10022020 :: Friday finance week in review

10022020 :: Friday finance week in review

A partial digest of what we learned:

Trump and others around him have contracted COVID-19. Though this became known Thursday night, his situation quickly changed from quarantine to hospitalization at Walter Reed by Friday evening. Following are some of the individuals who have also tested positive this past week (as of publication):

Melania

Close aide and personal counselor Hope Hicks

Trump campaign manager Bill Stepien

Utah Senator Mike Lee

North Carolina Senator Thom Tillis

RNC chairperson Ronna McDaniel

Kellyanne Conway

Notre Dame President Reverend John Jenkins

Among other things, Trump’s diagnosis calls into question the next scheduled presidential debate. The first one took place Tuesday. Terms used to describe it have included “acrimonious” and “a terrible missed opportunity.”

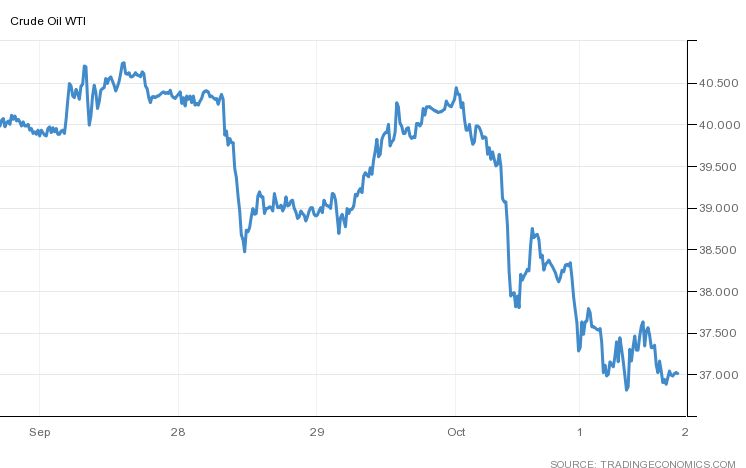

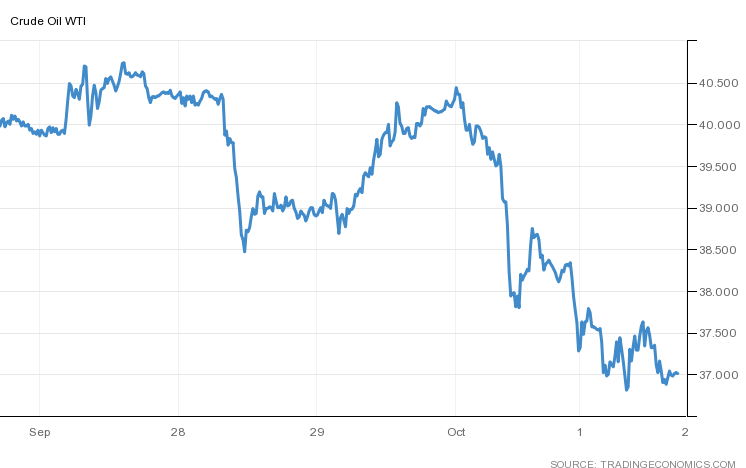

While equities markets ended down for the day today—with the NASDAQ losing the most froth (-327.51 points, -2.83%)—one of the assets to fare the worst was oil, which will be elaborated upon below.

There is still no agreement within the political establishment of the United States over further stimulus measures or safety nets for the general public, the country’s municipalities and states, or industry. There was some activity during the week, then the House passed it’s own $2.2 trillion package, and now Trump is under medical supervision. Pelosi has stated that this latest development may actually facilitate an accord somehow, but that remains to be seen.

The US Treasury Dept itself urged Congress to hurry on a stimulus deal earlier this week, highlighting the struggling airlines that it has now closed on loans to. All the same, United and American Airlines furloughed 32k employees on Thursday.

Job gains slowed in September. Additionally, initial jobless claims continued to exceed 800k, while American companies cut close to 119k employees for the month. Nevertheless, the official unemployment rate fell yet again to 7.9% overall, although this rate is worse for marginalized groups and never takes into account discouraged workers nor those who have chosen to leave the workforce early under voluntary separation agreements, for instance.

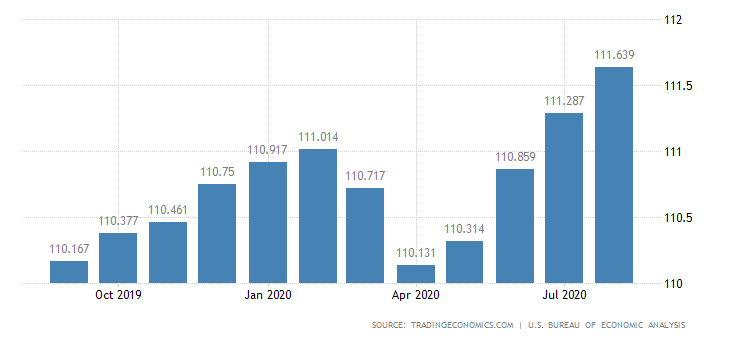

Consumer prices as measured by that “other” price index that the Fed keys off for its own inflation targeting, the PCE, rose for the fourth straight month in August.

The oil complex took a serious hit beginning Thursday, even though stocks had been falling as shown below.

Both Brent and crude slipped over 4% on Friday, the latter down to well under $40/barrel. Headwinds for the commodity may gather further, as global travel and industry remain subdued and electric vehicles gain in popularity.

Perhaps of greater significance right now, however, is that Trump is overwhelmingly pro big oil. As he has taken ill and/or his chances of reelection become cloudier, traders may wonder if the industry is at risk of losing a major force friendly to its interests and cut their positions accordingly.

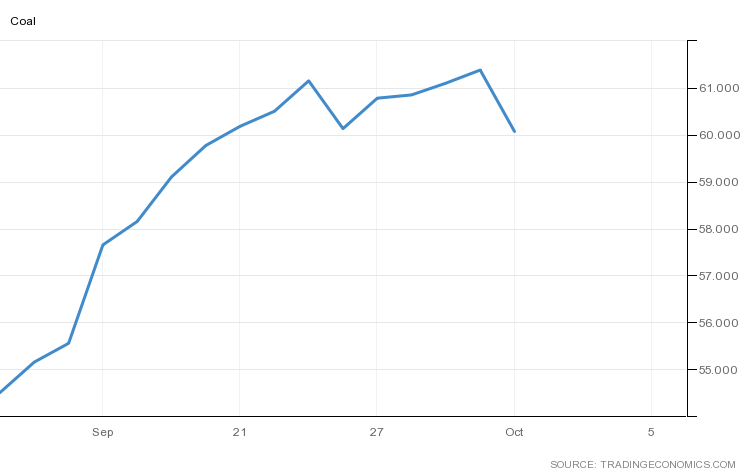

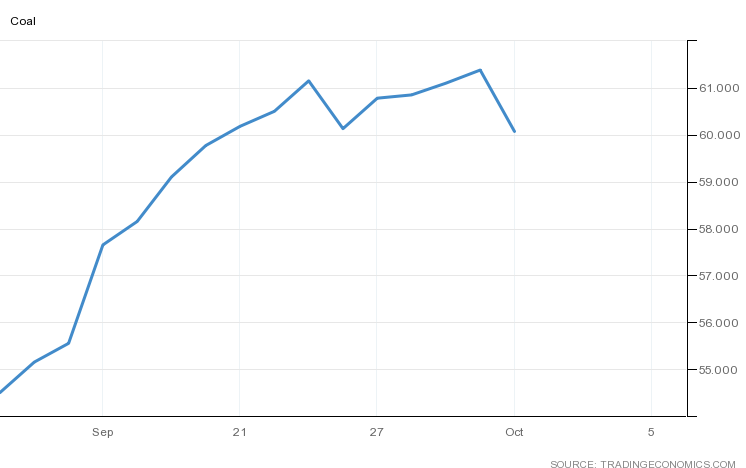

As if to confirm this, coal futures, representing the fortunes of another favorite industry of Trump’s, likewise declined on the day (-2.13%).

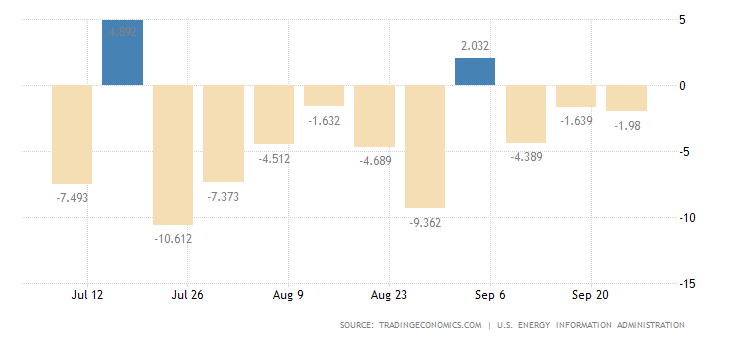

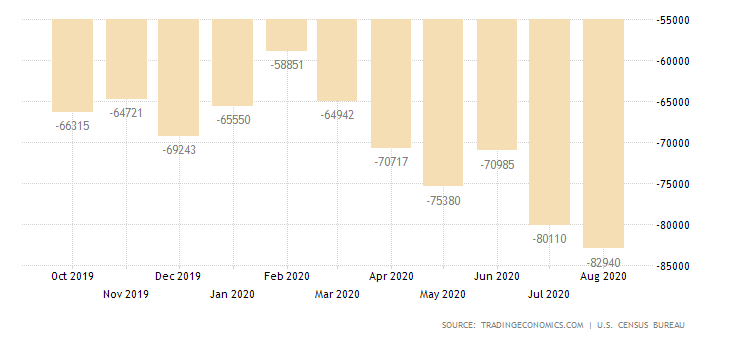

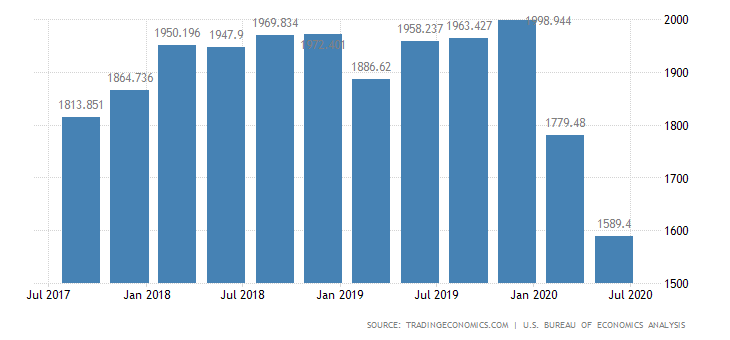

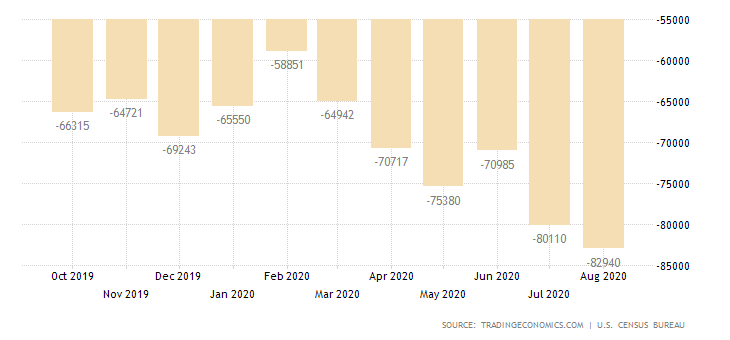

[tracking: XLE, ERX]The US trade deficit in goods as of August is the largest it has ever been. Capital goods, the country’s greatest export category, sank almost 4%. These goods include commercial aircraft and semiconductors.¹ Of relevance, a weak spot in Micron’s latest earnings was its inability to continue selling chips to Huawei given the highly-publicized restrictions on doing business with the Chinese firm.

Housing news was a mixed bag, with mortgage applications slowing for the latest week, but August construction spending and pending home sales under contract jumping, and July home prices rising. On the backend, performance of MBS has been lagging despite massive Fed support, due to headwinds like forbearance, faster prepayments, and excess supply (with only more expected).

The Fed is no doubt committed to sopping up securities and maintaining low rates, but the white flight elements of the housing market in the US must exhaust themselves eventually. It is an open question whether the employment picture, among other things, will improve in time to pick up the coming slack.

[tracking: XLRE, NLY, VNO]In the US, restrictions on banks’ share buybacks and dividend payments have been extended by the Federal Reserve for another quarter. Recent income will factor into calculations capping payouts, while stock repurchases are prohibited outright.

[tracking: XLF]Corporate profits for Q2-2020 fell 10.7%, putting them on par with those of four plus years ago.

[tracking: SPY]Gold and silver spent time climbing out of their holes this week, though they remain below their valuations of two and more weeks ago. Trump’s coronavirus diagnosis did not immediately boost their demand in any sort of safe-haven bid.

[tracking: GLD, SLV, DUST, JDST, GDX, GDXJ]Long-term bond yields climbed slightly. Again, one has to wonder if the trajectory of overall demand is down for the foreseeable future, and the perceived safety of Treasuries is in question. An uncertain/unstable presidency may not help matters.

[tracking: TMV]The final reading of US GDP growth for Q2-2020 is an annualized 31.4% plunge. Comparitively, this places the country near the bottom of the stack of the world’s nations for which data is readily available.

Sovereign matters:

Nigeria’s outlook has been revised upward by Fitch. It has become clearer to the ratings agency what the impact of the pandemic will be on the country’s economy.

Bolivia has been downgraded by Fitch for reasons including political (and racial) tensions, the uncertain outcomes of upcoming elections, and the socioeconomic impact of the pandemic.

[tracking: EDC, VXUS, VWO]

Footnotes

¹ Amadeo, Kimberly. “US Exports: Top Categories, Challenges, and Opportunities.” The Balance (February 26, 2020).