12042020 :: Week in review

A partial digest of what we learned:

With several states certifying their election results in the week ending December 4, including Arizona and Wisconsin—and California with its 55 votes doing so on Friday—Biden has officially accumulated enough pledged electoral votes to become the next president of the United States.

As outlined before, all states must certify their results and resolve any legal challenges and disputes regarding said results by this coming Tuesday. If any issues are left pending, Congress gets involved.

It would appear that six states, evenly split, have yet to certify their results. For Biden, they are Connecticut, Hawaii, and New Jersey; and Missouri, Texas, and West Virginia for Trump.

In the Pennsylvania case pending with SCOTUS, Democrats have now filed briefs in opposition to Republicans’ petition for a writ of certiorari.

Regarding Georgia, the machine recount requested by Trump is done and reaffirms a Biden victory. Hence, Trump’s legal team has filed a lawsuit in a bid to invalidate the results and either get a new statewide election for president or have the state legislature appoint its own electors. Ballotpedia has counted 64 election-related lawsuits to date, not including this one. It seems increasingly bizarre that any of these would amount to overturning the outcome.

Barr, for his part, has publicly stated that the DOJ found no major evidence thus far of widespread fraud underpinning election 2020, nor anything that would change the outcome. Furthermore, the civil lawsuits being pursued already were the most appropriate track, in his opinion. Having made this known, Barr has essentially excused himself and the DOJ from any additional action, further clearing the way for the Biden-Harris administration.

At the same time, his DOJ is investigating a conspiracy to lobby the White House for a pardon and, on a related note, campaign finance bribery in exchange for clemency. For whom, it is unclear. In parallel, one of Trump’s White House “liaisons” has been ejected from DOJ premises. Stirrup apparently attempted to insert herself one too many times into ongoing investigations and staffing matters.

Little by little, it seems that Trump is being cut out and the presidential transition is allowed to proceed incrementally. The next deadline after December 8 is December 14, when electors cast their votes from their respective state capitals. By December 23, those votes will have reached the president of the Senate, or Pence, in this case. Jan 6, Congress will tally those votes and Pence will announce the victor, at which point the results can be challenged one last time. A legitimate challenge will have to be evaluated separately by each chamber of Congress.

Equities and oil still stand to gain / yields loosen / gold decline from the clearing of presidential transition hurdles, and retreat / tighten / bounce from any serious complications that arise.

[tracking: SPY, VOO, VTI, QQQ, XLK, EDC, VWO, VXUS, LQD, VXX, XLE, TMV, GLD, VB, VTWO, TNA, KRE]

Congress has struck up conversation on stimulus again, but how many times have we already been through this loop? Seeing is believing. What’s very real is that Powell remains concerned about the lending programs administered by the Federal Reserve drawing to a close come the end of the calendar year, since Treasury has not reauthorized them.

If Mnuchin doesn’t extend any of them, some of the hard-earned progress made this year may be lost, and we may backslide. Thus far, the Treasury secretary is sticking to the idea of repurposing “unused” funds from the CARES act, especially to assist small businesses.

[tracking: SPY, VOO, VTI, QQQ, XLK, EDC, VWO, VXUS, LQD, VXX, XLE, TMV, TYO, GLD, VB, VTWO, TNA, KRE]The UK has become the first official western taker for the Pfizer-BioNTech vaccine, granting emergency authorization on December 2 with plans to begin inoculations the week of December 7. There are a host of unknowns, some of which have been raised here in past issues. Add to the list whether or not vaccines will altogether prevent transmission and infection.

Moderna is next to apply for emergency authorization, to be reviewed by the panel advising the FDA on December 17. Like Pfizer-BioNTech, the company will also be seeking emergency approval in the UK and elsewhere.

Once again, it’s time to avert another budget-related government shutdown. Most US agencies will see their funding expire on December 11, exactly in the middle of the December 8 and 14 electoral deadlines mentioned above.

Black Friday and Cyber Monday shopping figures set records. How is that possible in our current situation?

In part, it may have to do with the reality that millions in the US opted for mortgage and student loan forbearance. Indeed, bankruptcies are reportedly at a 14 year low (for now), thanks largely to shrinking non-commercial filings. Forbearance potentially leaves wouldbe consumers with some, or extra, disposable income for the holidays.

On the student debt side, it’s estimated that anywhere from 33-37+ million borrowers chose forbearance. Back in October, CNBC ran a piece indicating that only 11% or less of those people decided to keep paying down their debt, which has a typical monthly payment of $400. Taking the low end of the forbearance range, or 33 million people at $400 each, that’s $13.2 billion per month that isn’t being paid to service those loans. DeVos just granted a forbearance extension through the end of January 2021, too, meaning there’s a buffer of at least one more month.

As for mortgages, the MBA estimates that 2.8 million homeowners are in some type of forbearance at this time (an increase from the week before). According to 2019 data compiled by the US Census Bureau, the median monthly mortgage payment is $1,609. Using those figures, that’s over $4.5 billion per month that isn’t going to home loan servicers.

Combined, that’s $17.7 billion per month that wouldbe consumers aren’t paying towards their loans, which may help explain a portion of the stellar retail shopping figures.

[tracking: XRT, SPG, VNO, VNQ, XLK, QQQ]Gold and silver bounced this past week, but we’re still well off August’s high. Even then, gold was worth more back in 1980.

Reasons for the bounce could include the absolute snowballing of confirmed COVID-19 cases and illness, hospitalizations, and fatalities. The repercussions are reduced business and social activity, and stay-at-home restrictions. Unfortunately, the health crisis is deteriorating further, though most of us will make it through.

If instead the promise of $908 billion in stimulus is driving gold traders’ behavior, it should prove transitory and the impact limited. Gold is a poor inflation hedge and there’s no sustained inflation to come from a single incoming stimulus bill alone.

As for countering the implied indebtedness, S&P calculates that worldwide debt for 2020 will hit 265% of global GDP, or some $200 trillion. Yet gold sits at a mere $1,837/oz. The precious metal isn’t going to ameliorate the world’s debt situation, and another stimulus package probably won’t move the needle on gold in any major way. Besides, debt-servicing costs are currently quite low for certain sovereigns.

Similarly, dollar weakness as an explanation doesn’t hold water. At times, gold is moving in tandem with the DXY, not inversely to it.

What’s left to fuel gold? The collapse of modern society? Hoxne Hoard.

[tracking: GDX, GDXJ, GLD, DUST, JDST, SLV]

The DXY continued its decline to fall below 91 for the first time in over two years as investors, both at home and abroad, have been shifting away from dollar-denominated investments. China and EMs have been attracting a lot of attention, instead. This can be seen in exchange rates like that of the $USD/¥CNY since the end of May 2020.

[tracking: VWO, EDC, VWOB]Yields loosened considerably this past week, as they’re wont to do when the situation improves and investors seek riskier plays once again. The presidential transition, renewed stimulus efforts, and positive vaccine developments have all contributed. However, there may be other developments magnifying the movements, such as decreasing purchases of Treasuries by anyone other than the monetary authority and a larger shift to investments in other countries denominated in their home currencies.

[tracking: LQD, HYG, TMV]

GAO has reported that initial jobless claims data in the US is an inaccurate “approximation of the number of individuals claiming benefits during the pandemic because of backlogs in processing a historic volume of claims as well as other data issues.”¹ Hence, the news that they dropped to 712k (SA) for the week ending November 28 isn’t reassuring (not that 700k+ claims ever is). This was down from an upwardly revised 787k the week prior. One year ago, we saw 206k. The labor picture remains poor.

To add to this, nearly 289k people on an unadjusted basis applied for PUA, down from just under 319k the previous week.

As of November 14, over 20 million people were still claiming unemployment benefits of some kind, down close to 350k from the week prior. In the comparable week one year ago, the US witnessed less than 1.6 million people claiming unemployment insurance from all programs.²

Simultaneously, job growth appears to be fizzling out, with only 245k positions added for the month of November. The unemployment rate decreased to 6.7%, but because some people simply gave up looking for work as evidenced by the lower labor force participation rate.

[tracking: SPY, VOO, VTI]

Mortgage applications overall fell 0.6% for the week ending November 27, with homebuyer gains (9%) overshadowed by a decline in refis (4.6%). MBA also reported that the mortgage delinquency rate rose to 7.65% for Q3-2020. Meanwhile, NAR announced that pending home sales, or contracts entered into for existing homes, fell for the month of October. Construction spending went up (SA) for the same month. Rates wise, the going 30Y fixed stayed at 2.92%.

FHFA is extending to the end of January 2021 the window to request agency forbearance, as well as receive foreclosure/eviction protection. CMBS continue to occupy a troubled space.

The outlook here remains that real estate is eventually headed for a correction, at the very least, prompted by a chain reaction involving the spiraling health crisis and persistent labor weakness, in particular.

[tracking: XLRE, NLY, VNO, SPG]Oil finished up again for the week. This still seems largely driven not by actual inventories, but by the same factors driving most everything else in the US: vaccine success and progress on a presidential transition. Intertwined with the latter is the prospect of further fiscal stimulus, which may now be coming sooner than we had reason to anticipate. By this coming week, we might be adding a $900+ billion fiscal stimulus package to the mix.

That will inflate assets sensitive to stimulus, though the inflationary impact of stimulus is fleeting (until there’s more stimulus). Energy derived from fossil fuels is one of the most proven hedges against inflation. Another is equities.

Yes, OPEC+ members have returned to controlling supply, which dials in prices. Ongoing political and military conflict involving Iran and other nations, as well as holiday travel and the possibility of even more stimulus next year under Biden-Harris, are also supportive in the near term. Eventually, the pandemic as we know it will pass.

However, oil’s time is limited. We won’t be returning to the world we were familiar with. Things are evolving. In addition to those developments mentioned last go around, oil majors continue to scale back, adjust to a different future, and make revised projections about what to expect. Obstacles to the oil industry’s return to prominence are only accumulating, not the other way around. Players keep failing. Banks are checking out.

It used to be that “peak oil” was a supply-side term signifying that we were going to run out of the stuff, or what was accessible to us given the technologies of the day, anyway. At present, “peak oil” is being repurposed as demand-side lingo to describe a world in which we’re increasingly done with black gold.

There may be a couple of good runs left for the commodity. Again, it’s a proven hedge against inflationary pressures. The Fed has implemented a policy shift on inflation, ready to let things run hot at times. Fiscal stimulus is transiently inflationary. Beyond that, oil majors may clamp down on their activities so much that when demand does pick up again, there is a temporary squeeze that causes prices to spike; in other words, a supply shock.

However, if modern society keeps its act together, oil will ultimately go the way of coal.

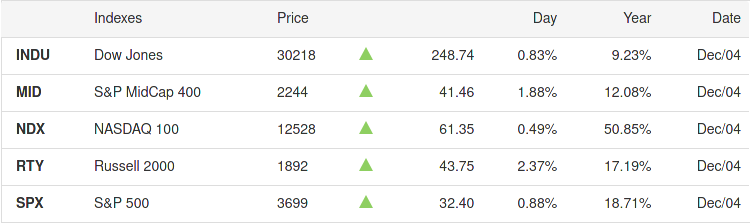

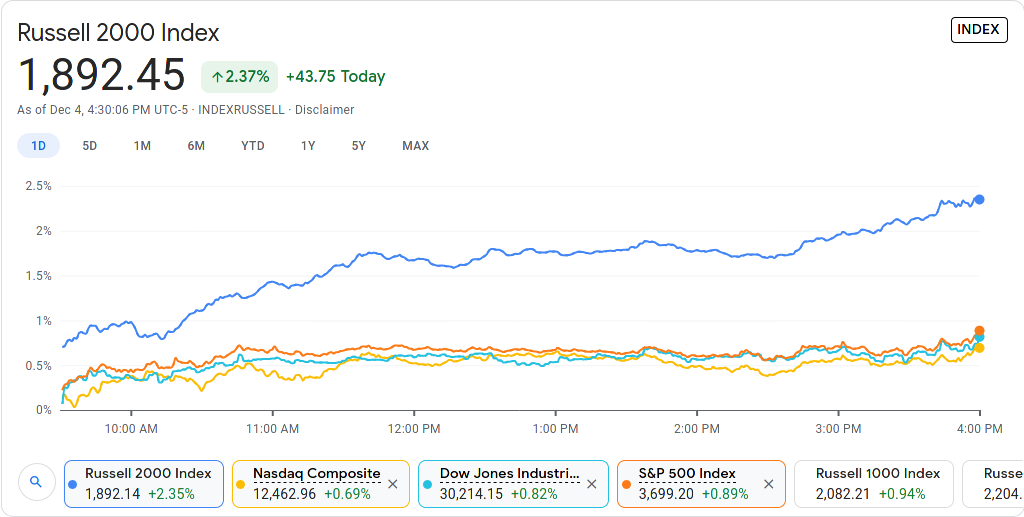

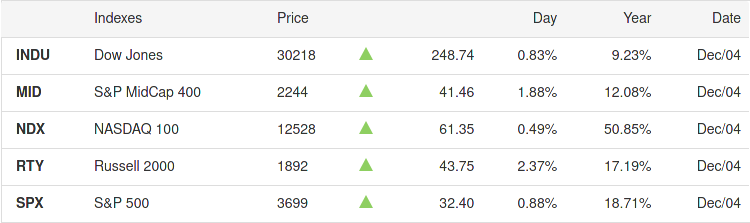

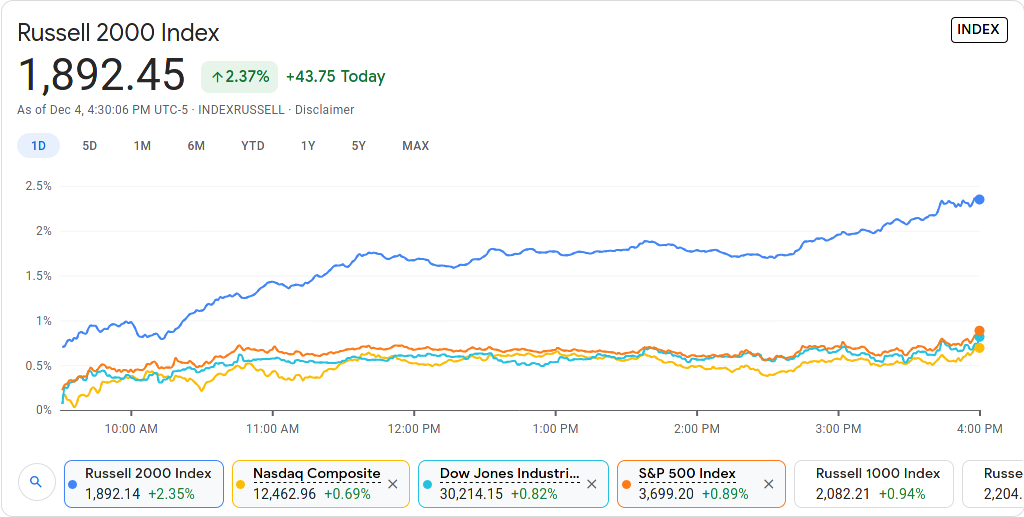

[tracking: XLE]All indices finished up for the week, but the Russell 2000 (RUT) has begun screaming past the others on a regular basis and is quickly catching up to the S&P’s yearly return (though all pale in comparison to the NASDAQ’s near 51%).

The RUT is primed to appreciate further, but it will be among the first to flame up should there be a reversal of fortunes, being as how its components are some of the most vulnerable to the pandemical nature of everything.

Generally-speaking, asset managers appear to be placing all their eggs in one basket, i.e. the basket of recovery. When people begin moving the same way, or “overcrowding” trades (to borrow a term), pay attention; bubbles could form across the board, and disappointment visit us possibly in the midst of 2021.

Our fortunes are predicated on everything working out just so: vaccines, stimulus, presidential transition, ending the pandemic, recovery, return to life as we knew it on some level. What if they don’t? Furthermore, we may all agree that there will be a recovery some day, but the more important point is that the wider consensus on what it looks like may not materialize. That's part and parcel of what could jeopardize the recovery; the consensus isn’t informed by fundamentals, but rather by preconceived notions.

[tracking: VTWO, TNA]Biden’s cabinet picks signal a focus on equity, which is crucial as marginalized groups have suffered disproportionate blows at the hands of the pandemic and America’s management of it.

Used car trends: The latest Carvana car count rose to 34,971 vehicles from 34,644 the week prior, while the CarGurus price index again fell slightly to $22,422 from $22,456.

Sovereign matters:

China’s central bank continues to inject liquidity into the country’s financial system via intermediate term loans and reverse repos.

Venezuela’s interannual inflation rate has hit 4,087%. Residents are relying on foreign currencies such as the dollar, not the bolivar, for transactions.

S&P has maintained their rating stance on Mexico, but also their negative outlook. They expect further economic trials for the country moving forward, which include difficulties at PEMEX.

Fitch downgraded Malaysia for the first time in over 20 years on account of its high and worsening debt/GDP and debt/revenue ratios; the concentrated nature of its revenue base given the pandemic (especially oil and tourism); and the slim majority of the new ruling party underlying its declared reform efforts.

Fitch has downgraded Suriname as the country is now in default and is pursuing a debt service standstill. Fitch doesn’t believe it will be sufficient to rectify the nation’s credit woes, including a lack of forex holdings.

Colombia has drawn $ billions from its line of credit with the IMF.

Australia, Ireland, and the UK are also experiencing feverish housing markets.

[tracking: EDC, VXUS, VWO]As of December 4, the US witnessed 136,049 fatalities strictly classified as “pneumonia” with no acknowledgement of COVID-19 on the death certificates, per CDC excess deaths data. That’s 401 people per day on average. As the CDC points out, many of these could be miscategorized COVID-19 fatalities going unrecognized in official tallies, meaning we’re undercounting. This, in addition to the official coronavirus death toll of 276,375, puts the likely COVID-19 death count somewhere north of 350-360k. Across all causes of death, we’re witnessing 112% of the deaths we would have expected in a non-pandemic year given historical trends.³

Footnotes

¹ “COVID-19: Urgent Actions Needed to Better Ensure an Effective Federal Response.” Report to Congressional Committees GAO-21-191. GAO (November 30, 2020).

² “Unemployment Insurance Weekly Claims News Release.” Release Number: USDL 20-2198-NAT. US Department of Labor (December 3, 2020).

³ Valenta, Philip. “Death by COVID-19 Hides in Plain Sight.” HedgeHound archive (December 4, 2020).