09252020 :: Friday finance week in review

09252020 :: Friday finance week in review

A partial digest of what we learned:

There is still no agreement within the political establishment of the United States over further stimulus measures or safety nets for the general public or the country’s municipalities. It was reported that talks between Mnuchin and Pelosi have resumed over a reduced package ($2.2 trillion) meant to facilitate further negotiations.

Personal consumption expenditures (“consumer spending”) account for some 67% of GDP.¹ If millions of Americans cannot consume because they do not have sufficient employment nor benefits, things are only going to get uglier.

On the state and municipality front, road construction projects across the country appear abandoned. Miles and miles of coned and rerouted highway in various states sits with no crew or machinery in sight.

Trump may not yield office should he not triumph in November’s election. Specifically, he was quoted as saying,

We want to have—get rid of the ballots and you'll have a very peaceful…there won't be a transfer, frankly. There'll be a continuation.²

This, and all other divisive and further polarizing language, helps matters none. Additionally, it may only serve as a further economic headwind.

Housing is back on, at least for now, though some are arguing it’s another bubble. Existing home sales rose again, as did single-family home prices, while mortgage applications—fueled in particular by refi activity—rebounded.

[tracking: XLRE, VNO]The general equities rout persisted this week, making it a full month of declines for the Dow and S&P 500. The NASDAQ, on the other hand, regained its footing to snap its recent losing streak. All indices rose into the close Friday, no doubt consisting of some short covering.

It’s the opinion here that the inflation scenario is still in play, unless we’re soon to see the end of stimulus.

[tracking: SPY, XLK]Gold was gutted this past week, and silver even more so. Chances are increasingly going up that the next major wave is down, even if the precious metals complex sees a near-term bounce for whatever reason. Junior miners especially took it on the chin.

Silver fared much worse than gold, plummeting nearly 15% for the week compared to gold’s near 5%.

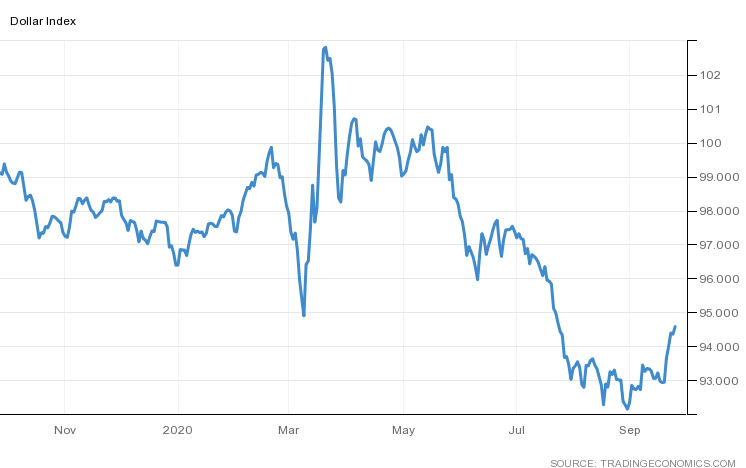

[tracking: GLD, SLV, DUST, JDST, GDX, GDXJ]The DXY strengthened a fair amount. After nearing 92 twice in August, it has breached 94.5 this month.

It may be tempting to oversimplify the situation by positing that the DXY and gold move inverse to each other and, hence, it should come as no surprise that the precious metals complex and the $USD had such different experiences this week.

However, that relationship isn’t a reliable one. You may recall that from the end of 2018 through 2019, gold and the dollar actually rose together. At any rate, the degree to which gold fell seems disproportionate to the strength in the dollar for the week.

Gold aside, there’s plenty of news to drive investors back into dollars as opposed to other currencies, including Brexit and COVID-19 resurgence in the eurozone.

[tracking: UUP]Sovereign matters:

Incredibly, Argentina is already at risk of default yet again, in spite of the recent restructuring of their $65 billion in debt. The country’s yield curve has inverted and concerns are mounting. Consumer sentiment and retail spending are deteriorating, GDP is contracting, the peso is falling. The ratings agencies may have to reconsider the upgrades they issued in the wake of the country’s debt restructuring.

Hungary’s outlook has been revised up by Moody’s, which cited an improving debt picture at home and abroad.

Laos saw its credit rating cut by Fitch, which cited a liquidity crunch.

Zambia has been downgraded by S&P, which cites the country’s difficulty in meeting its commercial obligations.

Spain’s GDP cratered for the quarter ended June 2020. Though the economy had already shrunk the previous quarter, this was the worst contraction on record.

Lebanon’s inflation rate hit 120% in August 2020.

Countries across the world are mostly either cutting rates or holding steady, for the time being. Turkey was one of the only nations to actually raise rates in a surprise attempt to restore price stability.

The EU plans to regulate, rather than shun, cryptos, including stablecoins. In doing so, it seeks to secure financial stability while maintaining access to the innovations.

[tracking: EDC, VXUS, VWO, ARGT]COVID-19 treatments are becoming more discernible, including long suspected vitamin D and now interferon therapies.

Additional major outlets are reporting on the reality that globally, we’ve undercounted fatalities at the hands of SARS-CoV-2 by not accurately attributing them to COVID-19. That said, they are still not catching on to the degree to which that is happening right here in the United States. Instead, other countries including Russia are highlighted.

Footnotes

¹ US Bureau of Economic Analysis. “Shares of Gross Domestic Product: Personal Consumption Expenditures.” FRED, Federal Reserve Bank of St. Louis (2020).

² Pecorin, Allison and Trish Turner. “Unanimous Senate Commits to Peaceful Transfer of Power after Trump Refuses.” ABC News (September 24, 2020).