07242020 :: Friday finance week in review

07242020 :: Friday finance week in review

A partial digest of what we learned:

Pending new home sales for the month of June again jumped considerably since setting a record for the month of May. Another historic era of white flight from urban centers is in motion, and mortgage companies are “just making hay right now.”

Initial jobless claims in the US (for the week ending July 18) increased for the first time since the last week of March, 2020.

AMEX earnings signal a collapse in consumer spending.Volumes were down considerably. The company also upped its loss provisions.

The bankruptcy knell sounded for BJ Services, marking another firm in the troubled American energy sector to seek protection.

Gold trended higher, nearing its all-time record. While there’s little evidence it is effective in hedging inflation, it may hedge the irrational quite well. The American White House such as it is, a bonkers COVID-19 situation in the US, justifiable civil unrest, and a further souring of the relationship with China continue to drive it up. It now sits near its all-time high of $1,920, set in September 2011.

The US services sector remains in a state of contraction. The IHS Markit US Services PMI has yet to break 50 since January 2020.

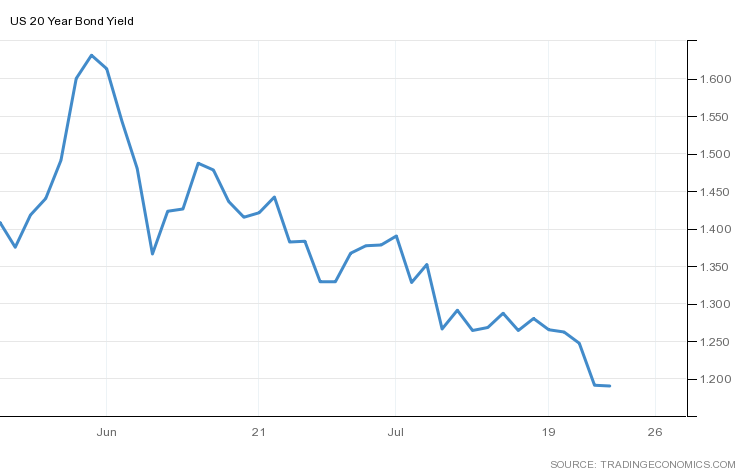

Long-term Treasury yields continued to sink since their recent peak in June. We are at or near April levels in the 10Y, 20Y, and 30Y. Safety is being sought.

The US and China ordered the closure of each others’ consulates. The escalating tensions put downward pressure on equities and gave gold an additional tailwind.

The EU passed a new stimulus package, notable for its centralization of representation; the European Commission will raise capital in the markets on behalf of all 27 member states.

Senate Republicans attempted to show leadership on further stimulus after a dangerous game of wait-and-see. Nothing concrete has emerged as of yet.

The DXY continued to drop, though the dollar gained on the yuan for the week, indicating appetite for risk is still lacking.