01012021 :: Friday finance week in review

First off, happy new year.

A partial digest of what we learned:

Trump signed off on the stimulus and Congressional budgetary spending bill (Consolidated Appropriations Act, 2021). Treasury and the IRS indicated that stimulus checks already started going out last Tuesday night. Meanwhile, an upgrade to $2k checks couldn’t even get a vote in the Senate. Yes, the size of stimulus checks that the government has already begun sending out was still being debated as of Friday night, and may be taken up again by the new 117th Congress, which convenes Sunday. Time will tell, and it’s unclear how that would even play out if checks for lesser amounts are being issued as we speak.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, SJB, TMV, VXX, XLE, TAN, GLD, VB, VTWO, TNA, XLF, KRE, BITW]Regarding the election 2020 timeline, January 6 is shaping up to be as expected. The country’s electoral process is under assault and being put through its paces. Simply put, it is in the nation’s best interest that the presidential transition proceed as it has since the founding of the country. Trump should be shown that there is something bigger than him, and if that thing in this moment is our adherence to American political tradition, then so be it.

Note that any violence in DC brought about by protests of the electoral vote counting in Congress, or any shenanigans among lawmakers around recognizing the election 2020 results, is particularly supportive of the precious metals complex.

[tracking: GDX, GDXJ, GLD, DUST, JDST, SLV]It seems increasingly appropriate to begin assessing SARS-CoV-2 and its potential to influence our behavior and impact our expectations from the perspective of a disease causing agent with which we cohabitate, not one we eliminate. It is a mutating, highly-infectious zoonotic entity that we may be stuck with.

Our World in Data reports that some 12.34 million vaccine doses have been administered as of January 3, enough to inoculate half that number of individuals.

Collectively though, this probably represents a first salvo only. In actuality, we might be heading down the path of the flu shot, each of which is a vaccine against a small group of influenza viruses that it’s believed will circulate most widely during an upcoming flu season, according to research. To that, we may now add COVID shots. This could be the beginning of a permanent relationship with SARS-CoV-2, especially if we know no treatments that destroy the infection in a manner similar to how we have become adept at curing bacterial infections.

Therefore, we are left with the same things we were always left with—personal responsibility, masks, and awareness building. The vaccines we have thus far will likely not spell the end of the pandemic.

Whenever the realization of all this settles in, the markets may give up some gains, for it will coincide with people continuing to fall ill, businesses still failing, prolonged higher rates of unemployment, NPLs, and further disruptions to ways of life that will usher in longer-lasting changes.

[tracking: VTI, SPY, VOO, QQQ, XLK, EDC, VWO, VXUS, LQD, SJB, TMV, VXX, XLE, TAN, GLD, VB, VTWO, TNA, XLF, KRE, BITW]Crypto is stealing the show. BTC, ETH, and LTC especially have been on a tear leaving many to wonder when consolidations or corrections will occur. Nothing goes straight up, and crypto as an asset class has already been through a bubble burst. But again, bubbles are things that financial phenomenons often encounter on their way to becoming established. This stuff called crypto isn’t going away.

For any cryptocurrencies that attain mainstream status—i.e. the core cryptoassets of the world such as BTC and ETH, not the random ego coins—a clear thesis is emerging: their value will be driven by rate of adoption, both as a common unit of trade and for portfolio diversification purposes. Decentralized and universal in appeal and use, cryptoassets are gaining global recognition.

On the simplest level, they promise to streamline and secure transactions while making them more transparent. Imagine traveling abroad and utilizing ETH via your smart device to pay for something priced in ETH, as opposed to having to constantly track a USD/EUR exchange rate and conversions; or, the corporate pieces of a global supply chain transacting with each other in LTC, no matter what different nations they themselves operate in; or central banks holding crypto as part of their reserves in order to manage the value of their fiats.

On the investment front, VanEck is the latest financial player to wade into the crypto ETF application pool with an SEC filing to launch the VanEck Bitcoin Trust. The SEC has shot down all prior applications for ETFs. To-date, BITW is what’s available as a fund, and it trades in OTC pink. Otherwise, one can trade BTC/USD futures on the CME, with ETH/USD futures on the way.

It seems the industry would have to submit to greater regulation to achieve full valuation potential. Treasury already wants the regulation part with greater scrutiny of unhosted wallet transactions over $3k in value, including who the participants are, among other things. Privacy advocates in the space find this troubling, but regulation and oversight may be what fosters greater comfort with the asset class, leading to greater acceptance and adoption and, ultimately, higher valuations.

A Biden presidency does not clarify the picture of the future of crypto. Yellen is believed to be anti-crypto, while one potential pick for heading the SEC, Gensler, is viewed as pro.

Stimulus checks to households may be supportive of cryptoasset prices in the near-term.

[tracking: BTC, ETH, LTC, BITW]The DXY is back to sub-90, which, again, is a clear signal that traders are preferring other currencies and/or assets (like crypto or hard assets), or financial securities not denominated in $USD, at this time. Any market corrections or downtrends should bring investors flocking back to the dollar, and the opinion here is that the door is open for markets to take a turn for the worse this year.

The Main Street Lending program will now terminate on January 8 so that loans that hit the portal on December 14 and sooner may be processed and funded. Again, these Fed lending programs have come to a conclusion because Treasury would not reauthorize them. At present, some Republicans in particular are seeking to ensure there are no new incarnations, either.

Initial jobless claims in the US declined to 787k (SA) for the week ending December 26, down from an upwardly revised 806k for the week prior. One year ago, we saw 220k.¹

To add to this, 308k+ people on an unadjusted basis applied for PUA, down from a downwardly revised 397k the previous week.

As of December 12, over 19.5 million people were still claiming unemployment benefits of some kind, down close to 800k from the week prior. In the comparable week one year ago, the US witnessed a little over 1.8 million people claiming unemployment insurance from all programs together.²

Multiple UI benefits programs were extended with the signing of the Consolidated Appropriations Act, and one, the FPUC, was even reinstated.

There is no new data release for mortgage applications on account of the holidays.

Cross-border European trading in securities moves out of London to financial centers within the eurozone with Brexit now a done deal. Market participants and onlookers will be watching for any hiccups on the first trading day of the year, January 4. Swaps trading has already hit snags.

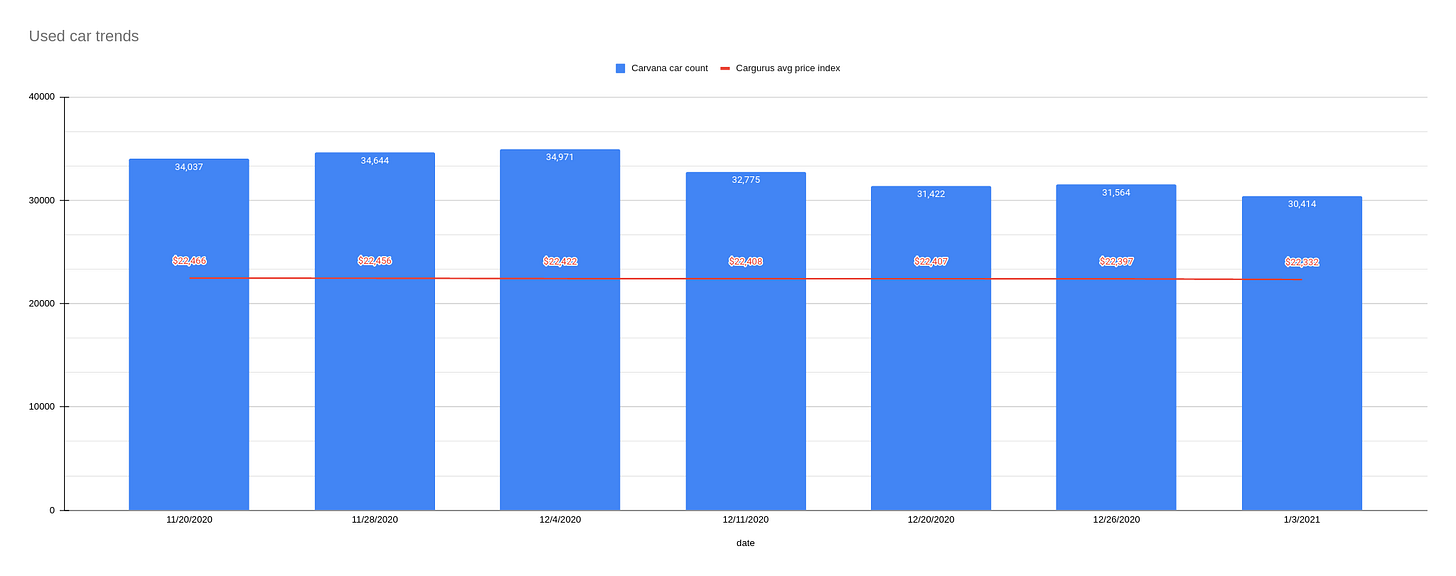

[tracking: GBP, EUR, EWU, IEV]Used car trends: The latest Carvana car count as of January 3 fell to 30,414 vehicles from 31,564 the week prior (-3.64%), while the CarGurus price index continued its decline to $22,332 from $22,397 (-0.29%). Prices on used vehicles have continued to decline in spite of shrinking inventory, and may indicate consumer preference for a particular car class that is overshadowed by slumping demand overall.

Sovereign matters:

Lebanon is increasingly in the grips of a humanitarian crisis. No aid appears to be forthcoming from the international community as it is said to be playing hardball with Hezbollah. The country is now looking to stretch for six months some $2 billion in forex that was earmarked for subsidies, in order to meet the most basic needs of the population.

UK’s Parliament approved the Brexit trade agreement struck with the EU. Also, AstraZeneca’s vaccine was granted emergency use authorization by Great Britain’s MHRA. The UK is the first to move forward with said vaccine.

Peru’s Congress has taken a step towards centralizing the economy by equipping its central bank with the right to set maximum and minimum lending rates in a bid to control the market for loans. This, as opposed to setting target rates and permitting market forces to determine actual going rates.

Jack Ma’s business empire continues to be scrutinized. Chinese regulators are looking into Ant Group’s equity investments and the rationale behind them, ostensibly for evidence of anticompetitive behavior. Antitrust action is already being taken against Alibaba.

Meanwhile, the PBOC is requiring that the nation’s banks reign in property lending. It will be enforcing loan portfolio caps in order to reduce systemic risk factors. Furthermore, forbearance as a practice is winding down in China in 2021 and banks will have to continue to shore themselves up against NPLs in an ever more challenging capital raising environment.

On the securities front, the PBOC has set forth rules to enhance the transparency of its bond markets. Elsewhere, the scope of QFII participation in China’s stock market has been expanded to include margin and shorting activities.

Additionally, appetite has returned for state enterprise bonds after a spate of surprise defaults in the fall. China has taken a decidedly un-American approach to bond defaults, permitting them to take place sans bailouts as a type of natural weeding out process, as well as investigating those corporations and underwriters involved.

Swiss currency interventions slowed in Q3. The country has been labeled a currency manipulator by the US, but rejects the characterization and has said it will forge ahead with franc supportive actions as needed.

Italy’s business community is urging the EU to relax its definitions on what it means to be in default on one’s credit obligations, saying that stricter classifications going into effect will impact a massive number of businesses and loan availability will dry up, exacerbating the problem. At issue are also calendar provisioning rules governing on what timeline financial institutions write down NPLs.

[tracking: GBP, EUR, EWU, IEV, MHCI, FXI, EDC, VXUS, VWO]Stat has run a side by side comparison of Pfizer-BioNTech’s and Moderna’s vaccines. Different age limits of patients and dosage storage temperatures count among the variations between the two.

As of December 23, the US witnessed 146,884 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s approximately 400 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 351,068, puts the probable COVID-19 death figure somewhere north of 450k. Across all causes of death, we’ve suffered 112% of the deaths we would have expected in a non-pandemic year given historical trends. Along with other situations where COVID-19 was not designated as a cause of death but where SARS-CoV-2 likely triggered a condition or exacerbated a preexisting one—heart disease, hypertension, diabetes, dementia—the “real” fatality count is probably much higher.

Footnotes

¹ The data quality of these numbers is still compromised, as outlined in a prior issue and based on a GAO report.

² “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 20-2341-NAT. US Department of Labor (December 31, 2020).