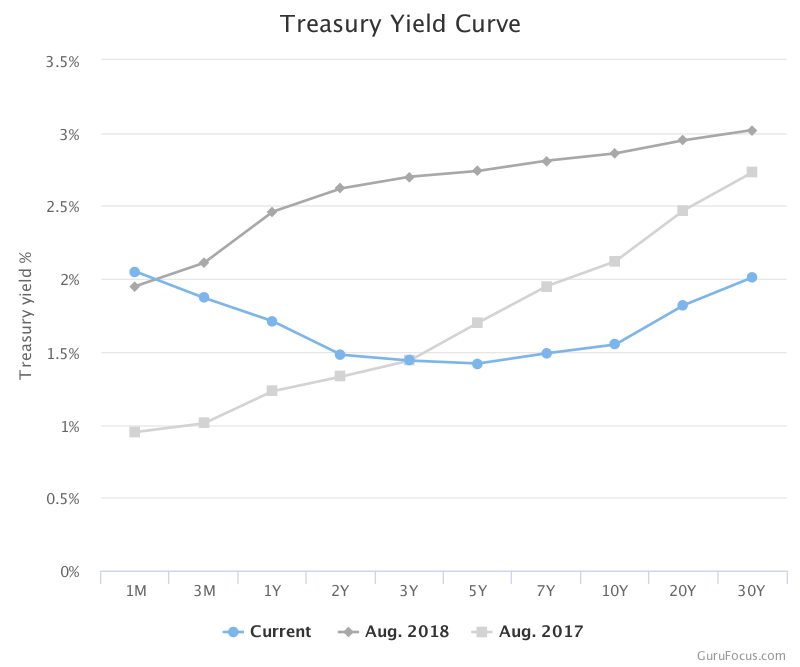

August 14th saw the yield on a 10 year US Treasury bond briefly dip below that offered on a 2 year US Treasury note. Everybody, their mothers, and their dogs began writing about yield curve inversion, as if it had come upon us suddenly. They mentioned its status as a harbinger of recession, they offered explanations of what it is, and they recommended what could be done about it, among other things.

But the yield curve has been inverted for a little while now. Further, what seemed to be lost in all the hubbub are the inflation numbers that came out this past Tuesday. It turns out that inflation in the United States rose, with overall and core annual inflation numbers as of July exceeding market expectations in both cases.

What’s more, the Fed recently cut rates by a quarter of a point, exactly two weeks before the 10Y and 2Y yields danced past each other. The ripples of a cut aren’t felt in the economy for a little while, so we won’t be able to discern the full impact of that July 31st cut anytime too soon. However, if we already had an uptick in inflation preceding the latest cut, and the yield curve stays inverted, and we do head towards (or into) a recession after all, then any additional cuts may do more harm than good.

In other words, instead of helping to secure an ongoing expansion or spare us from a recession, more cuts may have diminishing returns and actually invite something far worse: stagflation, an environment in which economic stagnation joins forces with inflation to make for a particular kind of nasty. Interest rate cuts from here on out may only propel inflation higher and do little to benefit GDP anymore. At current levels, that would start to go against the price stability portion of the Federal Reserve’s dual mandate.

What to squeeze to encourage economic growth moving forward? Trump’s tax cuts haven’t delivered in that department; they’ve pretty much just artificially inflated stock markets and boardroom salaries, from what anyone can tell. The trade landscape is increasingly uglifying. Meanwhile, we already have decent consumer spending and record unemployment (the other half of the Fed’s dual mandate). How much lower can that latter number go, being the lowest in 50 years, just to get paychecks in the hands of wouldbe consumers? Or wait, there’s Apple Card.

If the inverted yield curve remains an accurate predictor and we are indeed in danger of another recession, any additional interest rate cuts may only ignite — and then fan — stagflationary flames. At this point, it’s hard to believe that the release of more easy money into the system, without a clear road map around which to base its prudent investment, would lead to any further lasting economic growth. Therefore, the best means of escaping a recession may not lie with the Fed, but rather with the White House and a reversal of its protectionist policies on trade and other issues; it’s there that at least some of the roots of any impending recession most likely originate.