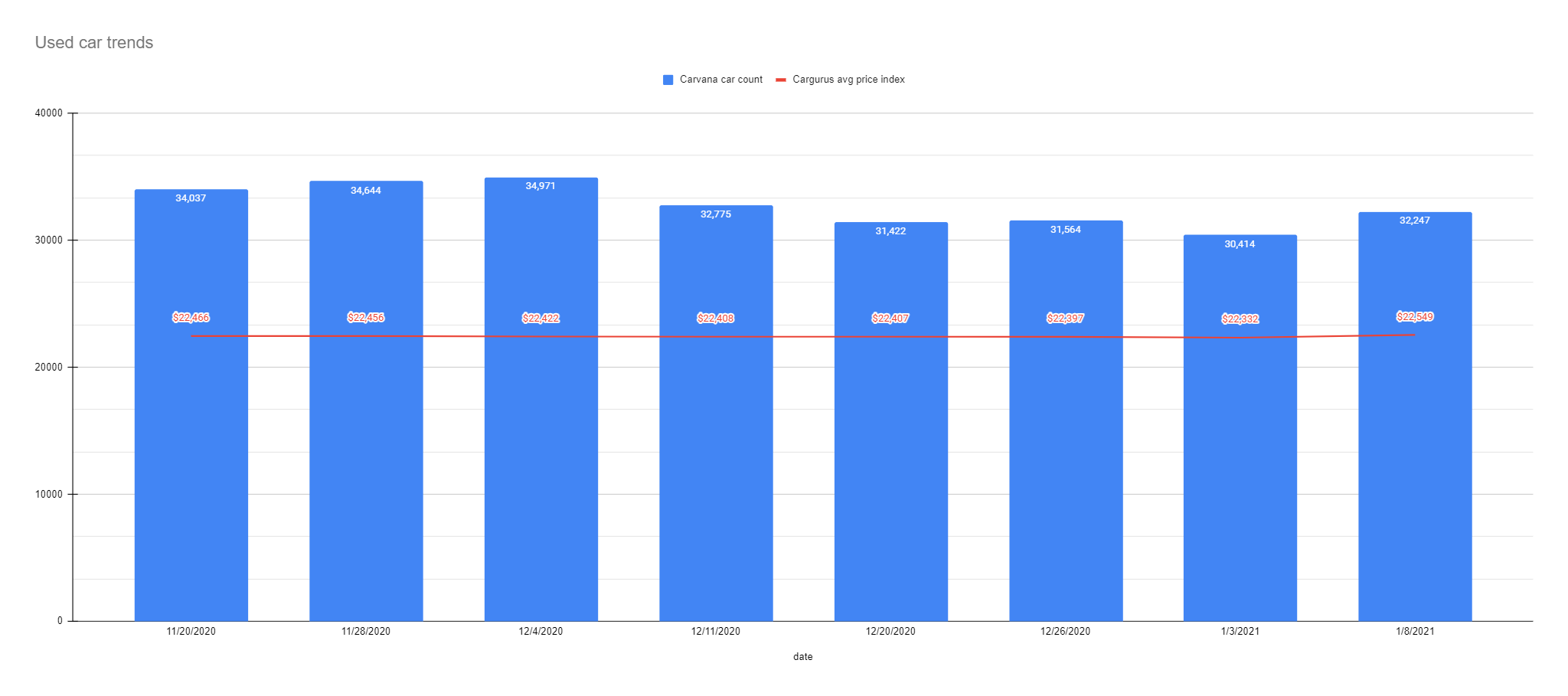

Used car trends: The latest Carvana car count as of January 8 jumped to 32,247 vehicles from 30,414 the week prior (6.03%), while the CarGurus average price index also rose to $22,549 from $22,332 (0.97%), reversing weeks of decline.

Sovereign matters:

The Swiss National Bank turned a pretty penny in 2020 from what earned them currency manipulator status, realizing a profit of nearly $24 billion. Global conditions which made it possible are making life hard for SNB elsewhere in terms of its monetary policy.

The current state of equity: Amazon attempts to confront housing issues it has helped to create.

As of January 8, the US witnessed 166,075 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s approximately 442 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 372,398, puts the probable COVID-19 death figure somewhere north of 470k. Across all causes of death, we’ve suffered 112% of the deaths we would have expected in non-pandemic times given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

¹ The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

² “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 21-1-NAT. US Department of Labor (January 7, 2021).

³ “Employment Situation News Release.” BLS (January 8, 2021).